Market pauses amid milestones

- Stocks cool on Friday after grab-bag jobs data

- Powell takes middle road, record week for gold

- This week: inflation (CPI and PPI), retail sales

Jerome Powell’s congressional testimony didn’t surprise anyone, the jobs report did, and the US stock market pushed its four-month-plus rally to new highs last week, even though it ran out of gas on Friday and lost ground for the week.

After a tech-led sell-off last Tuesday, the market rebounded the next two days as the Fed Chair continued to preach patience, but didn’t back away from the idea that the central bank would likely cut rates later this year. The S&P 500 (SPX) rallied to a second-straight all-time high early Friday after a mixed jobs report, but the bullish momentum evaporated as the session progressed:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks wobble at highs as traders parse jobs data.

The fine print: Friday’s jobs report initially looked hot—275,000 new jobs in February vs. an estimated 198,000—but with January’s and December’s totals both revised lower, first impressions may have been misleading. Following two days of somewhat soft secondary employment numbers, the week’s overall picture was of a still-solid labor market that may be cooling slightly. Depending on how one looked at it, the report had something for everyone—or no one, which may have explained some of Friday's volatility.

The number: $500 billion, the estimated opportunity Morgan Stanley & Co. analysts associate with an expected fivefold increase in the European data center market,1 driven by the need to keep up with key tech trends, like Generative AI.2

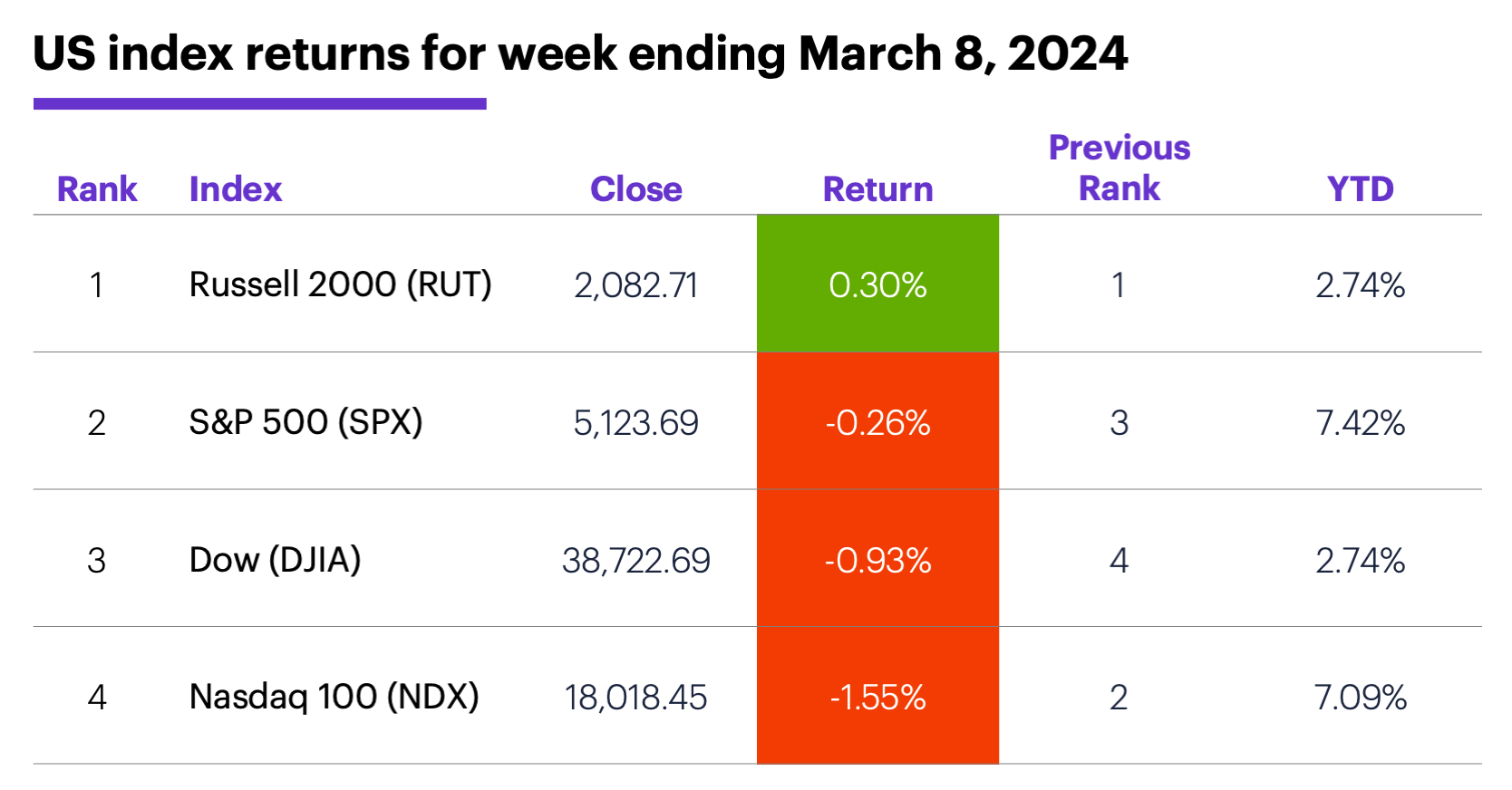

The scorecard: The small-cap Russell 2000 (RUT) held up best last week, while the Dow Jones Industrial Average (DJIA) lost the most ground:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were utilities (+3.4%), materials (+1.7%), and real estate (+1.6%). The weakest sectors were consumer discretionary (-2.6%), tech (-0.8%), and communication services (-0.6%).

Stock movers: On Wednesday, American Public Education (APEI) +37% to $15.57, and Hippo (HIPO) +34% to $19.39. On the downside, Phunware (PHUN) -30% to $10.27 on Wednesday, Amylyx Pharmaceuticals (AMLX), -82% to $3.36 on Friday.

Futures: Gold broke out of a trading range in record fashion, notching its eighth-straight up day and fifth-consecutive all-time high on Friday. April gold (GCJ4) topped $2,200 intraday on Friday, and ended the week up more than $85 at $2,184.50. April WTI crude oil (CLJ4) still hasn’t managed to break out of its consolidation, selling off on Friday to end the week nearly $2 lower at $77.86.

Coming this week

It’s all about inflation this week, as traders get a look at the latest Consumer Price Index and Producer Price Index readings:

●Monday: New York Fed Consumer Inflation Expectations

●Tuesday: NFIB Business Optimism Index, Consumer Price Index (CPI)

●Thursday: Producer Price Index (PPI), Retail Sales, Business Inventories

●Friday: Import and Export Prices, Empire State Manufacturing Index, Industrial Production and Capacity Utilization, Consumer Sentiment (prelim)

This week’s earnings includes another healthy dose of retail names:

●Monday: Casey's General Stores (CASY), Vail Resorts (MTN)

●Tuesday: Kohl's (KSS), Guess (GES), Phunware (PHUN)

●Wednesday: Dollar Tree (DLTR), Five Below (FIVE), Lennar (LEN), UiPath (PATH), Vroom (VRM)

●Thursday: Canadian Solar (CSIQ), Dollar General (DG), Dick’s Sporting Goods (DKS), GIII Apparel (GIII), Adobe (ADBE), Ulta Beauty (ULTA)

●Friday: Buckle (BKE), Jabil (JBL)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

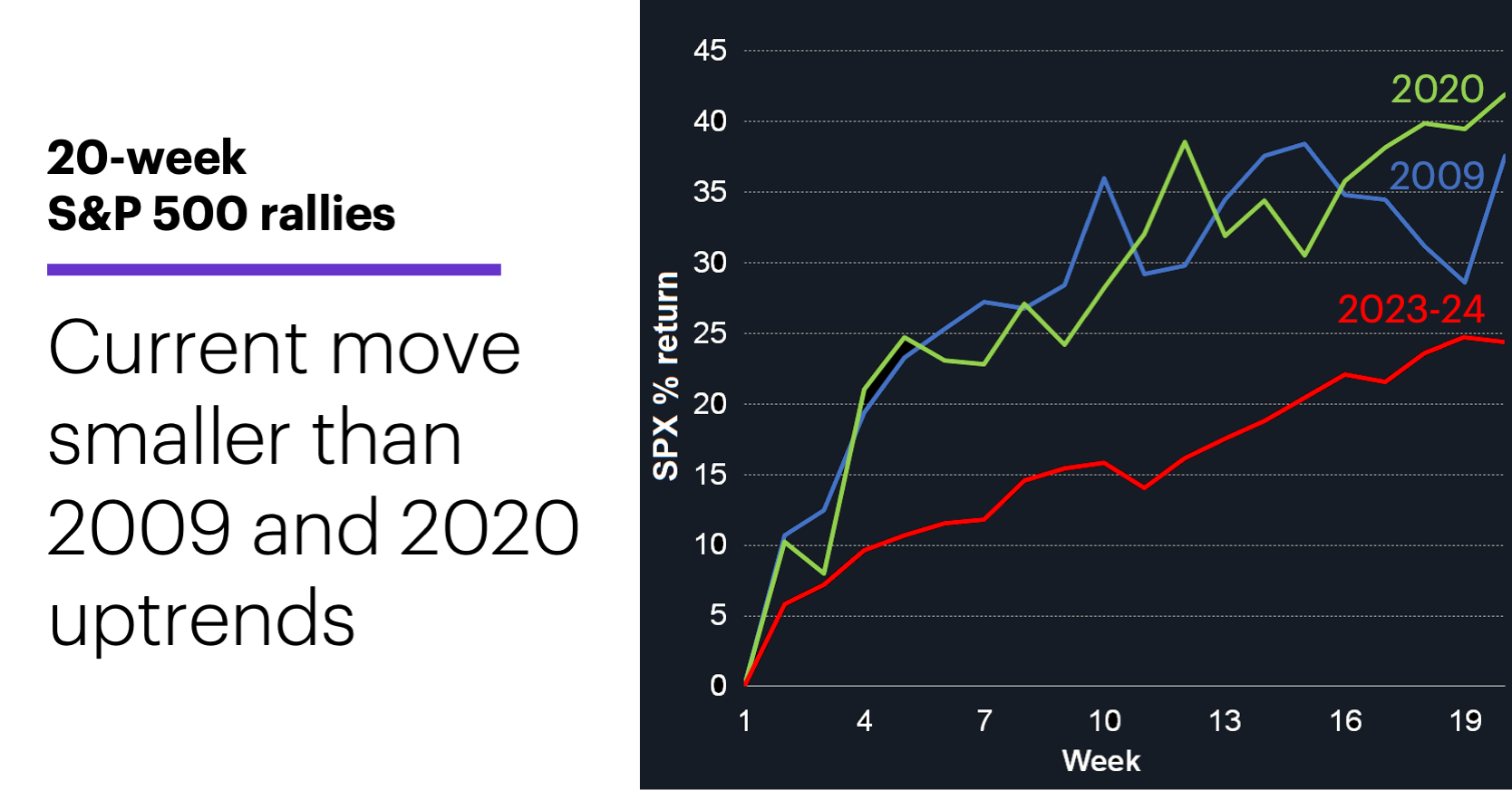

Rally check

The market may have paused last week, but the rally off the October lows, which reached the 20-week mark on Friday, is certainly one of the most notable of the past couple of decades.

Although some market watchers appear to be running out of superlatives regarding its recent performance, the following chart shows the uptrend isn’t without precedent:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index. Performance reflects percentage change in weekly closing prices, indexed to 100.)

Although the SPX ended last week roughly 25% above its October 2023 lows (red line), the rallies off the March 2020 pandemic lows (green) and the March 2009 financial crisis lows (blue) were both larger after 20 weeks.3

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Three Long-Term Trends by the Numbers. 3/6/24.

2 MorganStanley.com. Why European Data Centers Are Set for Major Growth. 3/7/24.

3 All figures reflect weekly closing prices, 2009–2024. Supporting document available upon request.