Stocks experience inflation jitters

- Market stumbles, recovers after hot CPI and PPI data

- Bonds fall as yields jump, 10-year rate near two-month high

- This week: Fed minutes, leading indicators, home sales

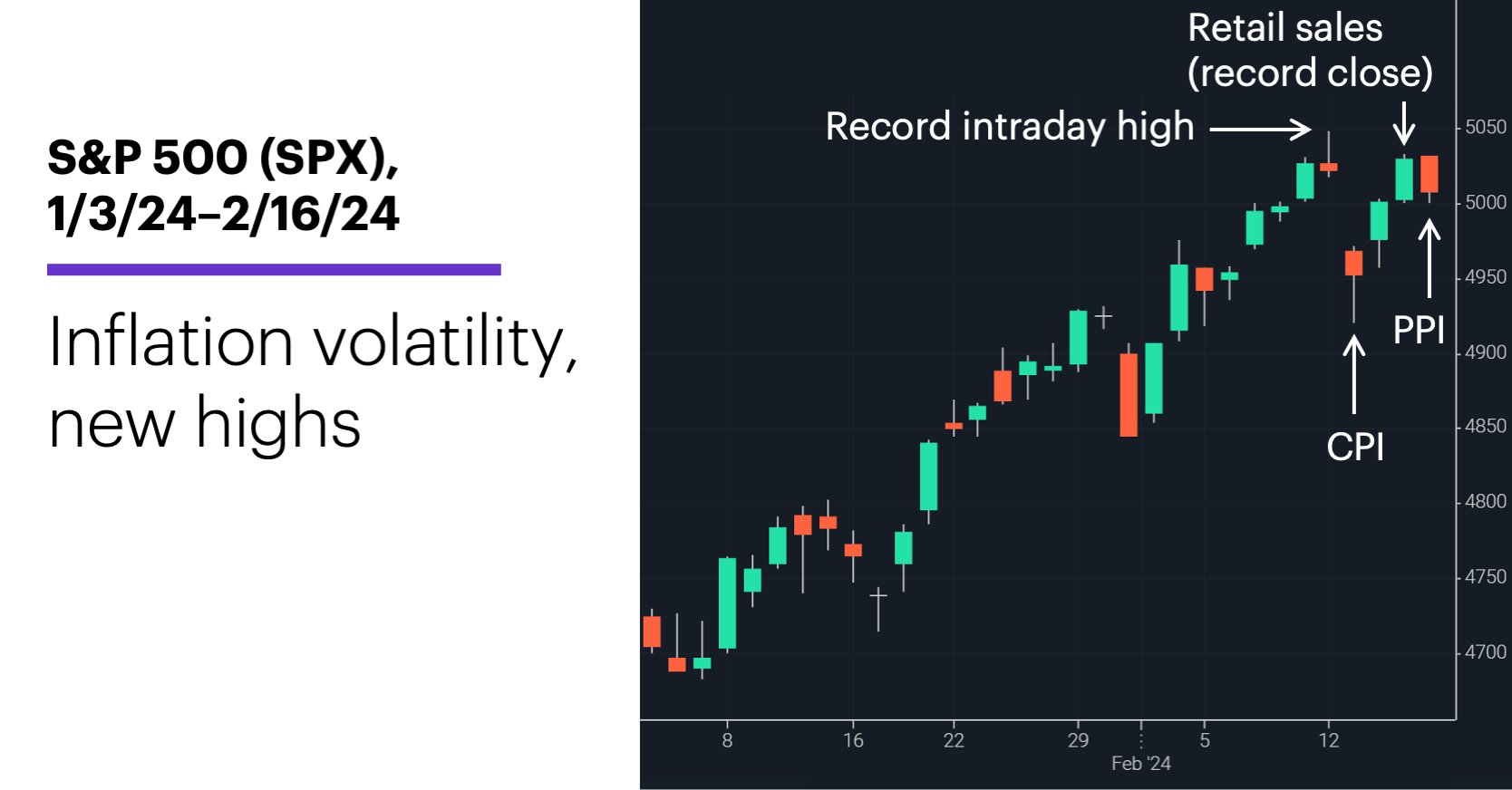

The US stock market set more records last week, but it also posted just its third weekly loss of the past three months, as hotter-than-expected inflation data appeared to give bulls pause about the timing of Fed rate cuts.

The S&P 500 (SPX) kicked off last week by setting a record intraday high, then suffered its second-biggest down day of the year after Tuesday’s consumer price index (CPI) showed inflation crept higher in January. But the SPX bounced back to close at a record high on Thursday, before dipping again on Friday after a similarly warm producer price index (PPI) reading:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Hot inflation cools market—a little.

The fine print: Despite the CPI and PPI surprises, last week hardly painted the picture of a uniformly overheating economy. Two of Thursday’s highest-profile numbers, retail sales and industrial production, came in much weaker than expected.

The move: Last Tuesday the 10-year T-note yield jumped 151 basis points—its second-biggest one-day increase of the past seven months—and closed above 4.3% for the first time since November 30.

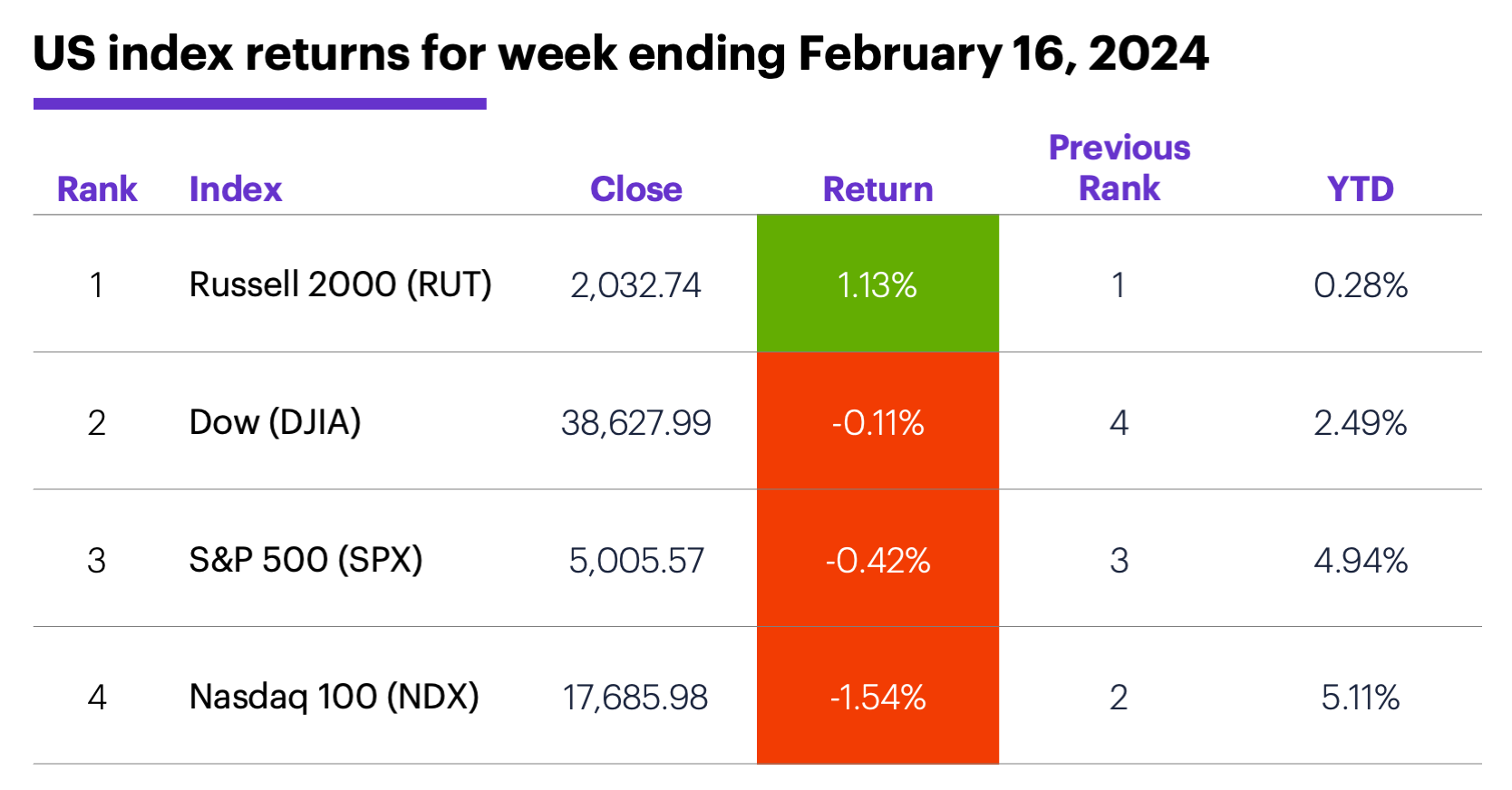

The scorecard: Last Tuesday was the worst day for the Russell 2000 (RUT) since June 2022, but the small cap index was the strongest performer last week, and it pushed back into positive territory for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were materials (+2.4%), energy (+2.2%), and financials (+1.4%). The weakest sectors were information technology (-2.5%), communication services (-1.6%), and consumer discretionary (-0.8%).

Stock movers: Gyre Therapeutics (GYRE) +40% to $14.77 on Wednesday, The Children’s Place (PLCE) +81% to $26.29 on Thursday. On the downside, The Children's Place (PLCE) -31% to $11.29 on Tuesday, QuidelOrtho (QDEL) -32% to $45.27 on Wednesday.

Futures: April WTI crude oil (CLJ4) closed last Friday at $78.27 after spending most of the week consolidating near a three-month resistance level around $78-$79. April gold (GCJ4) tagged a three-month low of $1,996.40 last Wednesday before bouncing to end the week at $2,025.20. Week’s biggest rallies: February micro ether (METG4) +11.7%, March palladium (PAH4) +9.1%. Week’s biggest declines: April natural gas (NGJ4) -10.8%, March ethanol (ZKH4) -7.7%.

Coming this week

This week’s numbers include:

●Tuesday: Leading Economic Indicators Index

●Wednesday: FOMC minutes

●Thursday: Chicago Fed National Activity Index, S&P Global Manufacturing and Services PMIs (flash), Existing Home Sales

This week’s earnings include:

●Tuesday: Axsome Therapeutics (AXSM), Home Depot (HD), KBR (KBR), LGI Homes (LGIH), Medtronic (MDT), Walmart (WMT), Keysight (KEYS), Palo Alto Networks (PANW), SolarEdge (SEDG), Toll Brothers (TOL)

●Wednesday: Analog Devices (ADI), Verisk Analytics (VRSK), DigitalOcean (DOCN), Etsy (ETSY), Five9 (FIVN), Nvidia (NVDA), Sunrun (RUN)

●Thursday: Fiverr (FVRR), Keurig Dr. Pepper (KDP), Newmont (NEM), Carvana (CVNA), Intuit (INTU), Block (SQ), Vir Biotechnology (VIR)

●Friday: Bloomin' Brands (BLMN), RB Global (RBA)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

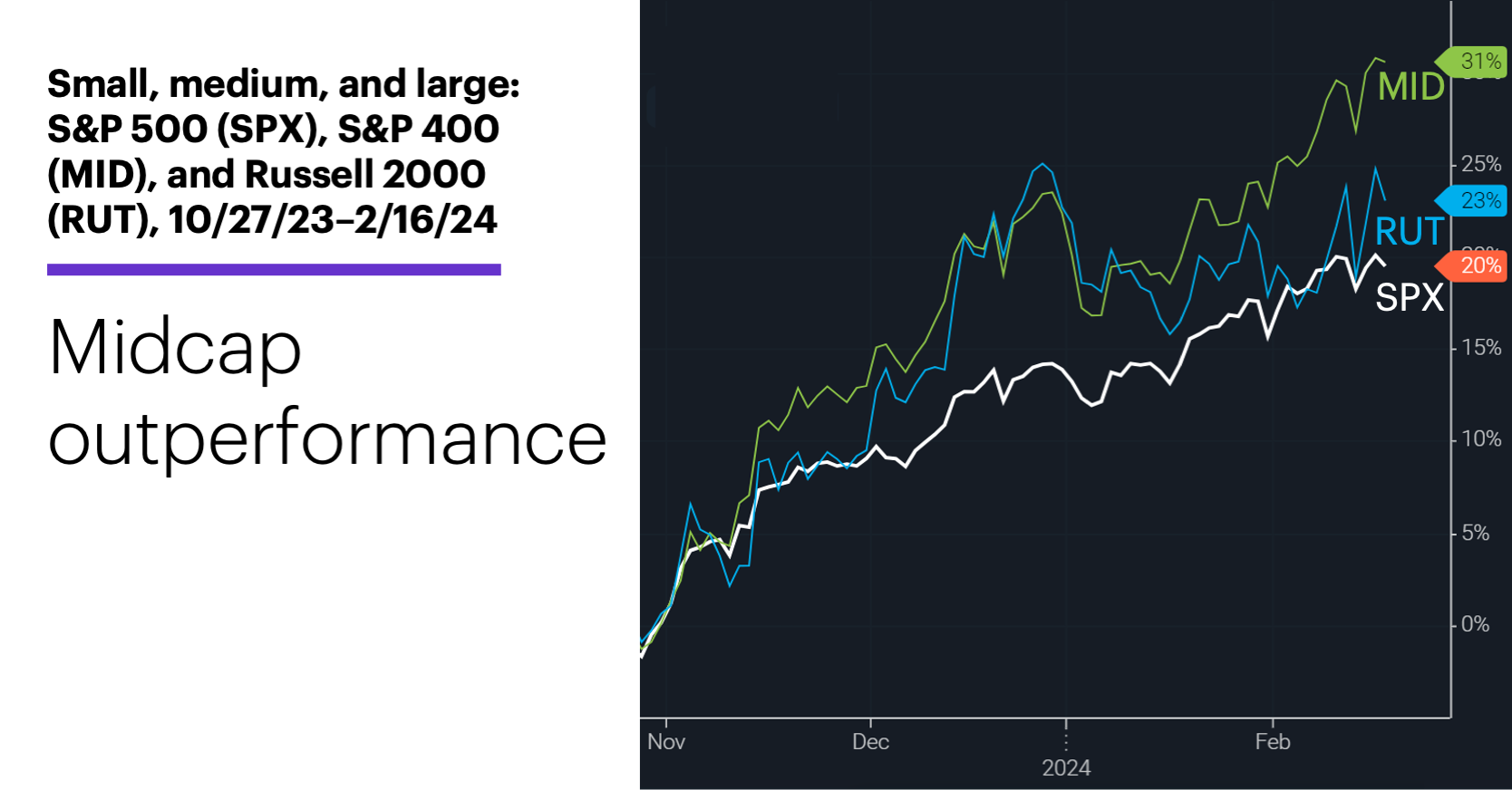

Forgotten midcaps

While last week’s inflation readings may have raised concerns the Fed will delay cutting interest rates, it’s too early to know whether those numbers were simply a blip in the overall disinflation trend, or something more significant.

For now, though, few analysts appear to doubt cuts are coming in the second half of the year—perhaps not as quickly as many people would like, but visible on the horizon, nonetheless. And that, as Morgan Stanley & Co. analysts explain, could lead to renewed strength in an area of the market that often gets lost in the shuffle—midcap stocks.

There’s already been some evidence of a shift. Since late-October lows, for example, the S&P 400 Midcap (MID) and the small-cap Russell 2000 (RUT) have mostly outgained the SPX:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

What could extend midcap relative strength? As the strategists note in “Quant Matters—Capturing Mid Cap Opportunities With Caution,” while midcap stocks are more vulnerable than large caps to high interest rates, they also have the potential to outperform as inflation stabilizes and in the early phase of a rate-cutting cycle.1

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Quant Matters—Capturing Mid Cap Opportunities With Caution. 2/12/24.