Market warms to cooling inflation

- Stocks hit records, bond yields fall as inflation cools

- Tech leads rally, gold and copper hit all-time highs

- This week: FOMC minutes, more retail earnings

There may still be debate about when the Fed will start cutting interest rates, but last week the stock market appeared to be pleased about the way the numbers were trending.

The S&P 500 (SPX) stalled a little toward the end of the week, but a solid Tuesday-Wednesday rally following cooler-than-expected inflation readings from the Producer Price Index (PPI) and the Consumer Price Index (CPI) propelled the index to record highs and a fourth-straight up week:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Record highs for S&P 500 and Nasdaq amid “Goldilocks” economic signals.

The fine print: Last Wednesday’s CPI was the week’s big number, but other data also indicated the US economy slowed recently, including soft retail sales, fewer housing starts, and falling industrial production. But the numbers suggested cooling, not a freeze—i.e., enough to keep hope for Fed rate cuts alive, but not enough to trigger concerns the economy is grinding to a halt. Morgan Stanley & Co.’s baseline forecast is for the Fed to cut rates at its September meeting.1

The moves: Last Wednesday the 10-year Treasury yield closed at its lowest level (4.36%) since April 4. But it pivoted higher on Thursday and ended the week only modestly lower at 4.42%. Meanwhile, on Friday the Cboe Volatility Index (VIX) closed at its lowest level since December 15.

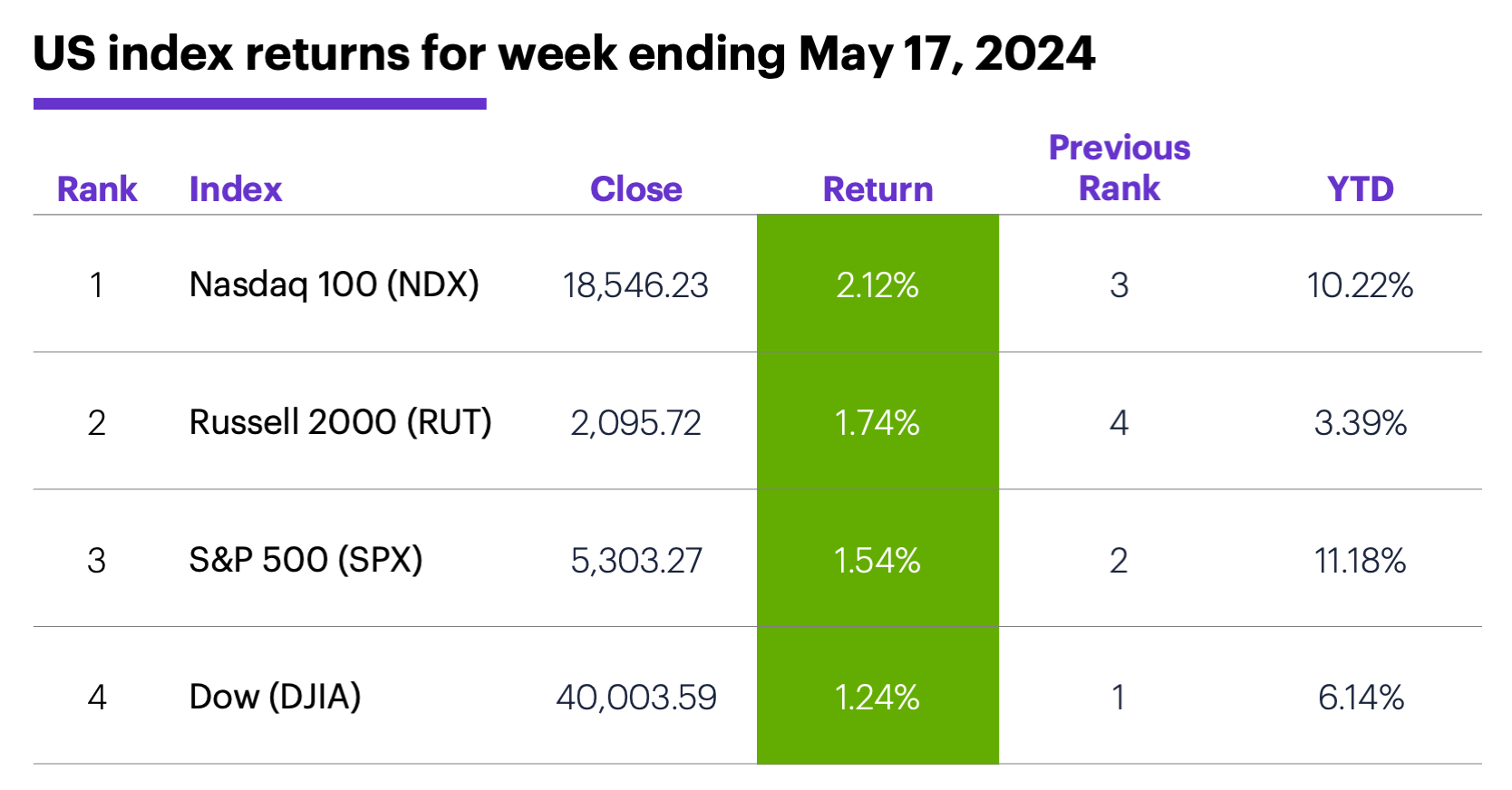

The scorecard: Except for the Russell 2000, all the major indexes hit record highs last week. The Nasdaq 100 (NDX) tech index led the market, while the Dow Jones Industrial Average (DJIA) topped 40,000 for the first time:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were information technology (+2.9%), real estate (+2.4%), and health care (+1.8%). The weakest sectors were industrials (-0.5%), consumer discretionary (-0.3%), and materials (+0.1%).

Stock movers: GameStop (GME) +74% to $30.45 on Monday and +60% to $48.75 on Tuesday (then -19% to $39.55 on Wednesday, -30% to $27.67 on Thursday, and -20% to $22.21 on Friday), Novavax (NVAX) +48% to $13.11 on Monday. On the downside, DLocal (DLO) -26% to $10, and Virtra (VTSI) -30% to $11.51, both on Wednesday.

Futures: After hitting a two-month intraday low of $76.70 last Wednesday, July WTI crude oil (CLN4) closed Friday at a more than two-week high of $79.58. June gold (GCM4) rallied more than $40 last week, closing Friday at a new record high of $2,417.40. Week’s biggest gainers: July orange juice (OJN4) +13.8%, July natural gas (NGN4) +12.6%. Week’s biggest decliners: July cocoa (CCN4) -17.4%, July oats (ZON4) -11.1%.

Coming this week

This week traders will get a look at the minutes from the April 30-May 1 Fed meeting, Durable Goods Orders, and the latest home price data:

●Tuesday: Cleveland Fed President Loretta Mester, Atlanta Fed President Raphael Bostic, and Boston Fed President Susan Collins panel discussion

●Wednesday: Existing Home Sales, FOMC minutes

●Thursday: Chicago Fed National Activity Index, S&P Global Manufacturing and Services PMIs (flash), New Home Sales

●Friday: Durable Goods Orders, Consumer Sentiment

Retail dominates the earnings calendar for a second week:

●Monday: Global-E Online (GLBE), Wix.com (WIX), Keysight (KEYS), Palo Alto Networks (PANW), Zoom Video (ZM)

●Tuesday: AutoZone (AZO), Eagle Materials (EXP), Lowe's (LOW), Macy's (M), Williams-Sonoma (WSM), Toll Brothers (TOL), Urban Outfitters (URBN)

●Wednesday: Analog Devices (ADI), Dycom (DY), Target (TGT), TJX (TJX), Nvidia (NVDA), Snowflake (SNOW)

●Thursday: BJ's Wholesale (BJ), Medtronic (MDT), NetEase (NTES), Ralph Lauren (RL), Intuit (INTU), Ross Stores (ROST), Workday (WDAY)

●Friday: Booz Allen Hamilton (BAH)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Dow by the numbers

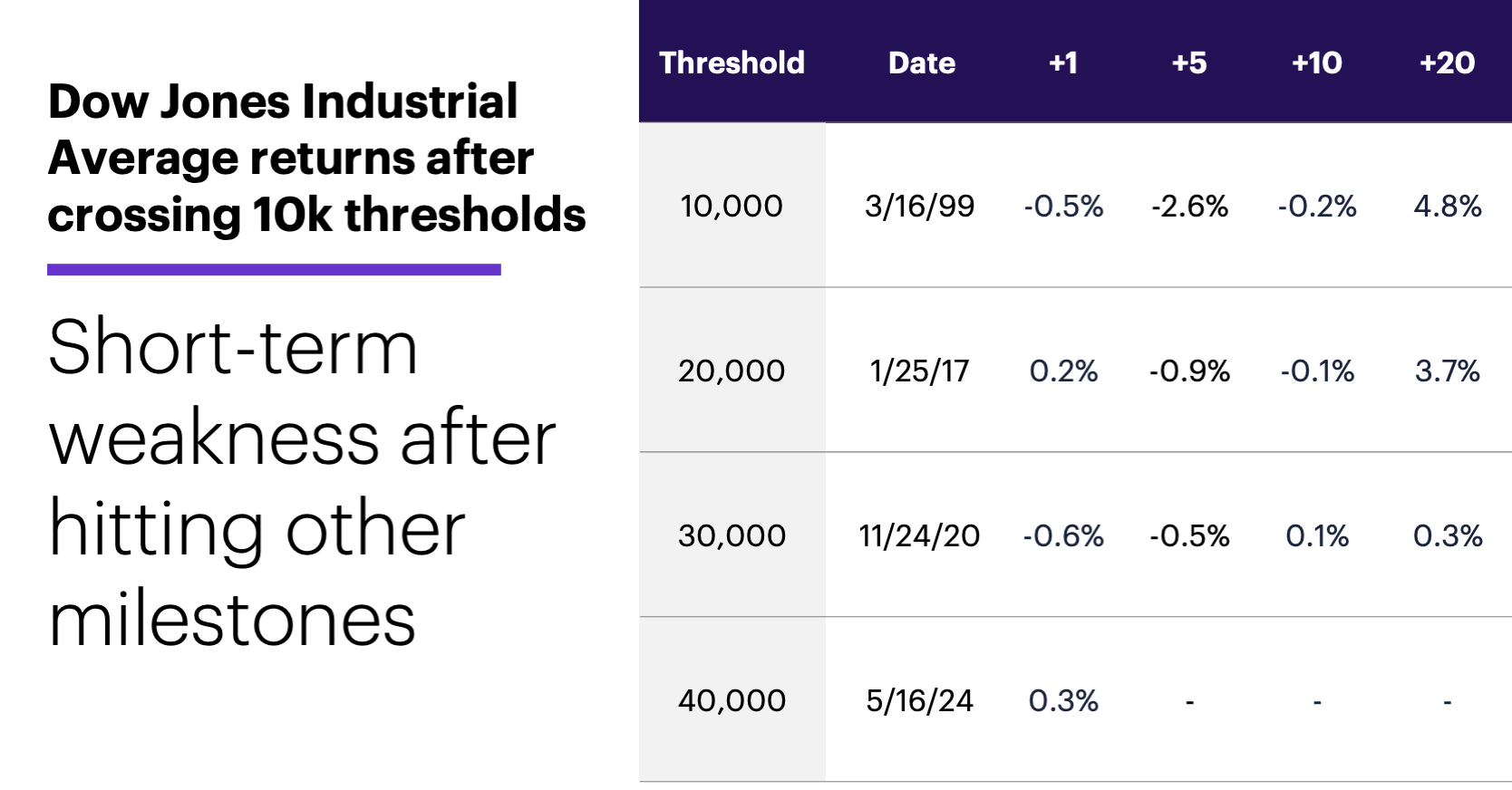

The Dow first topped 1,000 in November 1972. It took nearly 27 years for it to hit 10,000 (in March 1999), nearly 18 years to rally to 20,000 (in 2017), less than four to top 30,000 (in 2020), and just three-and-a-half to tag 40,000.

Here’s what the Dow did one-, five-, 10-, and 20 trading days after first trading at or above its past three 10k thresholds:2

Data source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

While it’s unwise to read much into less than a handful of examples, Friday’s modest stock market gains were actually better than the Dow’s tepid short-term performance after hitting the previous milestones. The index closed lower the next day two of three times, was lower after five trading days in all three instances, and was negative two of three times after 10 trading days. But after 20 trading days, the Dow was higher in all three instances.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Watch for a September Rate Cut. 5/15/24.

2 All figures reflect Dow Jones Industrial Average (DJIA) daily prices, 1999-2024. Supporting document available upon request.