Can target-date funds help you retire on time?

Morgan Stanley Wealth Management

06/26/25Summary: For investors who prefer not to reassess and tweak their retirement portfolios periodically, target-date funds may be an effective way to manage the risk of large swings in return.

To take the guesswork out of investing, many investors pour their retirement savings into a diversified portfolio, with allocations to funds comprised of stocks, bonds and cash. Doing so is easy, but it carries a downside: If you don’t monitor your investments periodically and adjust the allocations, you can find yourself overexposed to risk.

"People own those portfolios for years and sometimes never get away from them," says Robert Garcia, Chief Operating Officer of the Morgan Stanley Pathway Funds and Morgan Stanley Pathway Retirement Target Date Portfolios.

The best practice in such situations would be to periodically rebalance your holdings. But if you would rather not reassess and tweak your retirement portfolio regularly, target date portfolios may be a more effective way to invest. These portfolios consider the year in which you plan to retire and reduce your exposure to riskier investments as you near that date, helping limit the chance a market shock wipes out a substantial portion of your portfolio as you're getting ready to cash out.

How target-date funds work

The goal of target-date fund is to allow investors to get the benefits of age-appropriate diversification without the manual work of adjusting their investments manually as they get older. A fund targeted for a younger investor—shooting to retire in, say, 2055—might allocate between 96% to 76% of holdings in equities, while those nearing retirement might have a more conservative portfolio, holding, say, 40% in stocks.

Over time, the target-date fund automatically shifts its investment mix to become more conservative as retirement approaches.

"Instead of trying to understand what your risk level should be for your whole life cycle, target date portfolio will adjust automatically on your behalf," says Garcia.

Like other investments, there are several different versions of target-date funds, including those that are actively or passively managed, or a combination of both.

Target date portfolios can also be open or closed architecture. Meaning, some managers stock their target date portfolios with only their own proprietary products (closed), while others, have no such restrictions (open).

Managing large swings in returns

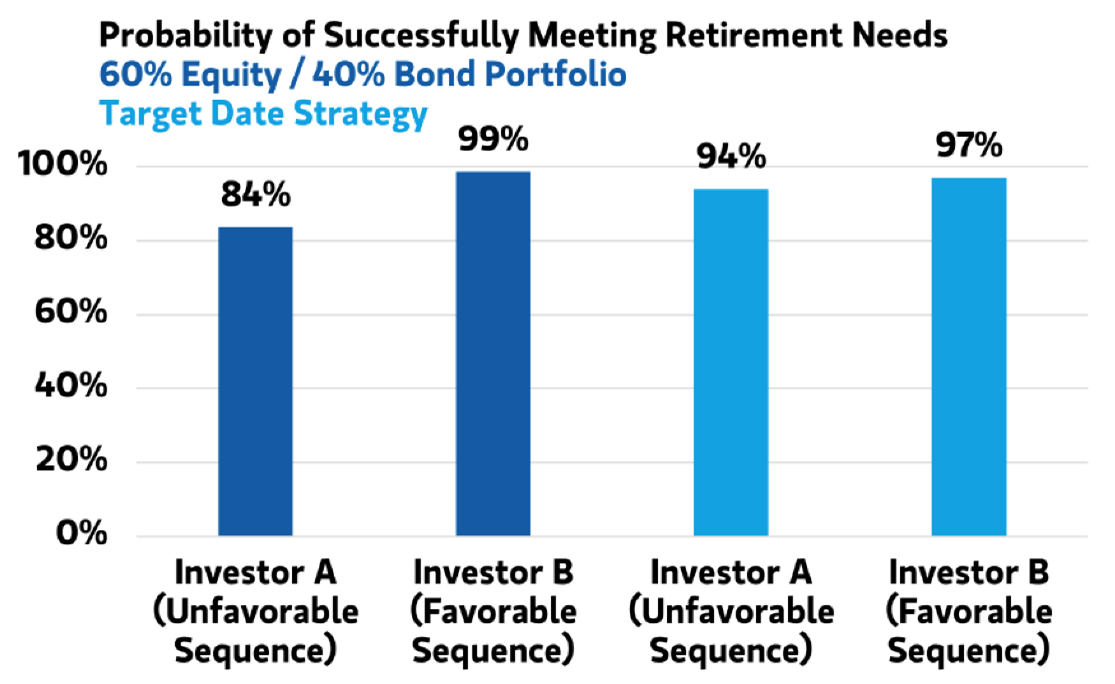

One of the main benefits of target-date funds may be how it handles one of the biggest risks to a retirement portfolio, the risk that poor performance during the first decade of retirement can have a detrimental long-term impact on the returns of the portfolio for decades to come, also known as sequence of returns risk. Consider how two portfolios—one using a balanced fund with a static 60% equity and 40% bond allocation, the other using a target-date fund—might fare under the following two circumstances for two investors, Investor A has a balanced portfolio and investor B uses a target-date fund.

One of the main benefits of a target-date fund may be how it handles one of the biggest risks to a retirement portfolio - the risk that poor performance while saving for retirement can have a detrimental long-term impact for decades to come.

Scenario one reflects actual historic returns: there's a decade of poor market performance (the 1970s), followed by 20 years of good market performance (1980s and 1990s) and then a decade of terrible market returns (2000s).

Scenario two assumes a different order of events: The worst returns happen during the first decade, followed by 1970s-like returns the following decade, and ending with the best returns during the last two decades. While the two scenarios produce the same average returns, the outcomes for Investor A and Investor B are significantly different.

Impact of Sequence of Return on Two Different Retirement Strategies

Note: For illustrative purposes only. See endnotes for assumptions and further details. Source: Morgan Stanley Wealth Management Global Investment Office

In a balanced portfolio (Investor A) the difference in the final portfolio value could vary vastly from scenario one, where the worst performance happens later in the investment period, to scenario two, where it happens early on.

On the other hand, the final value of a target-date fund (Investor B) may be considerably less affected from one scenario to the other. In practical terms, this could mean that if a market shock occurs later in life, investing in a target-date fund versus a balanced portfolio could be the difference between having enough money during retirement and falling short.

Finding a target-date fund with E*TRADE is simple

- Search all target date ETFs available through E*TRADE (choose ‘Life Cycle’ in the Fund Category)

- Search all target date mutual funds available through E*TRADE (choose ‘Life Cycle’ in the Fund Category)

How can E*TRADE from Morgan Stanley help?

Retiring on target

Find target date funds—ETFs that are designed to help reduce your exposure to riskier investments as your retirement date approaches.

Traditional IRA

You may be eligible to make income tax deductible contributions

Earnings potentially grow tax-deferred until you withdraw them in retirement.

Plan for your future

Explore easy-to-use planning tools and resources—designed to help you take control of your financial future.

Risk Assessment Tool

How risky is your portfolio?

Understanding risk is key to managing your investment performance. See your portfolio’s volatility, asset allocation and how you might fare in different hypothetical market scenarios.