Stocks stumble on inflation

- Inflation data pushes back rate-cut expectations

- Bond yields surge, gold rally rolls on

- This week: Retail sales, first full week of earnings

Last week again proved that the only certain thing about markets is that they don’t like uncertainty.

This time, mixed inflation data was the trigger. The S&P 500 (SPX) fell to a three-week low last Wednesday after the Consumer Price Index (CPI) surprised to the upside for a third-straight month, then bounced back on Thursday after a cooler reading from the Producer Price Index (PPI).

On Friday, though, the market appeared to decide the CPI was the more relevant of the two, although geopolitical tensions and soft performance from big banks at the outset of earnings season didn’t improve the mood:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Biggest weekly loss of year for S&P 500 amid inflation uncertainty.

The fine print: The odds of a June rate cut, which were above 55% before the CPI report, ended last week below 30%.1

The move: The 10-year-T-note yield surged 183 basis points to 4.55% last Wednesday after the CPI report—its biggest one-day increase since September 2022, and the third-biggest since March 2020.

The number: 2. The SPX posted back-to-back down weeks for just the second time since October.

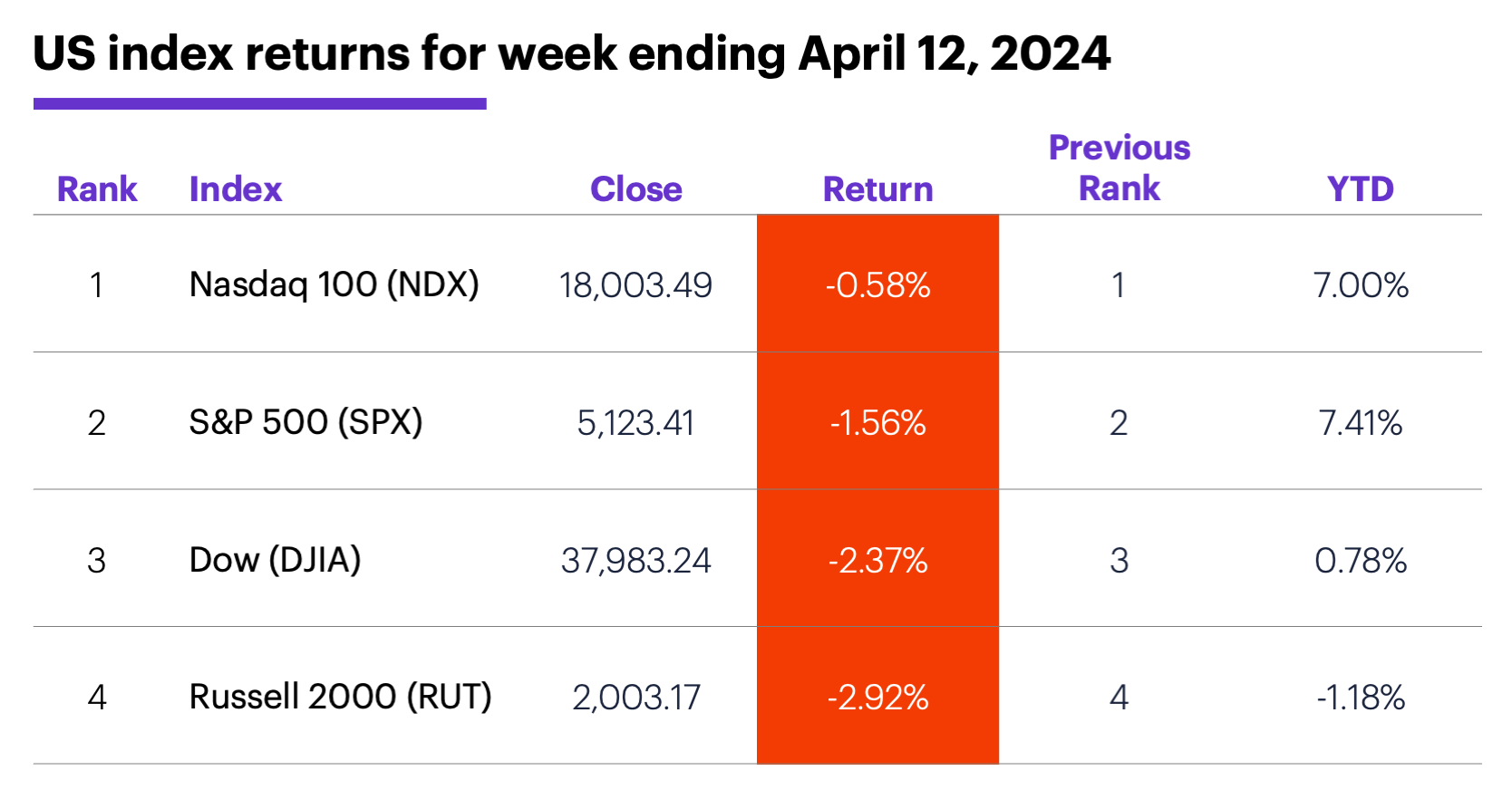

The scorecard: The Nasdaq 100 (NDX) lost the least ground, while the Russell 2000 (RUT) slipped back into negative territory for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were information technology (-0.1%), communication services (-0.5%), and consumer discretionary (-0.8%). The weakest sectors were financials (-3.6%), materials (-3.2%), and health care (-3.2%).

Stock movers: Alpine Immune Sciences (ALPN) +21% to $47.04 on Wednesday and +37% to $64.40 on Thursday, Rent The Runway (RENT) +162% to $19.38 on Thursday. On the downside, Globe Life (GL) -53% to $49.17 and Avita Medical (RCEL) -28% to $10.35, both on Thursday.

Futures: Another milestone for gold, which topped $2,400 for the first time. June gold (GCM4) closed Friday at $2,374.10, after trading as high as $2,448.80 intraday. May WTI crude oil (CLK4) spiked to a new contract high of $87.37 on Friday, but pulled back to end the week with a modest loss at $85.66. Week’s biggest gains: July cocoa (CCN4) +12.5%, April VIX (VXJ4) +8.9%. Week’s biggest declines: July sugar (SBN4) -6.9%, July soybean oil (ZLN4) -6%.

Coming this week

More big banks and other financial companies dominate the first full week of earnings season, but the calendar also includes a few high-profile airline, semiconductor, consumer, oil, and pharma names:

●Monday: Goldman Sachs (GS), FB Financial (FBK)

●Tuesday: Bank of America (BAC), Johnson & Johnson (JNJ), Morgan Stanley (MS), Northern Trust (NTRS), UnitedHealth (UNH), J.B. Hunt Transport (JBHT), United Airlines (UAL)

●Wednesday: Abbott Labs (ABT), Travelers (TRV), US Bancorp (USB), Alcoa (AA), CSX (CSX), Discover Financial (DFS), Kinder Morgan (KMI), Wintrust (WTFC)

●Thursday: Alaska Air (ALK), D.R. Horton (DHI), KeyCorp (KEY), Taiwan Semiconductor (TSM), Netflix (NFLX)

●Friday: American Express (AXP), Fifth Third Bank (FITB), Procter and Gamble (PG), Schlumberger (SLB)

The Retail Sales report and housing numbers highlight the economic calendar:

●Monday: Retail Sales, Empire State Manufacturing Index, Business Inventories, NAHB Housing Market Index

●Tuesday: Housing Starts and Building Permits, Industrial Production, Capacity Utilization

●Wednesday: Fed Beige Book

●Thursday: Philadelphia Fed Manufacturing Index, Existing Home Sales, Leading Economic Indicators

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

28 weeks and counting

Last week may have been the SPX’s second down week in a row—and its biggest weekly loss of the year—but so far the pullback has been far from severe. As of Friday, the SPX was only 2.5% below its March 28 record close—not much more than its December-January 2% pullback, which until last week was the index’s deepest downturn since late October.

Here’s a different way of looking at the market’s current position. Last week was the SPX’s 28th week without three down weeks in a row—its longest run since January 2022, although nowhere near the record of 119 weeks. Since 1957, the SPX has had three or more consecutive down weeks roughly two-and-a-half times a year, on average.2

During that span, the SPX has had 34 other runs of 28 weeks or more without a three-week pullback. As of Friday, the SPX’s 19.5% return since September 29 was the 16th-strongest of these runs. Here’s a breakdown of what the SPX did after the others:

•The run stopped at 28 weeks in only four of the 34 cases. For the other 30, it took anywhere from one to 91 weeks for the index to post three-straight down weeks, and the median wait was 17 weeks.

•The next week was positive 59% of the time with a median return of 0.7% (more than double the SPX’s overall 0.3% one-week return).

•After four weeks the SPX was higher 71% of the time, with a median return of 1.9% (nearly double the SPX’s overall 1% median four-week return).

Strong rallies inevitably increase “the market is due for a correction” chatter, and every pullback can make it feel like that correction has started. But the reality is that it’s impossible to know in real time when a trend will end.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 CMEGroup.com. FedWatch Tool. 4/12/24.

2 All figures reflect S&P 500 (SPX) weekly closing prices, 1957-2024.