Tech tops inflation

- Market rebounds as traders embrace (most) Big Tech earnings

- Commodities cool, bond yields edge higher

- This week: Jobs, FOMC meeting, more tech earnings

Last week was shaping up to be a big week for Big Tech, and in the end, tech-sector enthusiasm won the day despite concerns about inflation and delayed rate cuts.

Not that the outcome was a foregone conclusion. The S&P 500 (SPX) sold off as much as 1.6% early Thursday as disappointment over Meta’s (META) earnings call and inflationary signals from the Q1 GDP report wiped out most of a Monday-Tuesday rebound. But beats from Alphabet (GOOGL) and Microsoft (MSFT) after the bell energized Friday’s trading, despite another sticky inflation reading from the PCE Price Index:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Tech beats fuel market bounce.

The fine print: While Thursday’s Q1 GDP estimate was weaker than expected—1.6% vs. 2.3%—one of its below-the-headline data points appeared to heighten inflation concerns. Core PCE Prices (not to be confused with the monthly PCE Price Index released Friday) jumped from 2% in Q4 2023 to 3.7% in Q1, driving chatter about potential “stagflation”—the combination of a slowing economy and rising inflation.

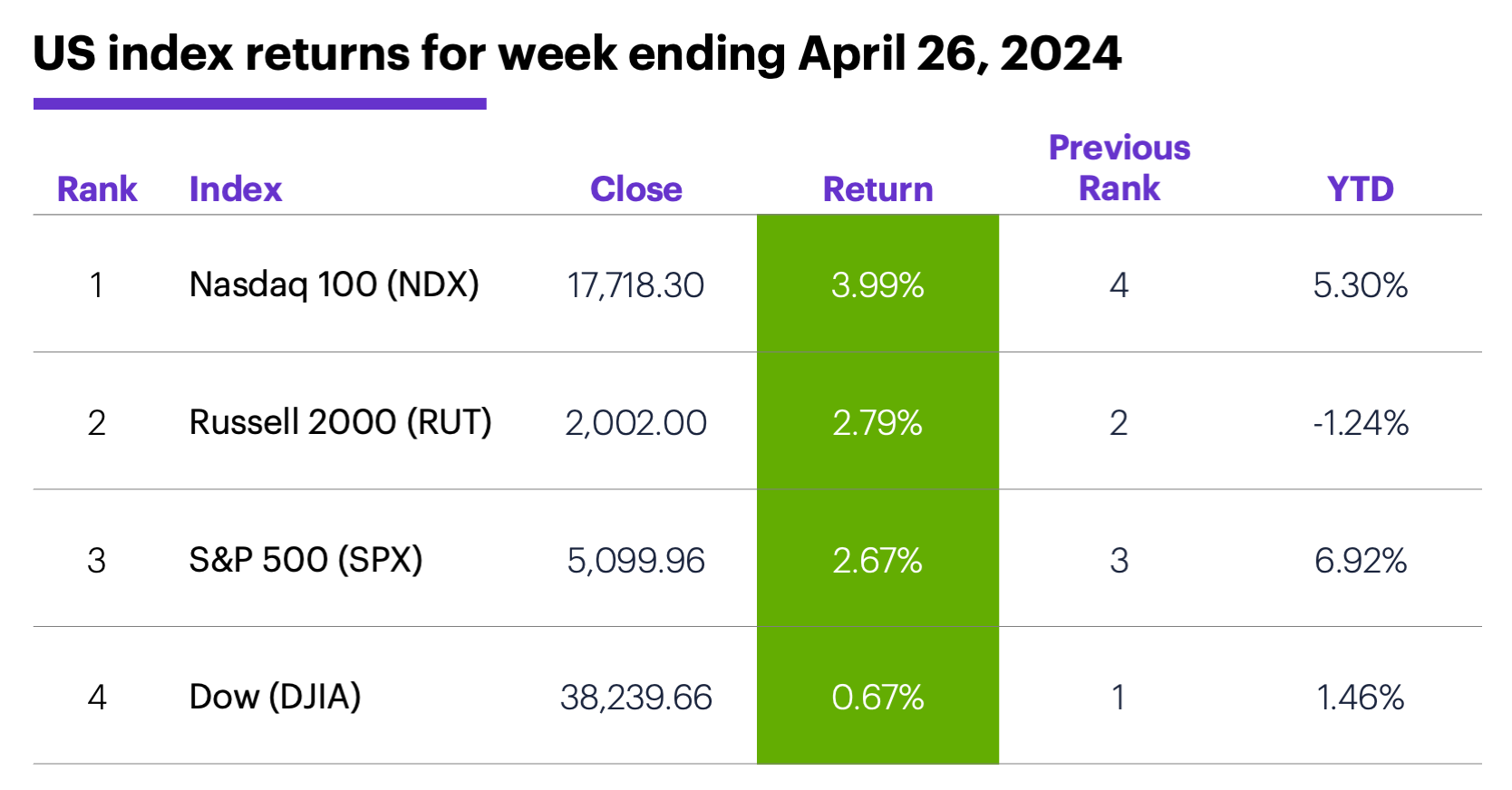

The scorecard: The Nasdaq 100 (NDX) tech index bounced back from its worst week since November 2022 with its best week since November 2023:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+5.3%), consumer discretionary (+3.6%), and communication services (+2.7%). The weakest sectors were materials (+0.7%), health care (+0.8%), and energy (+1%).

Stock movers: B. Riley Financial (RILY) +37% to $29.75 on Wednesday, Cullinan Therapeutics (CGEM) +31% to $25.30 on Friday. On the downside, Destiny Tech100 (DXYZ) -23% to $18.83 and Saia (SAIA) -21% to $428.81, both on Friday.

Futures: June gold (GCM4) posted its biggest down day of the year last Monday, and ended the week more than $60 lower at $2,347.20. June WTI crude oil (CLM4) rebounded to close last week more than $1.60 higher at $83.85. Week’s biggest gainers: July hard red wheat (KWN4) +12.2%, July wheat (ZWN4) +9.8%. Week’s biggest decliners: May VIX (VXK4) -13.7%, July cocoa (CCN4) -7.6%.

Coming this week

The earnings floodgate opens this week—more than 700 companies will report on just Wednesday and Thursday. Here’s a sample:

●Monday: Domino's Pizza (DPZ), On Semiconductor (ON), F5 (FFIV), Logitech (LOGI), Lattice Semiconductor (LSCC), Medifast (MED), MicroStrategy (MSTR), NXP Semiconductors (NXPI), Rambus (RMBS), SBA Communications (SBAC)

●Tuesday: Coca Cola (KO), LGI Homes (LGIH), Eli Lilly (LLY), McDonald's (MCD), Martin Marietta (MLM), PayPal (PYPL), Molson Coors (TAP), Advanced Micro Devices (AMD), Amazon.com (AMZN), Clorox (CLX), Starbucks (SBUX)

●Wednesday: Automatic Data Processing (ADP), Estee Lauder (EL), Barrick Gold (GOLD), Kraft Heinz (KHC), Mastercard (MA), Pfizer (PFE), Yum Brands (YUM), Carvana (CVNA), eBay (EBAY), Etsy (ETSY), First Solar (FSLR), Paycom (PAYC), Qualcomm (QCOM)

●Thursday: Baxter (BAX), Kellanova (K), Regeneron Pharmaceuticals (REGN), Wayfair (W), Apple (AAPL), Amgen (AMGN), Bill Holdings (BILL), Booking Holdings (BKNG), Coinbase (COIN), Five9 (FIVN), Illumina (ILMN), iRhythm Technologies (IRTC), Block (SQ)

●Friday: Cboe Global Markets (CBOE), Hershey (HSY), XPO (XPO)

Jobs data highlights the economic calendar, but Wednesday’s interest rate announcement (no change expected) will be dissected for insight into how recent data may be shaping the Fed’s plans:

●Tuesday: Employment Cost Index, S&P Case-Shiller Home Price, FHFA House Price Index, Chicago PMI, Consumer Confidence

●Wednesday: ADP Employment, S&P Global Manufacturing PMI, ISM Manufacturing Report, Job Openings and Labor Turnover Survey (JOLTS), Construction Spending, Fed interest rate decision

●Thursday: Challenger Job Cut Report, Balance of Trade, Productivity and Labor Costs, Factory Orders

●Friday: Employment Report

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Bucking the election year trend?

Despite the pullback from its March record highs, the stock market has, so far, performed a little better than it has in other presidential election years.

As we noted in “Election year market patterns” back in January, the SPX’s January-October performance has, historically, been a little weaker in presidential election years than in others. That underperformance has also been evident in the first four months of the year. Since 1944, the SPX’s average January-April return in non-election years was 4.4%. In election years, it was 1.3%.1 With a couple of days left in April, the SPX is up 6.9% for the year.

Of course, it’s fair to point out that other factors, such as interest rates, inflation, and earnings, have been more relevant issues for the market than the November election. But it’s also valid to argue that election outcomes can shape the economic and financial conditions that drive market action on a longer-term basis—and not just domestically. As Morgan Stanley & Co. strategists recently noted, European stocks derive roughly 25% of their market-cap-weighted revenues from the US, making the November election more than just a matter of politics.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 All figures reflect S&P 500 (SPX) monthly and daily closing prices, 1957-2024. Supporting document available upon request.

2 MorganStanley.com. European Markets React to Upcoming U.S. Election. 4/24/24.