Bulls get follow-through rally

- Small caps lead as stocks set fresh records

- Jobs report surprises to upside

- This week: FOMC minutes, inflation expectations

The S&P 500 (SPX) started last week by wrapping up its strongest two-month rally since December 2023. It ended it with a fresh record high, as Thursday’s jobs report came in stronger than expected and Congress passed the White House’s tax and spending bill by the July 4 target date.

The SPX set new all-time highs on three of the holiday-shortened week’s four trading days—including Wednesday, when the ADP private employment report showed a surprise loss of jobs last month, and set up expectations for a soft monthly jobs report on Thursday:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Second week of record highs for US stocks.

The fine print: The upshot of Thursday’s robust jobs report was that it appeared to dash hopes that the Fed would possibly cut interest rates at its next meeting in late July. Shortly after the numbers were released, the market-based odds of a cut dropped below 5%.1

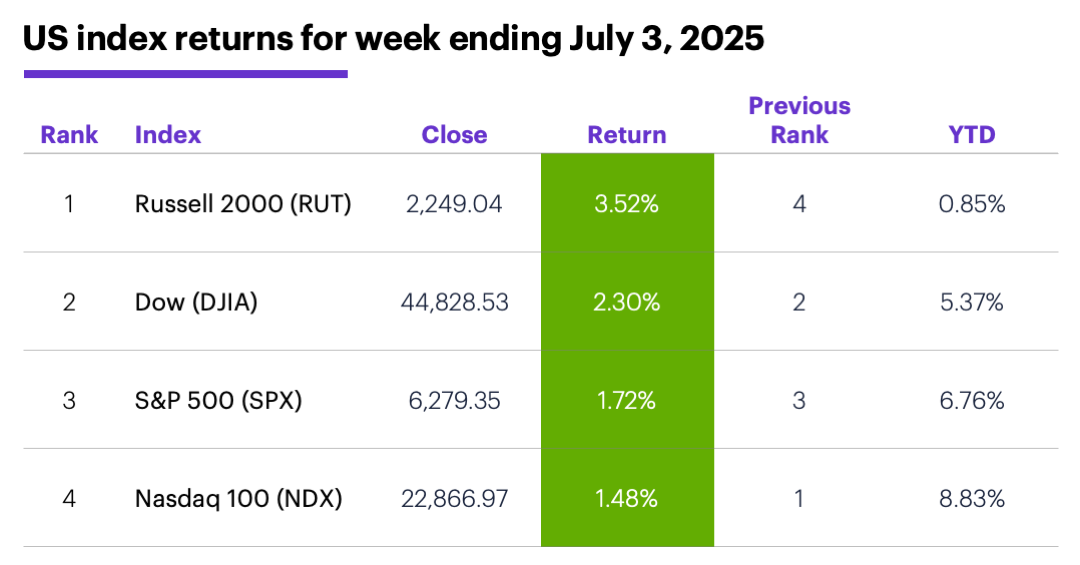

The number: 20, the number of weeks since the Russell 2000 (RUT) small-cap index last ended a week in positive territory for the year.

The scorecard: The RUT led the market, while the Nasdaq 100 (NDX) tech index lagged it—although it’s still ahead of the pack for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were materials (+3.7%), tech (+2.4%), and financials (+2.4%). The weakest sectors were communication services (-0.2%), utilities (+0.6%), and consumer discretionary (+0.8%).

Stock moves: Newegg (NEGG) +34% to $16.24 on Monday, Eyenovia (EYEN) +50% to $15.82 on Wednesday. On the downside, Centene (CNC) -40% to $33.78 and Regencell Bioscience (RGC) -29% to $10.36, both on Wednesday.

Yields: After falling to its lowest low since May 1 last Tuesday, the benchmark 10-year Treasury yield pivoted to end the week up 0.07% to 4.35%.

US dollar: The US Dollar Index (DXY) extended its slide, falling 0.22 to 97.18 last week.

Futures: August WTI crude oil (CLQ5) recovered a small portion of the previous week’s sell-off, climbing $1.40 to $66.92. Despite tagging a five-week low last Monday, August gold (GCQ5) reversed to end the week up $56.40 at $3,344.

Coming this week

This week’s number include:

●Tuesday: NFIB Business Optimism Index, consumer inflation expectations

●Wednesday: FOMC minutes

●Thursday: weekly jobless claims

This week’s earnings include:

●Monday: Corning (GLW)

●Tuesday: Penguin Solutions (PENG)

●Wednesday: AZZ (AZZ), Kalvista Pharmaceuticals (KALV)

●Thursday: Conagra (CAG), Delta Air Lines (DAL), Levi Strauss (LEVI), PriceSmart (PSMT)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Record highs +5 (days)

Last Thursday marked the fifth trading day since the SPX first traded to a new (intraday) record high on June 26. Its 2.2% gain since then was the second-strongest five-day gain of the 13 other times the index pushed to a new record high after falling into a correction. (The strongest was the 2.3% gain in 1990.)

The next five trading days (i.e., this week) were a bit softer, on average. Ten days after the SPX initially hit a new record high, the index was lower in seven of 13 cases.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 CMEgroup.com. FedWatch Tool. 7/3/25.