Bulls get the bounce

- Stocks erase Fed stumble, end week at record highs

- Jobs market surprises to upside, split decision for Big Tech

- This week: Service economy data, earnings grab bag

Last week looked like it could be a big one for the market—stocks had to sift through mega-tech earnings, a Fed interest rate announcement, and a jobs report—and the market didn’t disappoint.

It was a volatile ride, but two days after the biggest down day of the year dropped it to a seven-day low, the S&P 500 (SPX) closed Friday at a new all-time high and logged its 13th up week of the past 14:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks shrug off (for now) delayed rate-cut outlook.

The fine print: Last Wednesday the Fed downplayed the possibility of a March rate cut, and Friday’s (much) stronger-than-expected jobs report—more than double the estimated number of new jobs—seemed to strengthen the idea that the Fed would hold off until at least June. By the end of the week, the odds of a rate cut at the Fed’s March meeting had dropped from above 60% to around 21%.1 But that didn’t appear to faze bulls.

The number: 2 (out of 5), the number of last week’s mega-cap stocks that rallied after releasing earnings. Alphabet (GOOGL) and Microsoft (MSFT) sold off Wednesday after posting their numbers, while Amazon (AMZN) and Meta (META) jumped after releasing theirs. Apple (AAPL) was the odd man out, falling modestly on Friday.

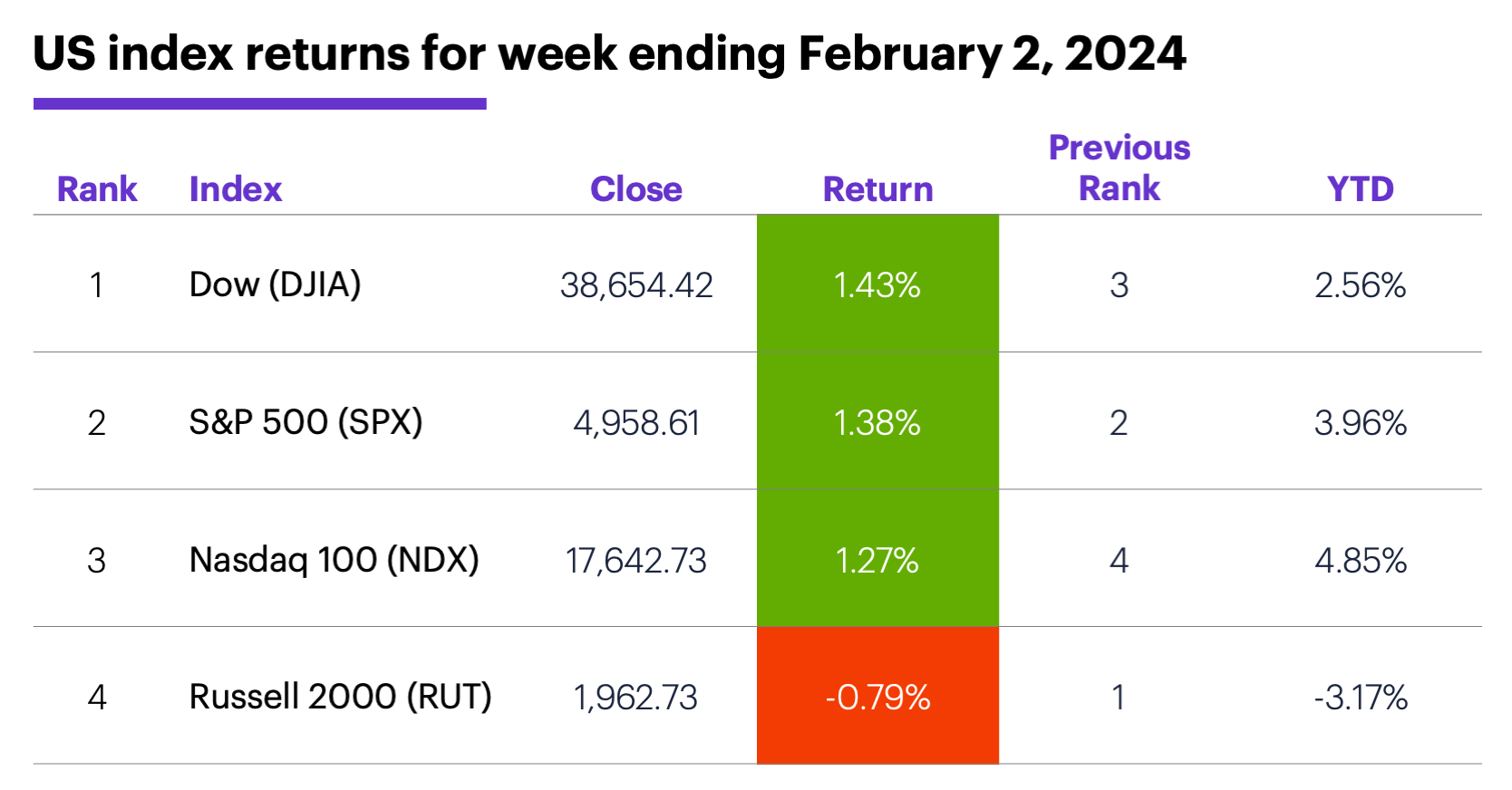

The scorecard: The small-cap Russell 2000 (RUT) continued to diverge from the rest of the market:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were consumer discretionary (+3.9%), consumer staples (+2.4%), and health care (+2.2%). The weakest sectors were energy (-0.7%), real estate (-0.4%), and utilities (+0.6%).

Stock movers: Sanmina (SANM) +28% to $64.91 on Tuesday, Powell Industries (POWL) +45% to $118.53 on Wednesday. On the downside Calix (CALX) -26% on Tuesday, New York Community Bank (NYCB) -38% to $6.47 on Wednesday.

Futures: March WTI crude oil (CLH4) tumbled to its lowest level in more than two weeks, closing Friday at $72.28. Despite pulling back on Friday, April gold (GCJ4) ended the week modestly higher at $2,053.70. Week’s biggest rallies: March orange juice (OJH4) +20.3%, March cocoa (CCH4) +7.2%. Week’s biggest declines: March RBOB gasoline (RBH4) -8.1%, March WTI crude oil (CLH4) -7.5%.

Coming this week

This week’s earnings calendar runs the gamut—everything from high-profile tech and consumer names to automakers and big pharma. Here’s a sample:

●Monday: Caterpillar (CAT), Estee Lauder (EL), McDonald’s (MCD), ON Semiconductor (ON), Tyson Foods (TSN), NXP Semiconductors (NXPI), Palantir (PLTR), Rambus (RMBS), Vertex Pharmaceuticals (VRTX)

●Tuesday: Eli Lilly (LLY), Spotify (SPOT), Toyota (TM), Amgen (AMGN), Chipotle (CMG), Edwards Lifesciences (EW), Enphase (ENPH), e.l.f. Beauty (ELF), Ford (F), Gilead Sciences (GILD), Silicon Motion Technology (SIMO), Snap (SNAP)

●Wednesday: Roblox (RBLX), Uber (UBER), Digital Turbine (APPS), Disney (DIS), Mattel (MAT), Netgear (NTGR), O’Reilly Automotive (ORLY), Paycom Software (PAYC), PayPal (PYPL), Wynn Resorts (WYNN)

●Thursday: AstraZeneca (AZN), Baxter (BAX), ConocoPhillips (COP), Hershey (HSY), Kenvue (KVUE), Ralph Lauren (RL), Spirit Airlines (SAVE), Spectrum Brands (SPB), Tapestry (TPR), Affirm (AFRM), Bill.com (BILL), Impinj (PI), Verisign (VRSN)

●Friday: Global Payments (GPN), PepsiCo (PEP), W.P. Carey (WPC)

This week’s numbers include:

●Monday: S&P Global Composite PMI, ISM Services Index

●Wednesday: Trade Balance, Consumer Credit

●Thursday: Wholesale inventories

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Lucky or unlucky 13?

The S&P 500 has had 13 up weeks in a 14-week span only 19 other times since 1957.2 Twelve of those times it closed higher the following week. It closed higher the week after that—that is, posted 15 up weeks in a 16-week span—only seven times. It closed higher in 16 out of 17 weeks just two times—once in 1957, once in 1958. So far, it’s never made it to 17 out of 18 weeks.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 CMEGroup.com. FedWatch Tool. 2/22/24.

2 Figures reflect S&P 500 (SPX) monthly closing prices, January 1957–January 2024. Supporting document available upon request.