What is a bond?

E*TRADE from Morgan Stanley

02/28/25Summary: Bonds offer steady income and diversification. Learn more about bonds and why investors find value in adding them to their investment strategies.

Along with stocks, ETFs, and other types of investments, bonds are a cornerstone of many portfolios. For some investors, bonds offer the opportunity to diversify, earn steady income, and add stability to investments, especially in times of high volatility.

What is a bond?

A bond is a fixed-income security that is a type of loan where you lend money to an issuer for a limited period, in exchange for receiving regular interest payments until the loan’s maturity date.

Bonds are typically issued by federal, state, or local governments, and corporations to either raise money to fund government projects or to fulfill business needs. As an issuer, an entity may borrow hundreds of millions of dollars at a time, so the principal is divided into units that is usually in the amount of $1,000 each.

There are multiple types of bonds that can potentially complement your investing strategies, and help you reach your financial goals while still being relatively low risk.

Here are some key terms to know before you begin researching bond investments:

- An issuer: The entity that borrows the money by issuing the bond. An issuer could be the United States government, a state or municipality, or a corporation.

- Principal: The face value of the bond. It is the amount of money that the issuer is borrowing.

- Maturity date: The due date when the issuer must repay the principal loan amount and any remaining interest to the bondholder. Once a bond is issued, its maturity date can range from a few months to over 30 years.

- Interest rate, also called coupon rate: The fixed amount the issuer pays for borrowing the money. The interest rate is usually determined at the time the bond is issued, and most interest payments are distributed semiannually with the principal repaid at maturity, along with the final interest payment. The rate of interest you earn on your bond depends on the price you pay for the bond when you buy it.

Understanding yield

The yield represents an investor’s return on the bond, conveyed as an annual percentage.

Important yield terms:

Current yield (CY)

The annual rate of return on the bond. It can change based on whether the bond was bought at a discount, at par, or at a premium.

- When purchased at a discount, the current yield is higher than the coupon rate.

- When purchased at par, the current yield is equal to the coupon rate.

- When purchased at a premium, the current yield is lower than the coupon rate.

Yield to maturity (YTM)

The expected yield if the bond is held to maturity.

- When purchased at a discount, the yield to maturity is higher than the coupon rate and current yield.

- When purchased at par, the yield to maturity is equal to the coupon rate.

- When purchased at a premium, the yield to maturity is lower than the coupon rate and current yield.

Yield to worst

The bond’s lowest possible yield if the issuer does not default but the bond is retired before its maturity date. Allows the issuer to avoid some interest payments.

Yield to call (YTC)

The total return if the bond is held only until its call date. A call date is the most common provision that lets an issuer to retire a bond early—i.e. pay the bond’s face value to the bond holder before the maturity date.

Holding bonds vs. trading bonds

When investing in bonds, you have the option to either keep them until maturity or trade them on the secondary market.

- Holding bonds: Bondholders who hold on to their bonds until the maturity date can expect steady income and their principal investment back once the loan ends.

- Trading bonds: Bondholders who buy and sell on the secondary market often try to profit from price fluctuations.

It’s important to note that after a bond is issued, the first buyer can resell it or trade it on what’s known as the secondary market. In fact, most investors buy bonds on the secondary market, not from the original issuer.

If you purchase a bond on the secondary market, the price may be dictated by many factors, including interest rates, market sentiment, macroeconomic conditions, perceived credit risk of the issuer, liquidity, and general supply and demand in the market for that bond.

Bond purchase options

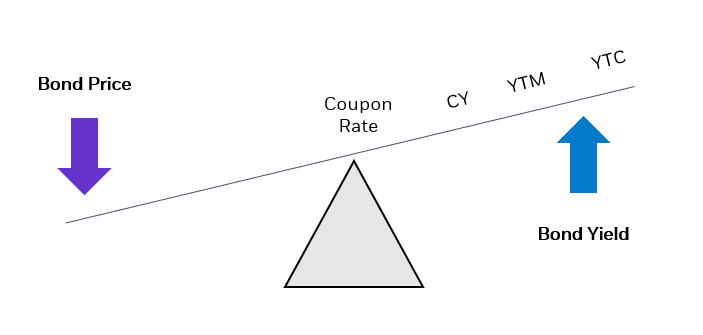

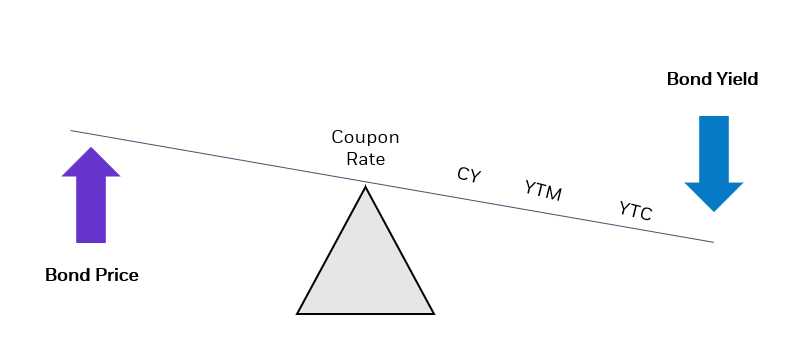

A bond's yield moves inversely with the bond's price like the see-saw diagrams show below.

A bond at par also known as a bond at face value.

Example: $1000 bond purchased for $1000 |

When interest rates are stable, the bond will continue to trade at par.

|

A bond at discount

Example: $1000 bond purchased for $980 |

When interest rates go up, the price of the bond goes down.

|

A bond at premium

Example: $1000 bond purchased for $1050 |

When interest rates go down, the price of the bond goes up.

|

Next steps in bond investing

There are many reasons to invest in bonds. Most bonds are generally considered safer than stocks. Adding even a small amount of bonds to your mix of investments can help you diversify and significantly reduce volatility in your portfolio.

In addition, US Treasury and municipal bonds can offer investors potential income tax advantages.

When you’re ready to invest in bonds, you can open and fund a brokerage account and make your purchase. Explore E*TRADE’s comprehensive Bond Resource Center, available post-login, to find user-friendly tools and resources to help you find the bonds you want, according to your risk tolerance.

How can E*TRADE from Morgan Stanley help?

Need help getting started with bonds?

To get started with bonds, visit our comprehensive Bond Resource Center. Use our Advanced Screener to quickly find the right bonds for you. Or call our Fixed Income Specialists at (877-355-3237) if you need additional help.

Brokerage account

Investing and trading account

Buy and sell stocks, ETFs, mutual funds, options, bonds, and more.