Market edges to new highs

- Tech leads as stocks grind higher to start earnings season

- Inflation moderate, retail spending tops expectations

- This week: GOOGL and TSLA earnings, durable goods

As earnings season gets into full swing, the stock market is still looking for direction, coming off a week in which major indexes set fresh records but continued to trade mostly sideways—despite mostly positive economic data and solid earnings from big banks.

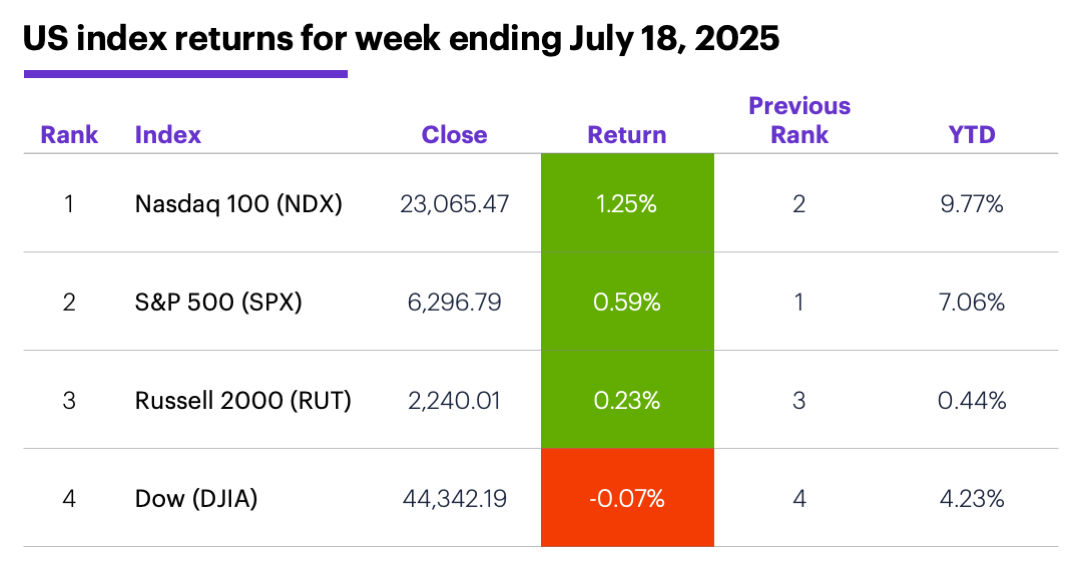

The S&P 500 (SPX) closed at a new record high last Thursday and hit an intraday record on Friday, but its 0.59% net gain represented the index’s smallest positive weekly return since March 21:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: New records, but modest gains.

The fine print: Last week’s relative tech strength owed a great deal to news that NVIDIA (NVDA) would be able to resume selling its H20 artificial intelligence chip to China. The stock jumped 4% to a new record high after the announcement last Tuesday, providing a rising tide that helped lift many tech (and especially AI) boats.

The numbers: 0.2%, the month-over-month increase in the core Consumer Price Index (CPI) reported last Tuesday—a smaller increase than expected, but higher than the previous month’s increase. The higher-than-expected 0.6% increase in retail sales reported Thursday suggested consumers were still spending, although they appeared to be more selective in their purchases.

The scorecard: The Dow Jones Industrial Average (DJIA) was the only major index to lose ground last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were information technology (+2%), utilities (+1.4%), and industrials (+0.7%). The weakest sectors were energy (-3.9%), health care (-2.5%), and materials (-1.5%).

Stock moves: USA Rare Earth (USAR) +31% to $15.54 on Tuesday, SharpLink Gaming (SBET) +29% to $37.38 on Wednesday. On the downside, Newegg Commerce (NEGG) -26% to $36.22 on Monday (and -19% to $29.33 on Tuesday), CareDx (CDNA) -38% to $11.81 on Wednesday.

Yields: The benchmark 10-year Treasury yield rose 0.01% to 4.43% last week.

US dollar: The US Dollar Index (DXY) rallied 0.63 to 98.48.

Futures: September WTI crude oil (CLU5) ended another choppy week $1.30 lower at $66.05. August gold also (GCQ5) extended its consolidation, falling $5.70 to $3,358.30 last week. Biggest gains: July ether (ETHN5) +18.8%, September orange juice (OJU5) +10.3%. Biggest losses: September cocoa (CCU5) -4.6%, September hard red wheat (KWU5) -3.7%.

Coming this week

This week’s numbers include:

●Monday: Leading Economic Indicators Index

●Wednesday: existing home sales

●Thursday: Chicago Fed National Activity Index, S&P Global Manufacturing and Services PMIs (flash), new home sales

●Friday: durable goods orders

The first full week of earnings season includes Alphabet (GOOGL) and Tesla (TSLA), alongside a busy lineup of high-profile consumer, aerospace and defense, and tech names. Highlights:

●Monday: Domino's Pizza (DPZ), Infosys (INFY), Medpace (MEDP), NXP Semiconductors (NXPI), Verizon (VZ), Wintrust (WTFC)

●Tuesday: Cal-Maine Foods (CALM), Enphase Energy (ENPH), Fiserv (FI), General Motors (GM), Halliburton (HAL), Coca Cola (KO), Lockheed Martin (LMT), Northrop Grumman (NOC), Texas Instruments (TXN)

●Wednesday: Freeport McMoRan (FCX), Chipotle Mexican Grill (CMG), General Dynamics (GD), Alphabet (GOOGL), International Business Machines (IBM), Southwest Airlines (LUV), Mattel (MAT), O'Reilly Automotive (ORLY), QuantumScape (QS), Tesla (TSLA)

●Thursday: American Airlines (AAL), Aon (AON), AT&T (T), Boyd Gaming (BYD), Colgate-Palmolive (CL), Dover (DOV), Honeywell (HON), Intel (INTC), Keurig Dr. Pepper (KDP), Union Pacific (UNP), Verisign (VRSN)

●Friday: Centene (CNC), HCA Healthcare (HCA), Phillips 66 (PSX), Saia (SAIA)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

The dollar and the stock market

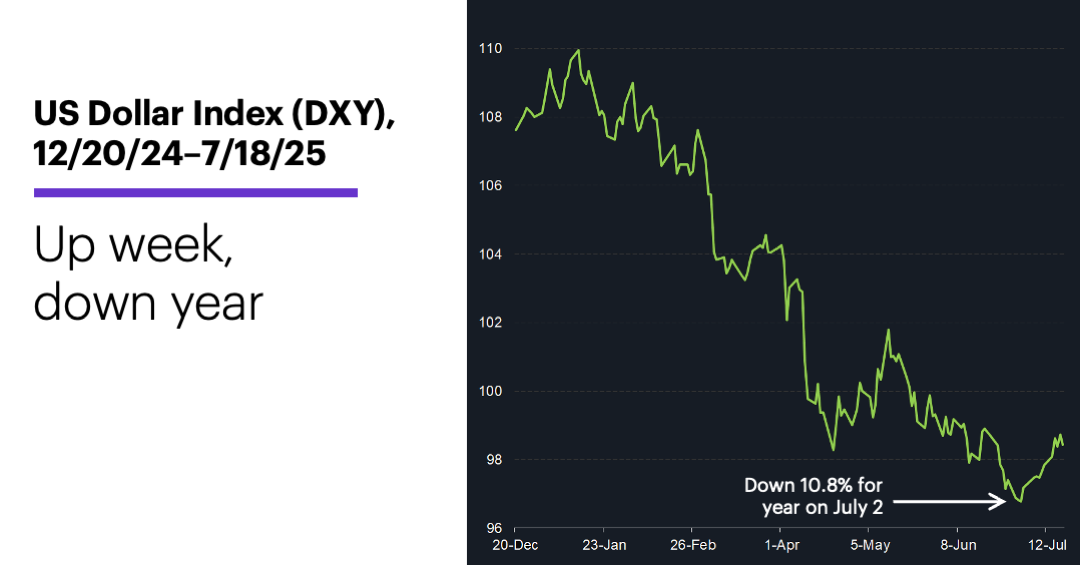

Although it’s been overshadowed by the stock market’s spring sell-off and return to new highs, the US dollar has been one of 2025’s more interesting market stories.

As of Friday, the US Dollar Index’s (DXY) was enjoying its second-largest upswing of the year—a 1.71 gain since July 2 that trails only the 3.51 rise from April 21 to May 12. Nonetheless, the DXY was still down more than 9% for the year, and has closed lower six months in a row—the longest such run since 2017:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.))

If the longer-term dollar-weakness trend continues, as Morgan Stanley & Co. analysts expect it could, the implications extend far beyond the currency market. As the strategists note, in an environment characterized by rising currency volatility and elevated macroeconomic uncertainty, companies with significant currency exposure could be more vulnerable than those with lower exposure.

Specifically, they note companies with low currency-risk exposure tend to be more insulated from “global macro shocks,” which have not been in short supply so far this year.1 Their research includes lists of US, European, and Japanese stocks with the lowest currency exposure.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Quant Matters—Introducing Low FX Sensitivity Factor Amid USD Weakness. 7/11/25.