Stocks kick off June with record highs

- Indexes set fresh milestones, jobs surprise to upside

- More NVDA gains help propel tech sector

- This week: Inflation (CPI and PPI), Fed rate decision

Continued tech strength helped June get off to a bullish start, despite some end-of-week choppiness as an unexpectedly strong jobs report appeared to—again—raise concerns about how soon the Fed would cut interest rates.

Just three trading days after it tagged a three-week low on May 31, the S&P 500 (SPX) closed at a new all-time high last Wednesday. It followed through with two intraday records, despite a little weakness on Friday after the monthly employment report showed a big increase in the number of new jobs:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: New highs for stock indexes amid mixed jobs numbers

The fine print: Friday’s jobs surprise wasn’t just about the US economy adding 272,000 jobs in May—a big overshoot of the 190,000 estimate. Data earlier in the week, including job listings, private payrolls, and weekly jobless claims all suggested the labor market was slowing. But below Friday’s strong headline number, the picture was more balanced: Unemployment ticked up to 4%, while April payrolls were revised downward to 165,000.

The move: Despite closing lower Thursday and Friday, Nvidia (NVDA) rallied $112.55 (10.3%) last week and hit higher highs every day but one—one of the pillars of the tech sector’s market-leading gain.

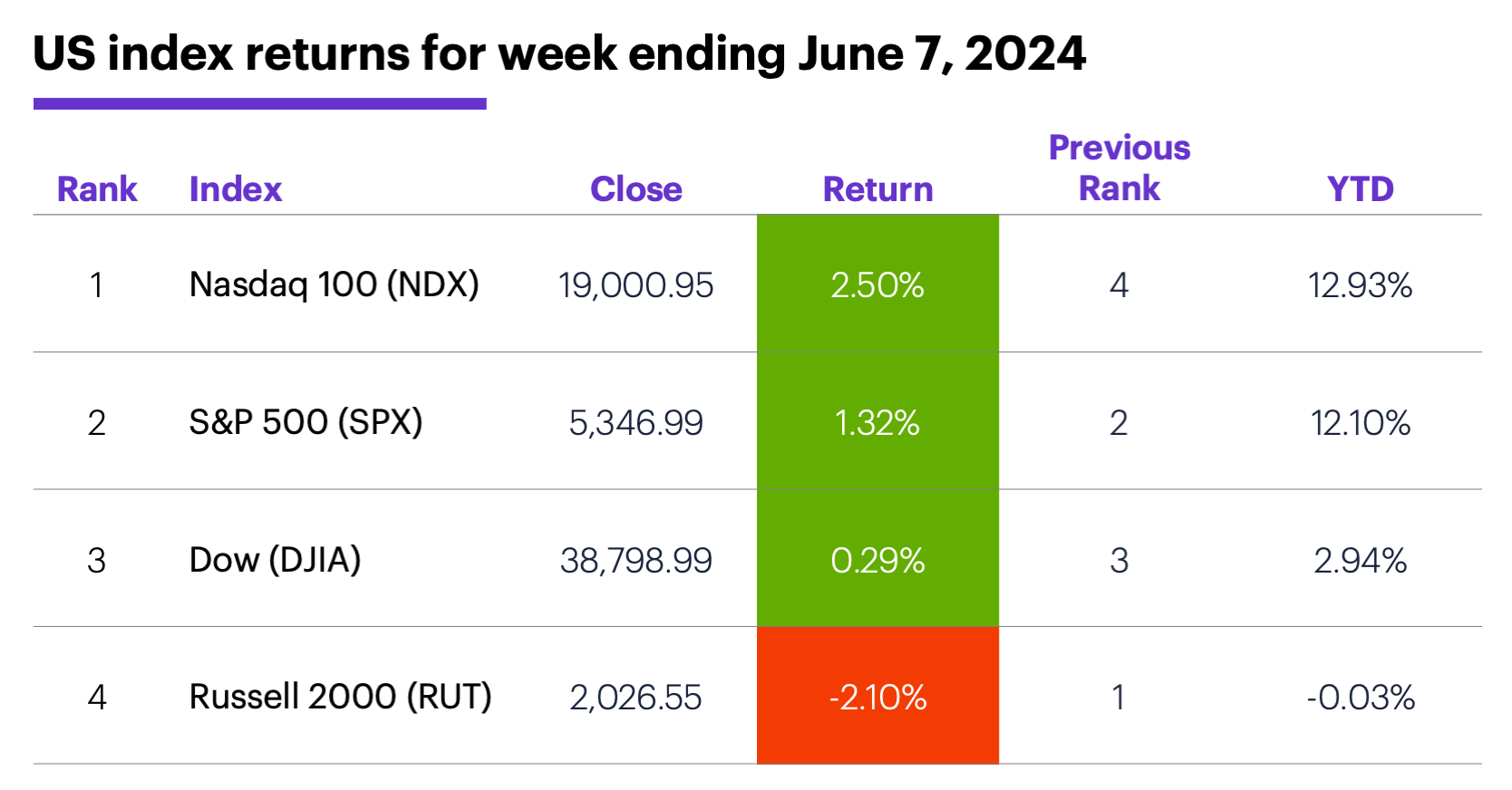

The scorecard: Along with the SPX, the Nasdaq 100 (NDX) tech index (and the Nasdaq Composite) hit multiple record highs last week. The Russell 2000 (RUT) small cap index failed to participate in the week’s gains, and ended the week slightly in the red for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+3.9%), communication services (+2%), and health care (+2%). The weakest sectors were utilities (-3.7%), energy (-3.3%), and materials -1.9%).

Stock movers: Structure Therapeutics (GPCR) +54% to $52.74 on Monday, GameStop (GME) +47% to $46.55 on Thursday (then -39% to $28.22 on Friday). On the downside, Ambac Financial Group (AMBC) -20% to $13.81 on Wednesday, Arcturus Therapeutics (ARCT) -25% to $31.82 on Friday.

Futures: After falling to a four-month low ($72.48) last Tuesday in the wake of OPEC’s announced production increases, July WTI crude oil (CLN4) rebounded to end the week down less than $2 at $75.53. A sharp (-3.4%) Friday sell-off dropped August gold (GCQ4) to $2,325, its lowest close since April. Week’s biggest gains: July natural gas (NGN4) +13.6%, July cocoa (CCN4) +6.5%. Week’s biggest declines: July oats (ZON4) -10.2%, June Mexican peso (6MM4) -7.7%.

Coming this week

Circle Wednesday—CPI in the morning, and the Fed’s interest rate announcement in the afternoon:

●Tuesday: NFIB Small Business Optimism Index

●Wednesday: Consumer Price Index (CPI), Fed Interest Rate Decision

●Thursday: Producer Price Index (PPI)

●Friday: Import and Export Prices, Michigan Consumer Sentiment (preliminary)

This week’s earnings include:

●Monday: Calavo Growers (CVGW)

●Tuesday: Oracle (ORCL), Academy Sports & Outdoors (ASO), Casey’s General Stores (CASY), Rubrik (RBRK)

●Wednesday: Broadcom (AVGO), Dave & Buster’s (PLAY)

●Thursday: Jabil (JBL), Signet Jewelers (SIG), Adobe (ADBE), RH (RH)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Utilities more than defensive?

Over the past three months, the SPX has gained 3.8% (despite tagging several record highs), while the S&P 500 utilities index has rallied 10.3%—more than any other sector except communications services. The majority of that relative strength has occurred since mid-April, when the market began rebounding off its pullback lows.

While it would be easy to argue this relative strength in utilities was the result of cautious investors shifting into a traditionally defensive sector amid various uncertainties—inflation, geopolitical risk, looming elections—Morgan Stanley & Co. research points to another possible factor.

In mapping the impact of AI on different areas of the global stock market, the analysts found the utilities sector was second only to tech in terms of its increased AI exposure since Q4 2023, and 97% of the global utilities stocks the analysts cover increased their AI “materiality”—conditions with the potential to support further upside in the sector.1

Event update: A Morgan Stanley Market Update will be available “On Demand” for all E*TRADE clients at 4:30 p.m. ET today. Morgan Stanley Wealth Management's Head of Market Research and Strategy, Dan Skelly, will discuss what may be in store for investors in the back half of 2024. To watch, click this link to log into your account. You will automatically be taken to the landing page.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. MorganStanley.com. Mapping AI’s Rate of Change. 6/4/24.