Life after a once-in-four-years rally

- S&P 500 rallied nearly 24% since April 4

- Index also closed at all-time high last Thursday

- After rally, short-term weakness followed by strength?

Strong rallies and record highs can fuel optimism, but they can also breed overconfidence and bad trading habits. We’ll only know in retrospect, but the stock market’s recent rally may offer a lesson in why traders and investors are often advised to avoid chasing the market.

At the end of last week, the S&P 500 (SPX) closed at a new record high and was up 23.8% from its close 13 weeks earlier on Friday, April 4:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

To put this move in perspective, the SPX has rallied 23% or more over the course of 13 weeks only 15 other times since 1957, the last time in 2020. But the current move also distinguished itself by virtue of its record high. That combination—a 23%-or-larger gain in 13 weeks coinciding with an all-time high—has never occurred before. Even if we cast a wider net by replacing the all-time high with a more modest 26-week (six-month) high, we find there were only seven other rallies that made the cut.

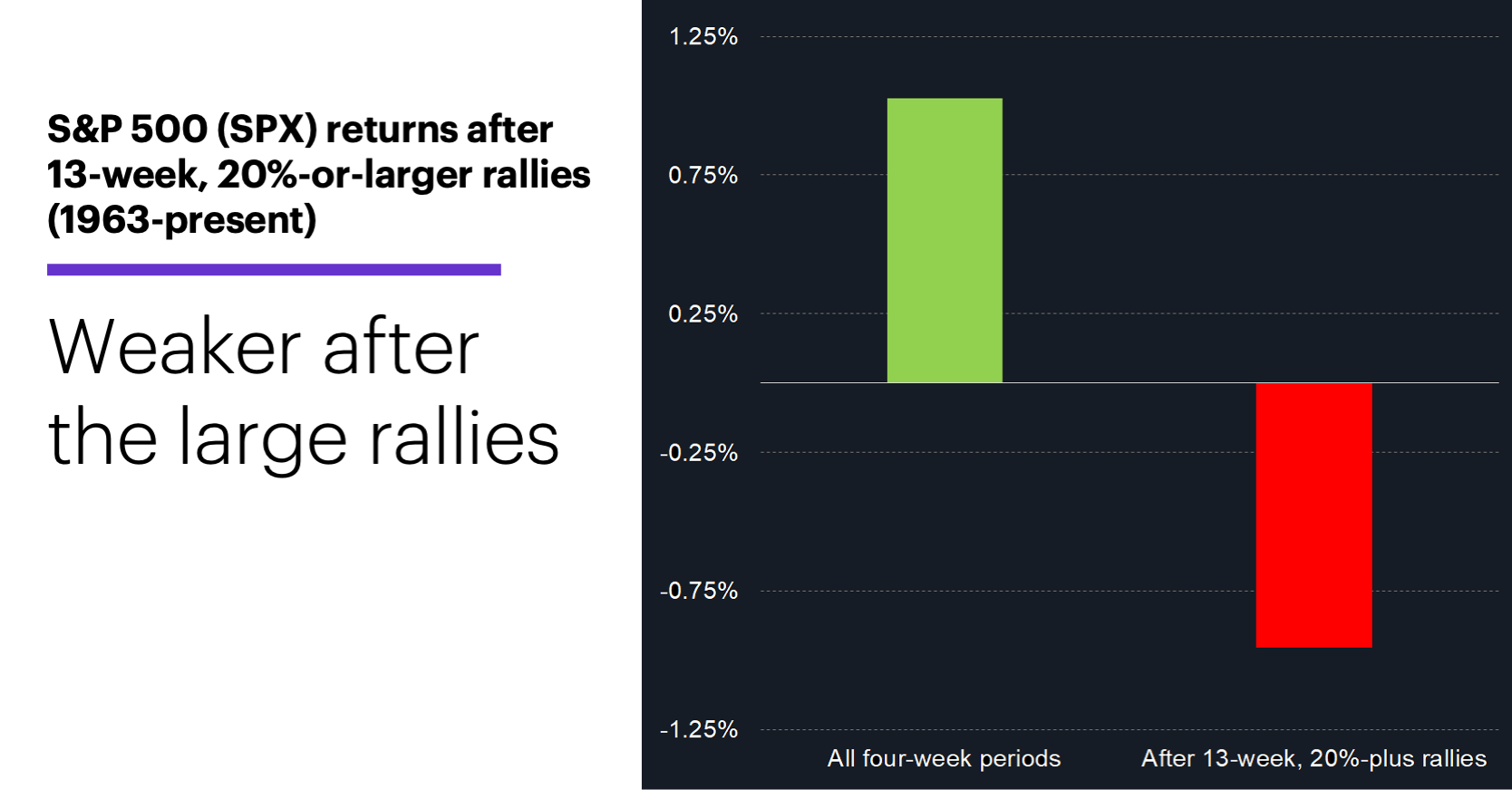

Further widening the net to capture all 13-week, 20%-or-larger rallies that made eight-week (or longer) highs snags 18 previous examples—not a statistically valid sample size, but perhaps enough to begin a discussion. The following chart compares the SPX’s performance after these rallies to its historical benchmark return:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

While the SPX’s median return for all four-week periods was 1.03% (left), the median four-week return after the large 13-week rallies was -0.91%. In fact, the index was lower four weeks later in 12 of the 18 cases (in one instance, it was unchanged).1

Of course, this doesn’t mean the SPX can’t extend its rally in the near term this time—after all, it did so five times before, with a median four-week return of 4.4% and a maximum gain of 8.5%. (The median return for the 12 times it declined was -2.4%.) It’s simply that the historical record shows that, in similar situations, a pullback occurred more often.

The stock market’s longer-term performance after these big rallies was much different than its shorter-term behavior.

The other side of the coin is that on a slightly longer-term basis, the SPX outperformed, on average, after the large rallies. For example, the SPX’s average 26-week (six-month) return since 1957 is 4.1%. The average 26-week return after the large 13-week rallies was 9.2%, and the index was higher at that point in 17 of the 18 cases.

Returning to the near-term horizon, it’s worth noting there was a fairly consistent pattern of short-term underperformance after rallies of this general duration and magnitude. For example, there have been 34 instances of the SPX rallying 17.5% or more in 13 weeks while also closing a two-week (or longer) high. Although the index’s typical short-term performance after these moves was better than that shown in the previous chart, after four weeks the SPX was still lower more often than it was higher. But as a general rule, the bigger the rally, the more significant the average short-term pullback.

That’s just another way of saying that even the strongest trends have pauses and setbacks. History shows that betting against the US stock market in the long term has been a bad idea. But the numbers here also suggest that chasing the market after the type of rally we’ve seen recently isn’t necessarily advantageous, since the more (and longer) the market goes up, the more likely it is to experience one of those pauses or setbacks, even if it eventually resumes its uptrend.

Market Mover Update: Copper prices soared to record highs on Tuesday after the White House announced it planned to implement a 50% tariff on copper imports. September copper futures (HGU5) jumped nearly 18% intraday before closing up 9.9% at 5.501.

Morgan Stanley Wealth Management notes the recently passed tax bill and financial deregulation could produce wide disparities in individual stock performance, creating a “stock picker’s market,” in which investors may benefit from a more targeted, strategic approch.2

Today’s numbers include (all times ET): preliminary wholesale inventories (10 a.m.), EIA Petroleum Status Report (10:30 a.m.), FOMC minutes (2 p.m.).

Today’s earnings include: AZZ (AZZ), Kalvista Pharmaceuticals (KALV).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 All figures reflect S&P 500 (SPX) weekly closing prices, 1957–2025. Supporting document available upon request.

2 MorganStanley.com. It’s a Stock Picker’s Market. 7/2/25.