Bulls keep squeezing

- Market still risk-on heading into final week of 2023

- More records for Dow and Nasdaq, S&P 500 comes close

- This week: Home prices, trade balance, consumer confidence

Two things about this market are certain. First, the S&P 500 (SPX) will eventually post a weekly loss.

Second, last week wasn’t that week.

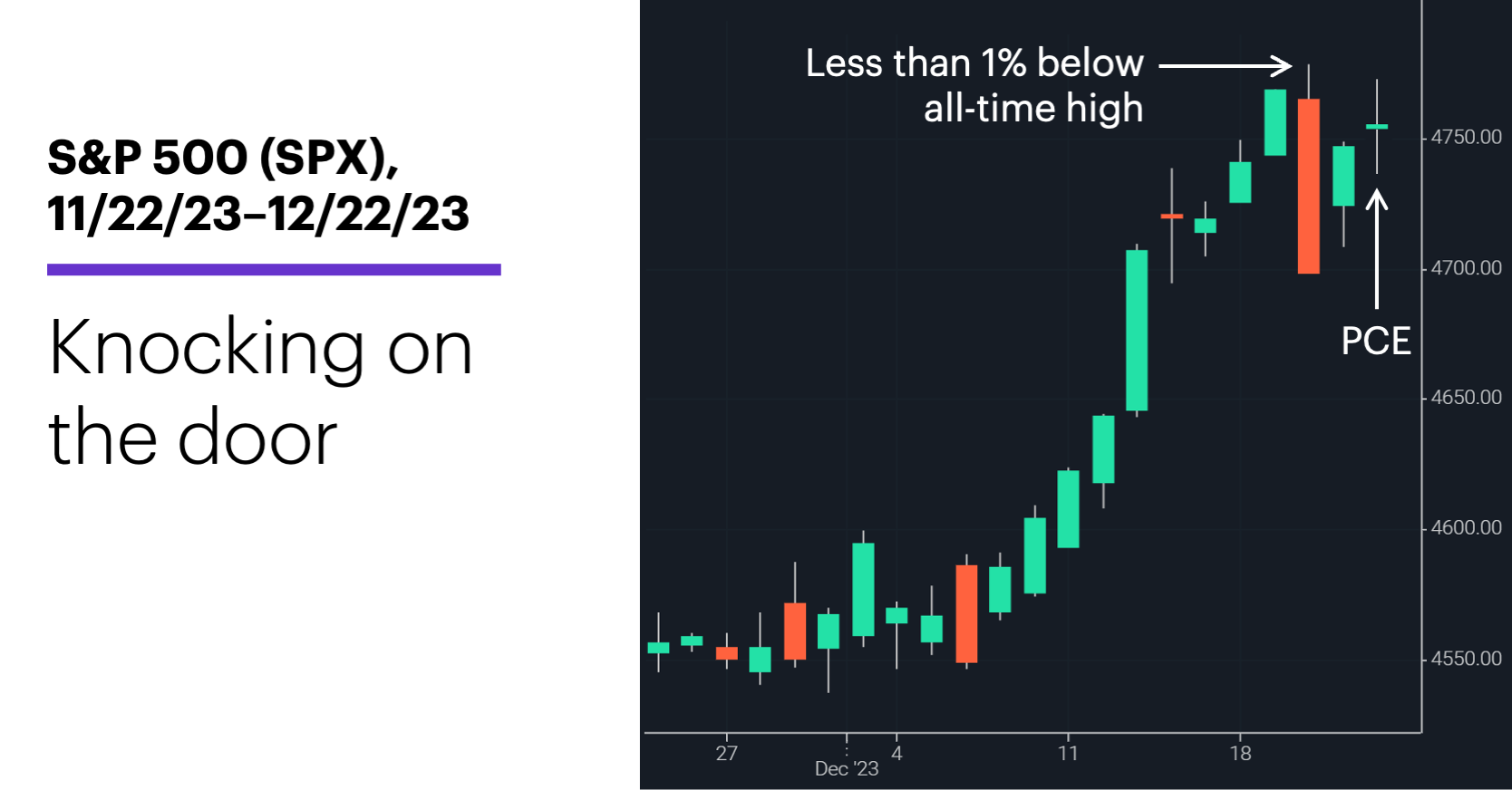

For a moment, though, it looked like it could be. When the S&P 500 (SPX) experienced its biggest one-day sell-off since September last Wednesday—after rallying to within 0.9% of its all-time high earlier in the day—the index slipped into the red for the week. But thanks to a strong Thursday rebound (and modest follow-through on Friday), the SPX’s run of consecutive up weeks extended to eight:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: S&P 500 one week from longest streak since 2004.

The fine print: The market’s boundary-pushing rally off its October lows has been fueled in part by the idea that falling inflation and a cooling economy will translate into rate hikes sooner rather than later—an idea the Fed has, without success, attempted to downplay. Morgan Stanley Wealth Management recently highlighted the potential risk that, having aggressively priced in rate cuts, the market may not get the boost many people expect if and when rates actually fall.1

The number: -0.1%, the month-over-month drop in the PCE Price Index reported on Friday. It was the first decline for Fed’s preferred inflation gauge in more than a year.

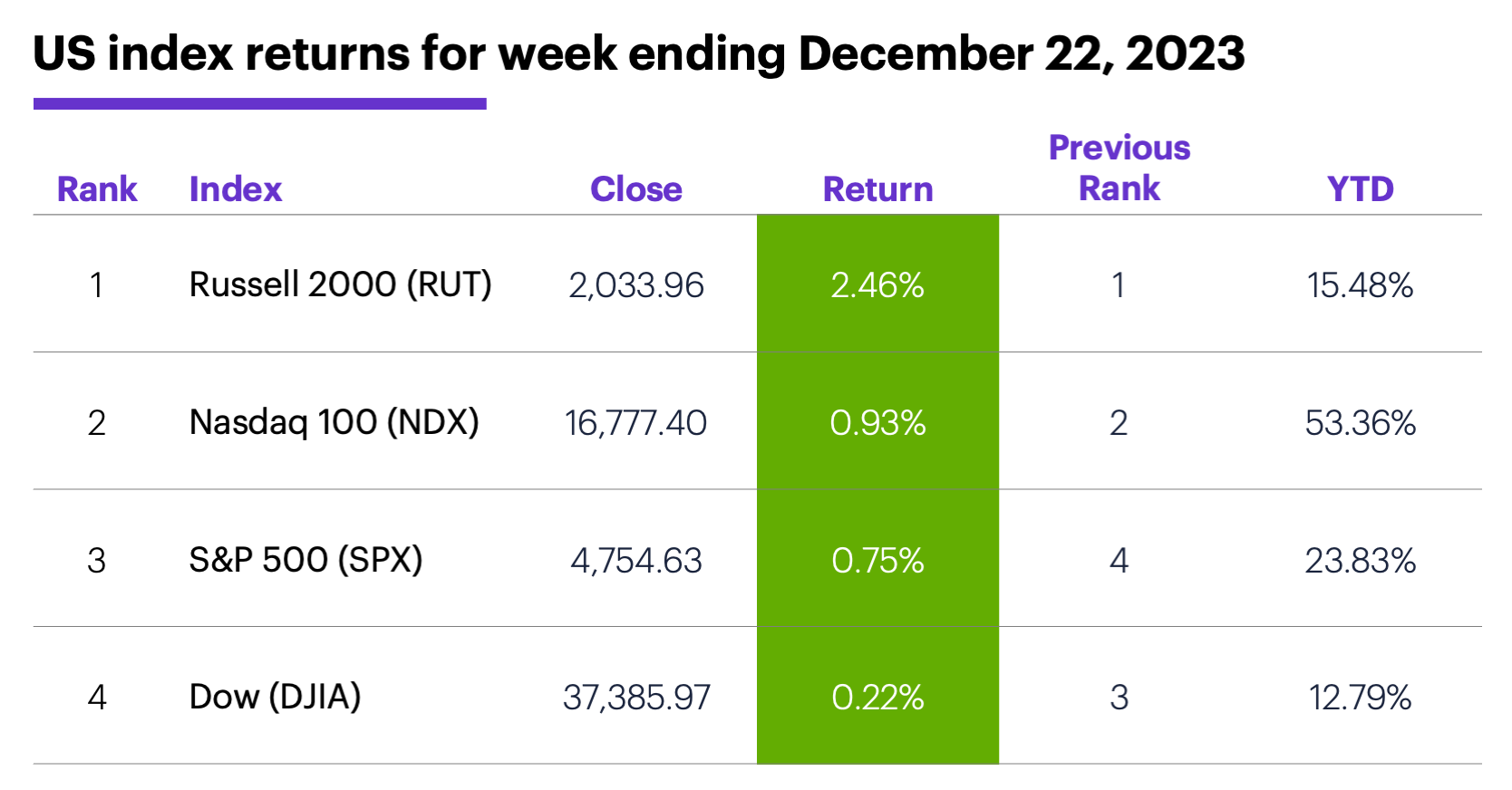

The scorecard: The Dow Jones Industrial Average (DJIA) and Nasdaq 100 (NDX) both hit fresh record highs, but the small-cap Russell 2000 (RUT) led the market for a fourth week—its longest run at the top since February 2022:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+4.1%), energy (+1.7%), and materials (+1.1%). The weakest sectors were utilities (-1.3%), technology (+0.1%), and real estate (+0.3%).

Stock movers: on Monday Zimvie (ZIMV) +52% to $17.10, Karuna Therapeutics (KRTX) +48% to $317.85 on Friday. On the downside, Lantheus (LNTH) -27% to $55.60 on Monday, Argenx SE (ARGX) -25% to $338.91 on Tuesday.

Futures: February WTI crude oil (CLG4) closed a volatile week modestly higher at $73.56. A Friday rally pushed February gold (GCG4) to a three-week high close of $2,069.10. Week’s biggest gains: January VIX (VXF4) +3.6%, March aluminum (ALH4) +3.5%. Week’s biggest losses: March orange juice (OJH4) -10.7%, March sugar (SBH4) -6.2%.

Coming this week

This week’s numbers include:

●Tuesday: Chicago Fed National Activity Index, S&P Case-Shiller Home Price, FHFA House Price Index, Consumer Confidence

●Thursday: Trade Balance in Goods, Retail and Wholesale Inventories (advance), Pending Home Sales

●Friday: Chicago PMI

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Market on the run

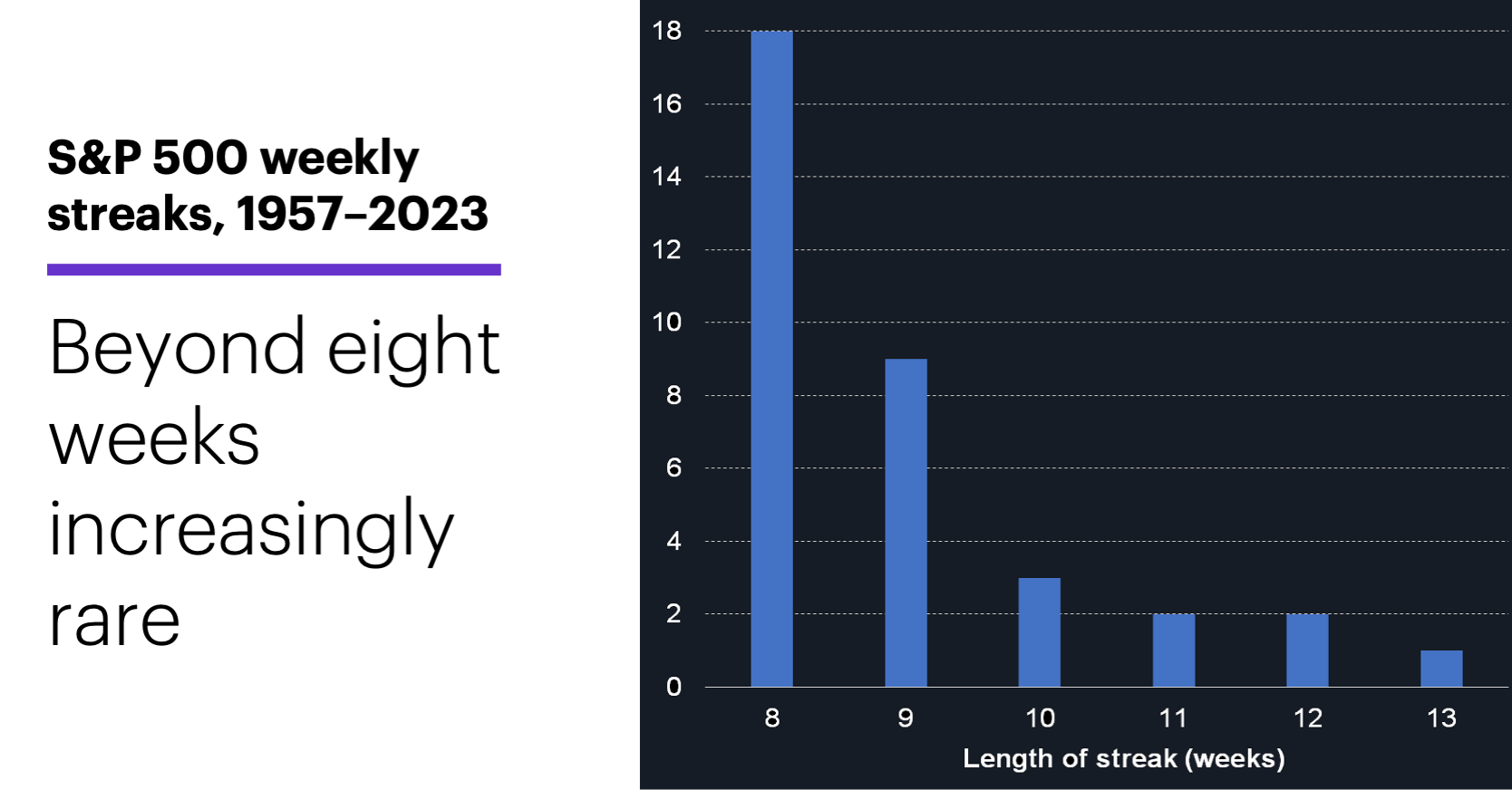

The SPX’s eight-week streak is nothing to sneeze at—it’s the longest the index has gone without a down week since November 2017, and one of only 33 eight-week-or-longer runs since 1957.2

In terms of how much the SPX has rallied over the past eight weeks, the story initially appears to be a little different. As of Friday, the SPX was up 15.5% since October 27. That’s its biggest eight-week return since August 2022, but only the 31st-largest since 1957—and well below the 28.4% the index gained in the record-setting eight weeks that ended on May 1, 2009.

Reality check: There have been 3,494 other eight-week periods since 1957, which means the SPX gained more in the most recent one than it did in 99% of all the others. Also, if we look at just the 348 eight-week periods that, like the one that just ended, followed the lowest SPX close in at least 12 weeks, that 15.5% return is the 10th-largest since 1957, and bigger than 97% of all others.

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

If the weekly streak continues, the SPX will be pushing into rare territory. The chart above shows that of the 17 previous eight-week runs since 1957, nine extended to a ninth week. But of those nine, only three made it to 10 weeks, while two of those made it to 12 weeks. Only one (in 1957) made it to 13 weeks—the longest run of the past 67 years.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. 3 Risks in an Unfamiliar Market. 12/11/23.

2 Reflects S&P 500 (SPX) weekly closing prices, 1/2/40–12/15/23. Supporting document available upon request.