Record run gets inflation test

- Market cautious amid sticky inflation data

- Small caps fall, energy rides oil surge, bond yields jump

- This week: FOMC meeting, housing data

The stage is set for this week’s Fed policy meeting, after last week’s double-dose of higher-than-expected inflation data renewed debate over whether the central bank is still on track to cut interest rates early in the second half of the year.

The S&P 500 (SPX) shrugged off last Tuesday’s upside surprise from the consumer price index (CPI)—rallying more than 1% and closing at a record high—but it appeared to have second thoughts after Thursday’s producer price index (PPI) came in even hotter. The end result was a small weekly loss for the SPX—its first back-to-back down weeks since October:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Market pads records despite inflation data.

The fine print: Last week was the ninth in a row that the SPX made at least one new record high, even though it posted a net loss for the week. Continuing that streak may depend on whether traders and investors think the Fed will delay cutting interest rates until later in the second half of the year—a risk Morgan Stanley & Co. strategists debated in a recent economic roundtable.1 As of Friday, the odds of a June rate cut stood at 51%.2

The number: 20, the number of weeks since the last time the SPX posted back-to-back down weeks—one shy of its longest streak of the past decade (December 2018–May 2019).

The move: May cocoa futures (CCK4) jumped more than 25% last week to a new all-time high of $8,018/ton. Cocoa prices are up more than 190% year over year.

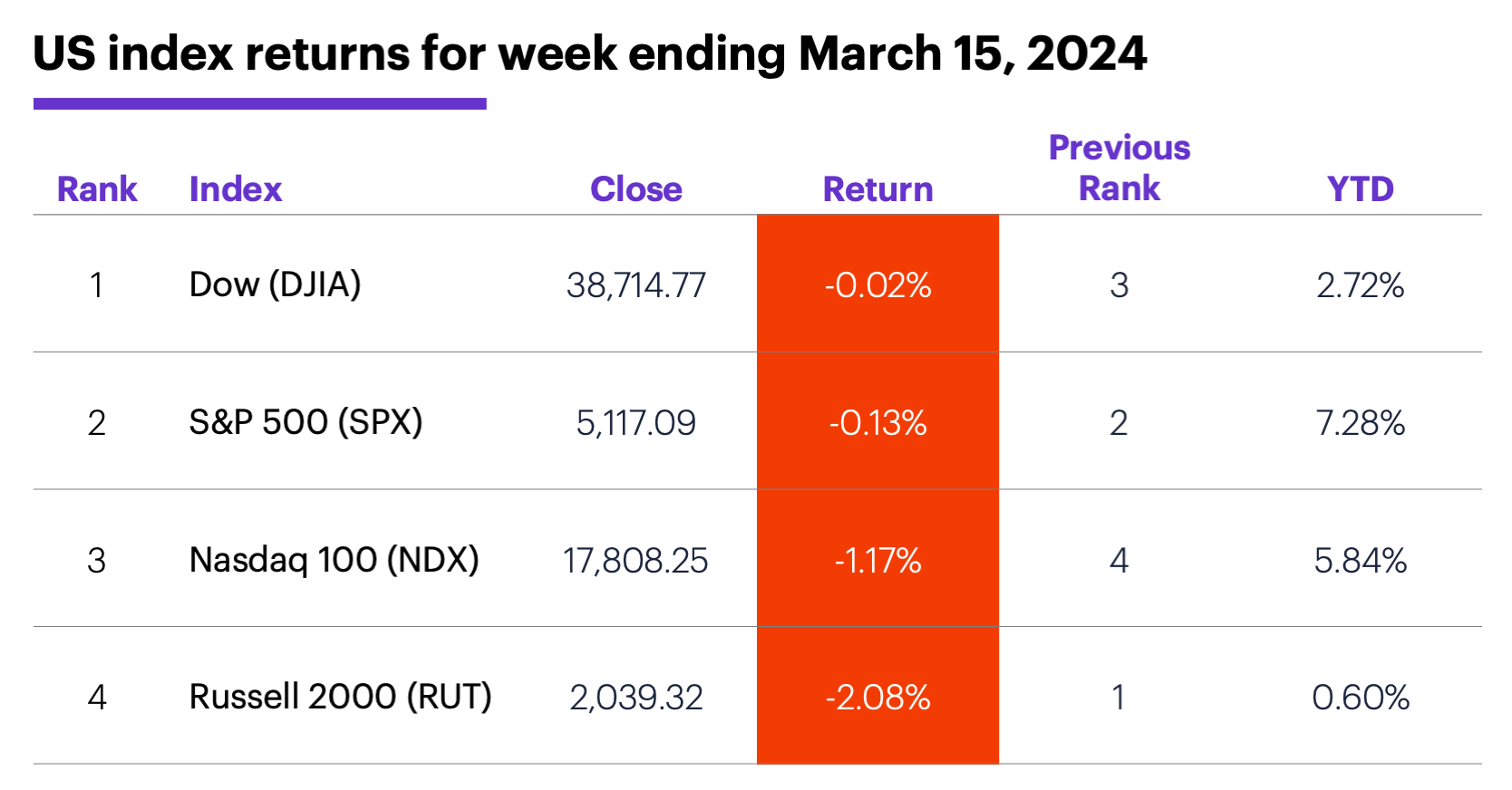

The scorecard: The small-cap Russell 2000 (RUT) and Nasdaq 100 (NDX) tech index posted the biggest declines last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+3.7%), materials (+1.5%), and communication services (+0.4%). The weakest sectors were real estate (-3.1%), consumer discretionary (-1.2%), and health care (-0.9%).

Stock movers: Vroom (VRM) +56% to $17.49 on Wednesday, Cardlytics (CDLX) +77% to $14.50 on Friday. On the downside, Pagaya Technologies (PGY) -25% to $11.55 and RCM Technologies (RCMT) -25% to $21.60, both on Thursday.

Futures: April WTI crude oil (CLJ4) hit its highest level since late October ($81.62) last week amid Ukrainian drone strikes on Russian oil refineries and a tight 2024 supply forecast.3 The market ended the week up more than $3 at $81.04. April gold (GCJ4) retreated from record highs, closing Friday at $2,161.50. Week’s biggest rallies: May cocoa (CCK4) +25.4%, May RBOB gasoline (RBK4) +7.4. Week’s biggest declines: March ether (ETHH4) -7.1%, May natural gas (NGK4) -7%.

Coming this week

No one’s looking for the Fed to cut rates on Wednesday, but everyone’s looking for clues about what they thought of last week’s sticky inflation data, and if it will impact their timeline:

●Monday: NAHB Housing Market Index

●Tuesday: Housing Starts and Building Permits

●Wednesday: Fed interest rate decision

●Thursday: Current Account Q4, Philadelphia Fed manufacturing survey, S&P Global Manufacturing PMI (flash), S&P Global Services PMI (flash), Existing Home Sales, Leading Economic Indicators Index

This week’s earnings include:

●Monday: Science Applications (SAIC), StoneCo (STNE)

●Tuesday: Core & Main (CNM), HealthEquity (HQY)

●Wednesday: General Mills (GIS), Ollie’s Bargain Outlet (OLLI), Chewy (CHWY), Five Below (FIVE), KB Home (KBH), Micron Technology (MU)

●Thursday: Accenture (ACN), Designer Brands (DBI), Darden Restaurants (DRI), FedEx (FDX), Lululemon (LULU), Nike (NKE)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Pedal to the metal

Gold may have given back some ground last week, but it’s still well above its late-February highs and still basking in the afterglow of its push to record highs a week earlier. But as has been the case many times in the past, gold grabbed headlines even though it lagged the rest of the precious metals space.

Since February 27—the day before gold strung together nine-straight up days and multiple record highs—April gold futures (GCJ4) had gained 6% as of Friday. Not only was that roughly half as much as the returns in silver and palladium over the same period, it was slightly less than platinum’s 7% gain, and even trailed copper’s 8% rally.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Economics Roundtable: Updating Our 2024 Outlook. 3/14/24.

2 CMEGroup.com. CME FedWatch Tool—Meeting Probabilities. 3/15/23.

3 U.S. Energy Information Administration (www.eia.gov). Short-term energy outlook. 3/12/24.