Tech overrides inflation

- Stocks rally, yields fall amid mixed inflation data

- Small caps surge, chip sell-off highlights tech sector volatility

- This week: Retail sales, housing starts, full week of earnings

To the casual observer, last week’s stock market action may have been somewhat puzzling. The broad market retreated from record highs after one of the clearest indications that inflation had continued to ease. The next day it rallied, despite a stickier-than-expected inflation reading.

But there was more to the market than inflation data. On Thursday, a tech sell-off (led by semiconductor stocks) dragged down the S&P 500 (SPX) even though the Consumer Price Index (CPI) came in cool. When many of those stocks rebounded on Friday, the market shrugged off a hotter-than-expected Producer Price Index (PPI), locking in the SPX’s 10th up week of the past 12 while surviving a late sell-off that erased half the day’s gain:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: As goes tech, so goes the market?

The fine print: Nvidia (NVDA) fell 5.6% last Thursday, the headline move of a bad day for tech in general, and semiconductor stocks in particular. The major indexes with the most exposure to the group (SPX, Nasdaq Composite, and Nasdaq 100) closed lower, while those with the least (Russell 2000 and Dow Jones Industrial Average) gained ground.

The move: Bonds behaved as expected after last Thursday’s friendly CPI reading—prices rose as yields tumbled to their lowest level since mid-March, with the benchmark 10-year T-note yield falling as low as 4.19%.

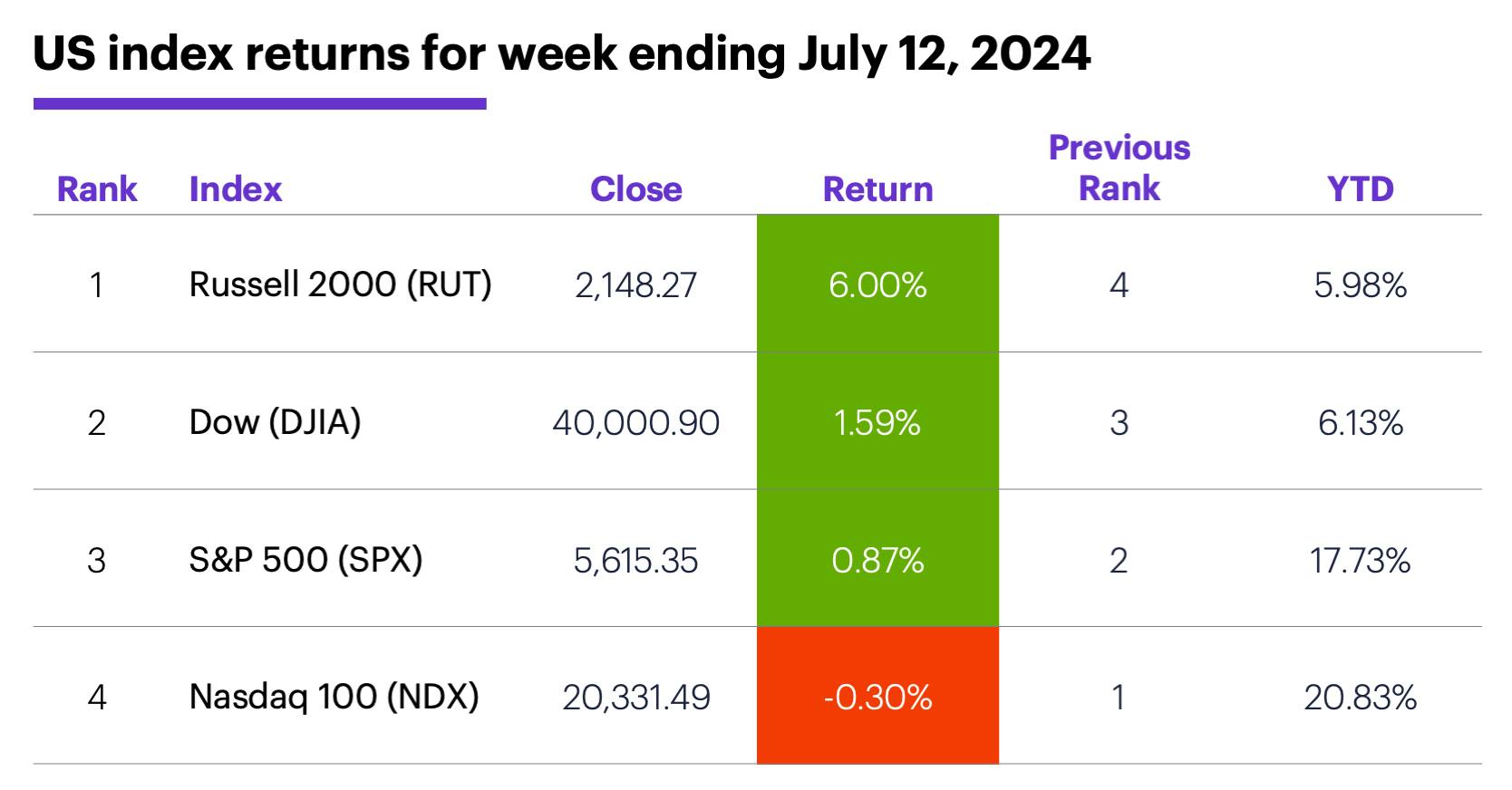

The scorecard: The Russell 2000 (RUT) small-cap index posted its biggest weekly gain since last November and turned positive for the year. The Nasdaq 100 (NDX) tech index posted a small loss:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were real estate (+4.7%), utilities (+4.1%), and materials (+3.1%). The weakest sectors were communication services (-3.6%), consumer staples (+0.2%), and energy (+0.4%).

Stock movers: On Monday, Morphic (MORF) +75% to $55.74 and Annovis Bio (ANVS) +39% to $15.46. On the downside, Indivior (INDV) -34% to $10.19 and Helen of Troy (HELE) -28% to $64.33, both on Tuesday.

Futures: August WTI crude oil (CLQ4) posted its first down week since June 7, falling a little less than $1 to $82.33. Thanks to its second-biggest up day of the year last Thursday (+1.8%), August gold (GCQ4) ended the week up nearly $23 at $2,420.70. Week’s biggest gains: September coffee (KCU4) +8.7%, September E-Mini Russell 2000 (RTYU4) +6.3%. Week’s biggest declines: September wheat (ZWU4) -6.7%, September palladium (PAU4) -6.6%.

Coming this week

Financials dominate the first full week of earnings season, but some big tech, big pharma, oil, and airlines also check in. Highlights include:

●Monday: Blackrock (BLK), Goldman Sachs (GS), FB Financial (FBK), ServisFirst Bancshares (SFBS)

●Tuesday: Bank Of America (BAC), Morgan Stanley (MS), Progressive (PGR), PNC Financial Services (PNC), UnitedHealth (UNH), J.B. Hunt Transport (JBHT)

●Wednesday: ASML (ASML), Johnson & Johnson (JNJ), US Bancorp (USB), Prologis (PLD), Alcoa (AA), Crown Castle (CCI), Discover Financial (DFS), United Airlines (UAL), Wintrust (WTFC)

●Thursday: American Airlines (AAL), Abbott Labs (ABT), Cintas (CTAS), D.R. Horton (DHI), Keycorp (KEY), Novartis AG (NVS), Taiwan Semiconductor (TSM), Intuitive Surgical (ISRG), Netflix (NFLX), PPG (PPG)

●Friday: American Express (AXP), Halliburton (HAL), Verizon (VZ), Schlumberger (SLB)

This week’s numbers include:

●Monday: Empire State Manufacturing Index

●Tuesday: Retail Sales, Import Price Index, Business Inventories, NAHB Housing Market Index

●Wednesday: Housing Starts and Building Permits, Industrial Production and Capacity Utilization, Fed Beige Book

●Thursday: Philadelphia Fed Manufacturing Survey, Leading Economic Indicators Index

This week’s stocks splits include:

●Monday: Broadcom (AVGO), 10 for 1

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

‘Tis the season(s)

With the next major inflation reading (the PCE Price Index) more than two weeks away, the market will likely turn its attention to earnings. The first companies to announce last week posted mixed numbers and got mixed initial reactions: Delta Air Lines (DAL) and ConAgra (CAG) fell, Fastenal (FAST) rallied, PepsiCo (PEP) was flat, and all three of the big banks that announced on Friday closed lower.

Since October 2010, the first full week of earnings season has tended to be a stronger-than-average week for the market—but not dramatically so. For example, there have been 26 other times the first full week of the season followed a Friday featuring the release of the initial big bank numbers. In those weeks, the SPX had a median gain of 0.4% (vs. 0.3% for all weeks) and closed higher 65% of the time (vs. 59% of all weeks).1

We’re also in the midst of another season—election season. Morgan Stanley & Co. strategists noted recent events have increased inquiries about the implications of a Republican sweep this November. But while they acknowledge that both growth and longer-term interest rates could move higher in this scenario, it doesn’t necessarily call for a shift toward value and cyclical stocks—a playbook that worked leading into the 2016 election.2

The difference, they explain, is that the economic cycle is more mature today than it was in 2016—a backdrop historically characterized by the market paying up for quality and liquidity. Also, in 2016 inflation wasn’t a headwind to consumers the way it is now. Their take: Remain focused on quality and be selective about cyclicals.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 All figures reflect S&P 500 (SPX) weekly closing prices, 2010-2024. Supporting document available upon request.

2 MorganStanley.com. 2024 U.S. Elections: The Impact of Inflation. 7/8/24.