Q1 sticks the landing

- Stocks wrap up March, Q1 with more records

- Tech soft, small caps strong, gold above $2,200

- This week: Jobs, manufacturing and services

It was far from an emphatic statement, but bulls still managed to leave their imprint on the final, holiday-shortened week of the first quarter.

While the S&P 500 (SPX) posted its smallest weekly gain of the year, it was also the 18th up week of the past 22 and the 11th-straight week with a new record daily high or close. The SPX also wrapped up a fifth-consecutive up month, its 10th-strongest five-month return since 1957, and its best Q1 return (10.2%) since 2019:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: S&P 500 wraps up Q1 with more records.

The fine print: The SPX ending Q1 ahead of the Nasdaq 100 (NDX) tech index is hardly evidence of a sea change, but Morgan Stanley & Co. strategists recently noted signs of improving market breadth in sectors other than tech. They argue a sustained broadening of the market rally will require earnings growth from stocks other than the mega-cap names that have driven index gains in recent months. Two possibilities: industrials, which could benefit from fiscal spending and AI-driven data center buildout, and energy, which they describe as “one of the cheapest and most under-owned areas of the market.”1

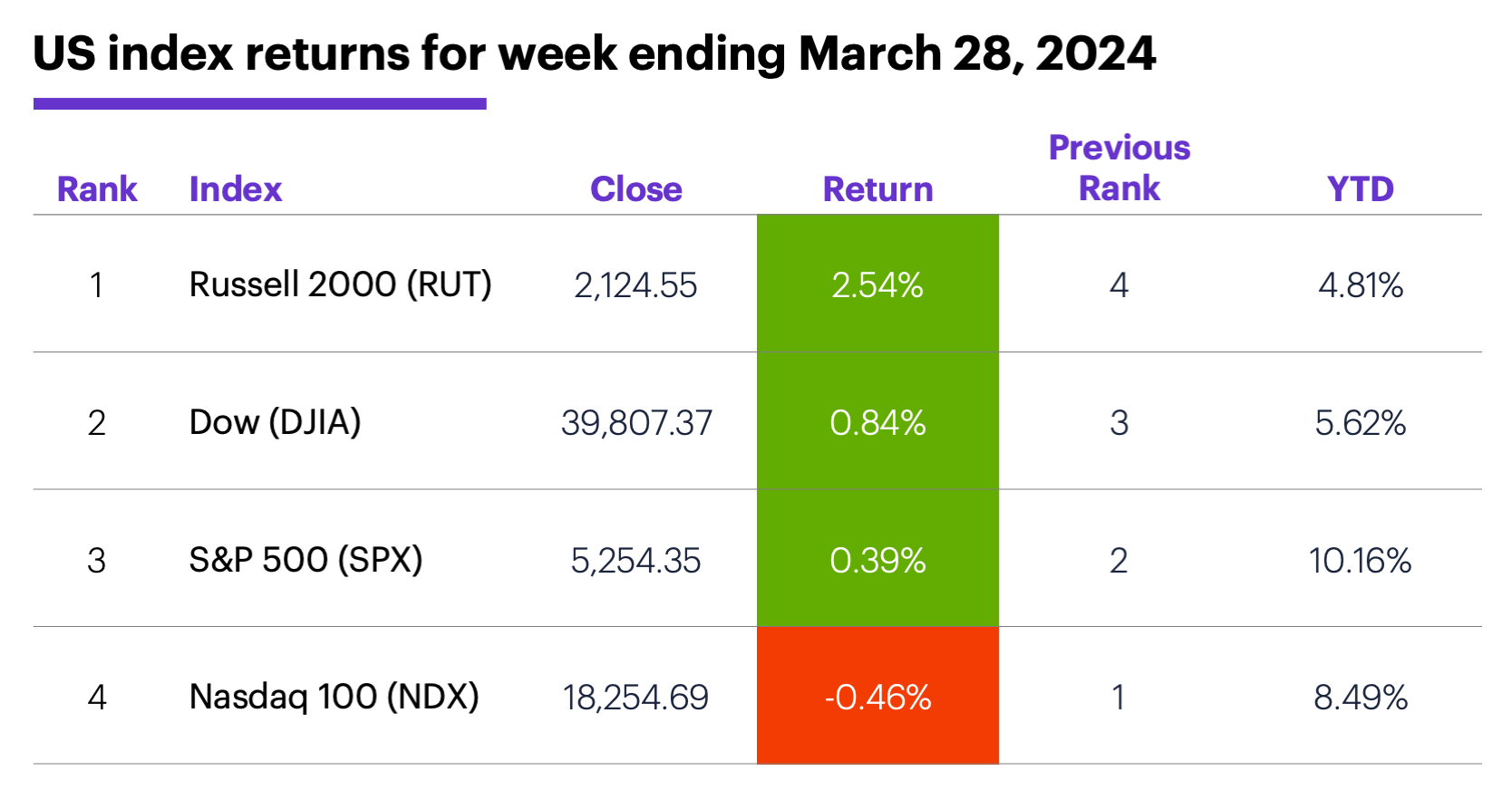

The scorecard: The Russell 2000 (RUT) small cap index led the market:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were utilities (+2.8%), real estate (+2.23%), and energy (+2.21%). The weakest sectors were industrials (+0.60%), communication services (-0.8%), and information technology (-1.3%).

Stock movers: Krispy Kreme (DNUT) +39% to $17.35 on Tuesday, Stoke Therapeutics (STOK) +38% to $14.17 on Wednesday. On the downside, Aehr Test Systems (AEHR) -22% to $11.37 on Monday, Cardlytics (CDLX) -33% to $13.60 on Tuesday (after rallying 27% on Monday).

Futures: June gold (GCM4) rallied every day last week, closing Thursday at a new all-time high of $2,227.10. May WTI crude oil (CLK4) ended a choppy week at a five-month high of $83.17. Cocoa prices hit $10,000/ton for the first time last week, and May Cocoa (CCK4) closed Friday at $9,766, up more than 12% for the week.

Coming this week

Plenty of nuts-and-bolts economic data will hit the Street before Friday’s jobs report:

●Monday: S&P Global Manufacturing PMI, ISM Manufacturing Index, Construction Spending

●Tuesday: Factory Orders, Job Openings and Labor Turnover Survey (JOLTS), vehicle sales

●Wednesday: ADP Employment, S&P Global Services PMI, ISM Services Index

●Thursday: Job Cuts, Trade Balance

●Friday: Employment Report, Consumer Credit

This week’s earnings include:

●Monday: PVH Corporation (PVH)

●Tuesday: Cal Maine Foods (CALM), Dave & Buster’s (PLAY)

●Wednesday: Acuity Brands (AYI), Levi Strauss (LEVI)

●Thursday: Conagra (CAG), Lamb Weston (LW), RPM (RPM), Kura Sushi (KRUS)

●Friday: Ermenegildo Zegna (ZGN)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Pivoting from Q1 to Q2

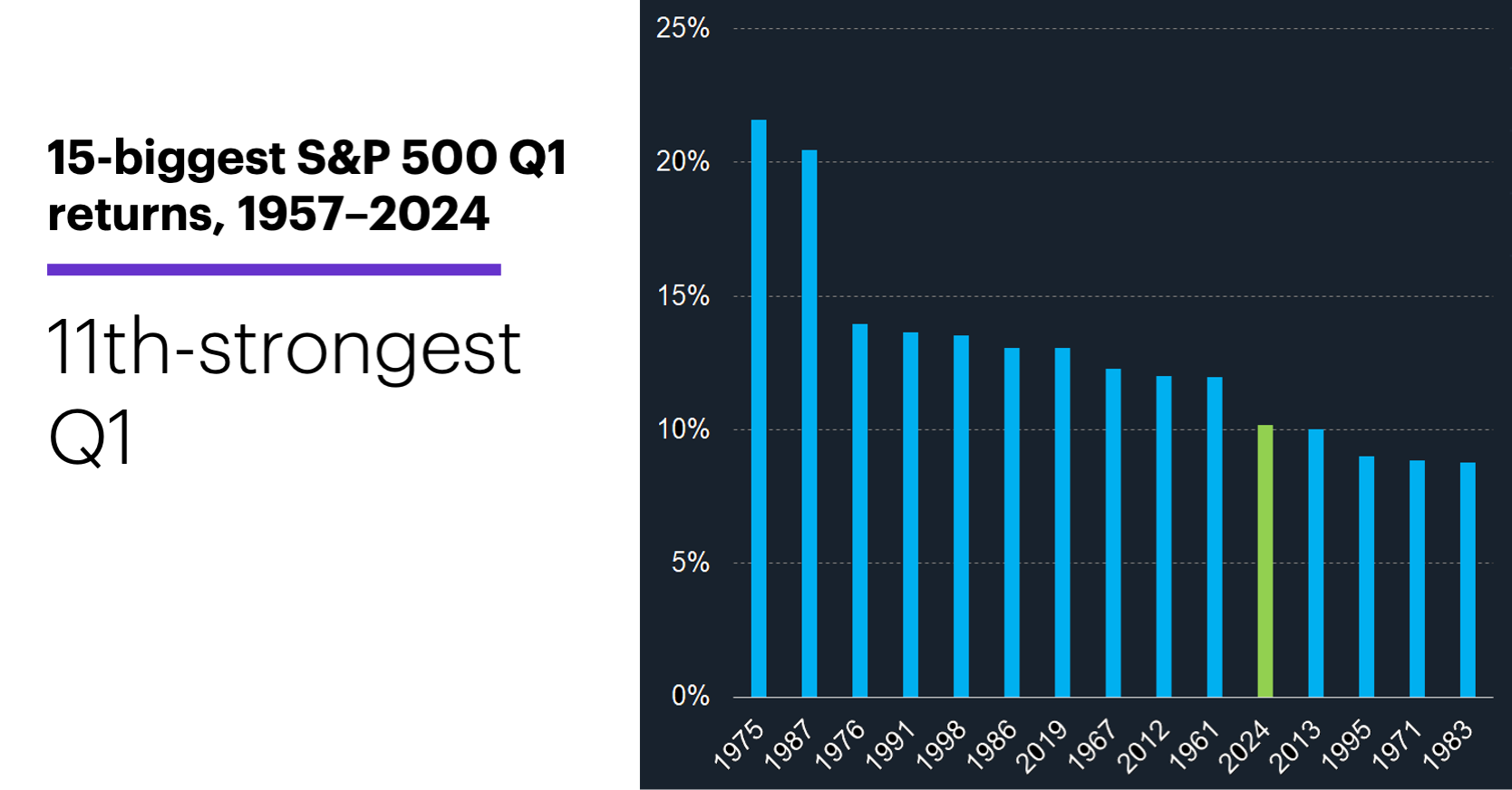

The rest of 2024 clearly has a tough act to follow. Not only was the SPX’s 25.3% gain since the end of October its 10th-strongest five-month rally since 1957, only 10 other Q1s have been stronger over the past 67 years:

Data source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

Such performance will likely—and understandably—incline some traders to argue the market is “overdue” for a pullback. In the past, though, stronger-than-average Q1s haven’t necessarily led to Q2 weakness. The median Q2 return after the strongest Q1s was 2.4%, almost identical to the median return for all other Q2s.2

Finally, April has been one of the most consistent up months for the SPX, with positive returns in 49 of the past 67 years, 24 of the past 30, and nine of the past 10. However, it’s 1.2% median return is only the sixth-strongest out of all months of the year, and it was only 0.9% after the strongest Q1s.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Finding Late-Cycle Winners. 3/26/24.

2 All figures reflect S&P 500 (SPX) weekly closing prices, 1957–2024. Supporting document available upon request.