More summer heat for stocks

- Latest milestones: S&P 500 tops 5,500, NDX tops 20,000

- Jobs market cools, bond yields swing, oil gets pumped

- This week: Inflation (CPI and PPI), intro to earnings season

A holiday-shortened week didn’t slow down the stock market.

Led—again—by the tech sector, multiple major indexes recorded new records last week, including on Friday after the monthly jobs report highlighted a cooling labor market. The S&P 500 (SPX) closed higher every day, and outgained its average full-week positive return in just four trading days:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Jobs market slows, stock market doesn’t.

The fine print: The minutes from the Fed’s June policy meeting showed some board members were sufficiently concerned about sticky inflation to hike interest rates, if necessary. Is the Fed behind the curve? As Morgan Stanley & Co. strategists note, the Fed is still applying “economic brakes” via high interest rates even though the US economy is slowing. The longer it waits to cut, the greater the risk it won’t be able to prevent a potential recession—a scenario the strategists still peg as a low-probability event, but one that could gain importance as time passes.1

The moves: Tesla (TSLA) gained more than 27% last week, its largest weekly gain since January 2023, and its seventh-strongest on record. Also, after jumping 11 basis points to 4.48% last Monday—its highest level since May 31—the benchmark 10-year Treasury yield reversed to end the week lower at 4.28%.

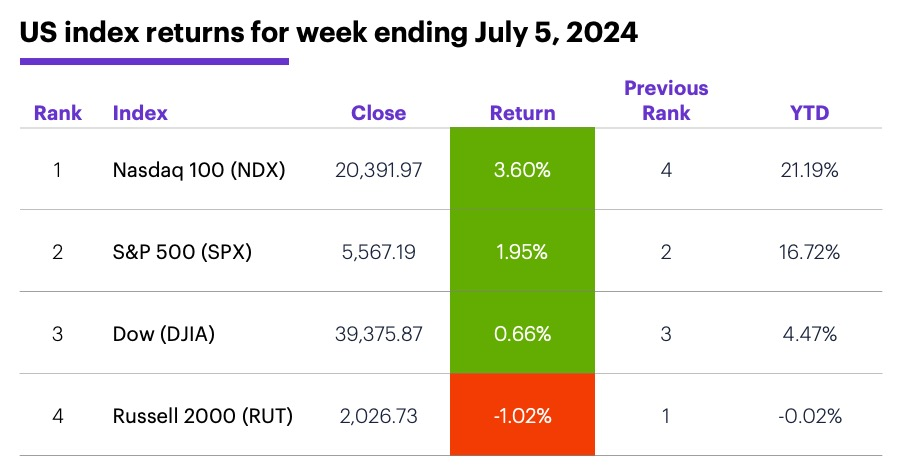

The scorecard: The Nasdaq 100 (NDX) tech index posted its second-biggest weekly gain of the year, while the Russell 2000 (RUT) small-cap index once again ignored the larger market trend:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+3.4%), consumer discretionary (+2.3%), and communication services (+2.2%). The weakest sectors were health care (-1%), energy (-0.9%), and utilities (-0.5%).

Stock movers: Inseego (INSG) +20% to $12.81, MediWound (MDWD) +35% to $1960 on Friday. On the downside, Cartesian Therapeutics (RNAC) -10% to $24.27 on Monday and -35% to $15.77 on Tuesday, Pacira Biosciences (PCRX) -20% to $22.74 on Tuesday.

Futures: Oil’s summer rally continued. August WTI crude oil (CLQ4) rallied more than $1.50 last week, closing Friday at $83.16. August gold (GCQ4) made a push out of its recent consolidation, gaining nearly $60 and closing Friday at a six-week high of $2,397.70. Week’s biggest gains: September palladium (PAU4) +12.1%, December soybean oil (ZLZ4) +11.8%. Week’s biggest declines: August natural gas (NGQ4) -13.6%, July ether (ETHN4) -13.5%.

Coming this week

All roads lead to inflation this week, but Fed Chair Jerome Powell’s semiannual testimony before the Senate Banking Committee will also be closely watched:

●Monday: New York Fed Consumer Inflation Expectations, Consumer Credit

●Tuesday: NFIB Business Optimism Index, Jerome Powell Senate testimony

●Wednesday: Wholesale Inventories

●Thursday: Consumer Price Index (CPI)

●Friday: Producer Price Index (PPI), Consumer Sentiment (preliminary)

The first Q2 earnings start trickling in, highlighted by a few big banks on Friday:

●Monday: Greenbrier (GBX)

●Tuesday: Helen Of Troy (HELE), Smart Global (SGH)

●Wednesday: AZZ (AZZ), PriceSmart (PSMT), WD-40 (WDFC)

●Thursday: Conagra Brands (CAG), Cintas (CTAS), Delta Air Lines (DAL), PepsiCo (PEP)

●Friday: Blackrock (BLK), Citigroup (C), Fastenal (FAST), JPMorgan Chase (JPM), Wells Fargo (WFC)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Pullbacks, rebounds, and trends

July definitely got off to a bullish start. If it turns out to be another positive month for the US stock market, the result wouldn’t just be in line with July’s bullish tendency over the past couple of decades, it would also mesh with the market’s historical performance after other strong eight-month rallies.

From the end of last October (which marked the end of a three-month pullback) to the end of last month, the SPX gained 30%—more than it has in all but 11 other eight-month periods since 1957.2 The last time it rallied that much in an eight-month span (after a down month) was in June 2021. While that’s not much to go on, the SPX was positive the following month eight of 11 times, with an average return of 2.2%.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Why Central Banks Still Get it Wrong Sometimes. 7/3/24.

2 All figures reflect S&P 500 (SPX) monthly closing prices, 1957-2024. Supporting document available upon request.