Tech carries market

- Stocks mixed—tech rolls, real estate and energy tumble

- Bond yields climb, oil pulls back, metals retreat from highs

- This week: Fed inflation, GDP, more retail earnings

The US stock market is coming off a second week of record highs, but not necessarily another week of gains as the major indexes churned amid hawkish Fed minutes and mixed economic data and earnings.

Tech fared well, but gains elsewhere were more elusive and trading was choppy. The S&P 500 (SPX) pushed to an all-time intraday high on Thursday but sold off sharply to close at a five-day low, and Friday’s rebound was just enough to get the index back to breakeven for the week:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Market wobbles around highs.

The fine print: Last Thursday’s intraday reversal occurred despite AI chipmaker Nvidia’s (NVDA) breakout to record highs after its latest earnings beat. The stock closed up more than 9%, but even the Nasdaq 100 (NDX) tech index ended the day in the red.

The numbers: As recently noted by Morgan Stanley Wealth Management, recent economic data has been “noisy.”1 Last week’s numbers were no exception. Home sales slowed, but durable goods orders were much stronger than expected, +0.7% vs. the -0.5% estimate.

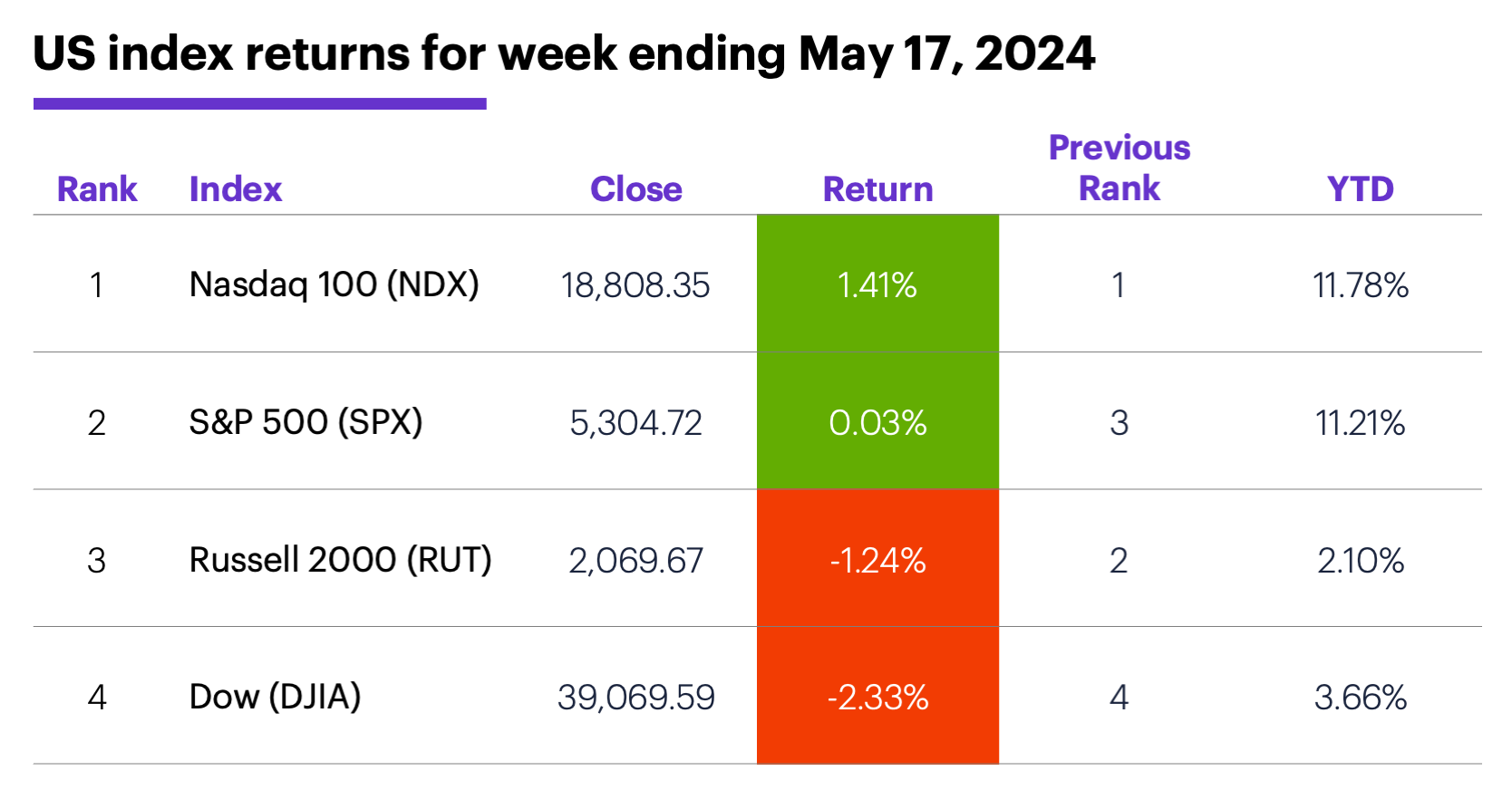

The scorecard: The NDX rode tech strength to a positive week and a record high and close on Friday:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+3.3%), communication services (+0.1%), and industrials (-0.8%). The weakest sectors were energy (-3.9%), real estate (-3.7%), and financials (-2.1%).

Stock movers: Bakkt Holdings (BKKT) +45% to $16.65 on Monday, Merus (MRUS) +36% to $59.99 on Friday. On the downside, Verastem (VSTM) -66% to $4.12 and Workday (WDAY) -15% to $220.91, both on Friday.

Futures: Despite a Friday rally, July WTI crude oil (CLN4) closed Friday at $77.72, down $1.86 for the week. Gold (and other metals) retreated, with June gold (GCM4) closing at a record high of $2,430.30 last Monday, then ending the week more than $80 lower at $2,334.50. Week’s biggest gainers: May ether (ETHK4) +20.6%, July cocoa (CCN4) +12.9%. Week’s biggest decliners: June milk (DCM4) -7.4%, June cheese (CSCM4) -6.5%, July copper (HGN4) -5.7%.

Coming this week

It may be a short week, but it’s a busy one, with Fed inflation (PCE Price Index), the first revision of Q1 GDP, and housing prices:

●Tuesday: S&P Case-Shiller Home Price Index, FHFA House Price Index, Consumer Confidence, Dallas Fed Manufacturing Index

●Wednesday: Fed Beige Book

●Thursday: GDP (second estimate), Trade Balance in Goods (advance), retail and wholesale inventories (advance), Pending Home Sales

●Friday: Personal Income and Spending, PCE Price Index, Chicago PMI

Retail highlights the earnings calendar again, but there are also a few notable tech names:

●Tuesday: Box (BOX), Heico (HEI), Cava Group (CAVA)

●Wednesday: Advance Auto Parts (AAP), Abercrombie & Fitch (ANF), Dick’s Sporting Goods (DKS), Agilent Technologies (A), American Eagle Outfitters (AEO), C3 AI (AI), Salesforce (CRM), HP (HPQ), Okta (OKTA)

●Thursday: Best Buy (BBY), Burlington Stores (BURL), Dollar General (DG), Foot Locker (FL), Kohl's (KSS), Autodesk (ADSK), Ambarella (AMBA), Costco (COST), Dell (DELL), Gap (GPS), Nordstrom (JWN), Lululemon Athletica (LULU), Marvell Technology (MRVL), Ulta Beauty (ULTA), Zscaler (ZS)

●Friday: Genesco (GCO)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

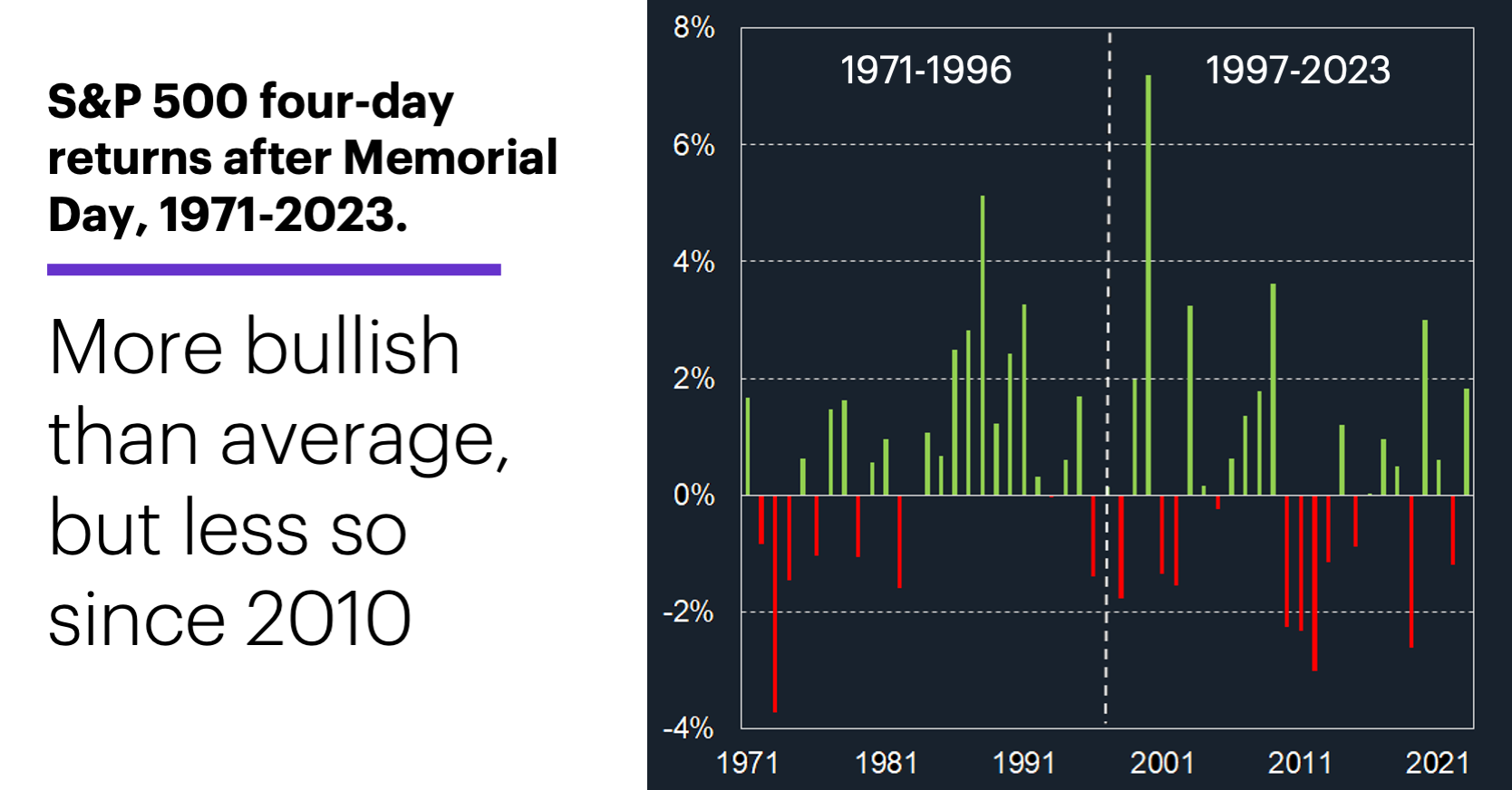

Memorial Day market pattern

Since 1971, when Memorial Day became a fixed Federal holiday on the last Monday in May, the shortened week after it has tended to be more bullish for the market than the average four-day period.

While the SPX had a positive return in 56% of all four-day periods from May 1971–May 2023 (with an average return of 0.14%), it had a positive return in 62% of the four-day periods following Memorial Day, with an average gain of 0.5%:2

Data source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

However, over the most recent 27 years (and especially since 2010) declines have been more common and, sometimes, larger. From 1971-1996 the SPX gained ground in the four days after Memorial Day in 17 of 26 years, with an average return of 0.7%. But from 1997-2022, the SPX rallied during this period in just 16 of 27 years, with average return of 0.4%.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. The GIC Weekly: For Now, Bad Is Good. 5/20/24.

2 All figures reflect S&P 500 (SPX) daily prices, May 1971–May 2023. Supporting document available upon request.