Stocks start March at record highs

- Stocks climb amid moderate Fed inflation reading

- First Nasdaq Comp record high since 2021

- This week: jobs report, Jerome Powell congressional testimony

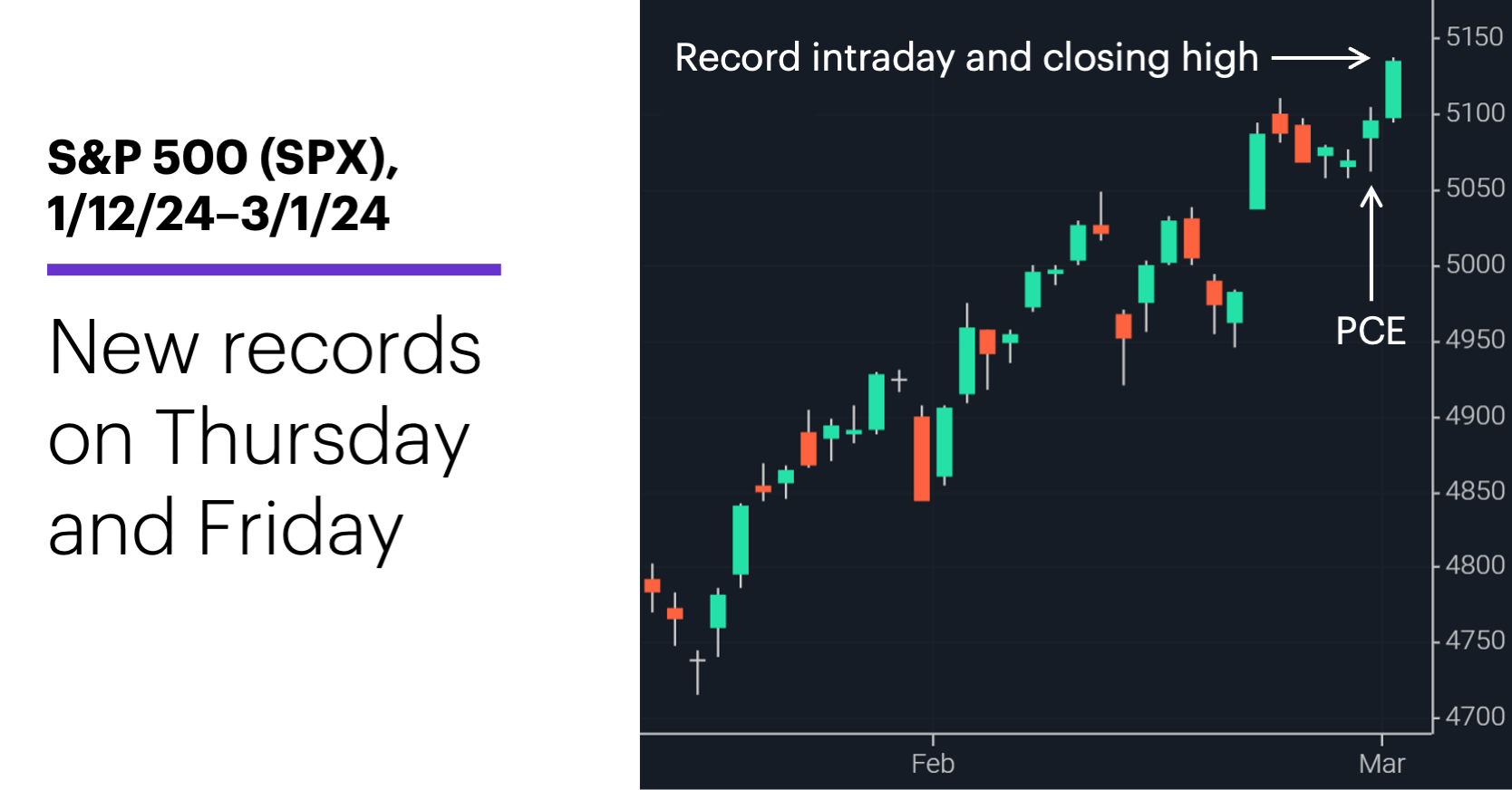

After stumbling mid-February on hotter-than-expected inflation data, stocks ended the month with a bounce as a cooler reading from the Fed’s go-to inflation gauge, the PCE Price Index, appeared to ease concerns the central bank would further delay rate cuts.

In addition to boosting the S&P 500 (SPX) to its second-biggest February return of the past 25 years (5.2%), Thursday’s rally helped the index claim its 16th positive week out of the past 18, and end last week with consecutive record highs:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Bears still hibernating as March starts.

The fine print: The market had been pulling back last week before last Thursday’s PCE release, which actually showed inflation rose in January. But the fact that the increase was in line with expectations—and that December’s number was revised lower—may have encouraged bulls after the upside surprises from the CPI and PPI earlier in February. Morgan Stanley & Co. analysts recently discussed some of the peculiarities of the recent inflation data, and how the Fed may interpret it.1

The number: 53.7%, the probability of a June rate cut as of Friday.2 The odds were below 50% before the PCE Price Index release.

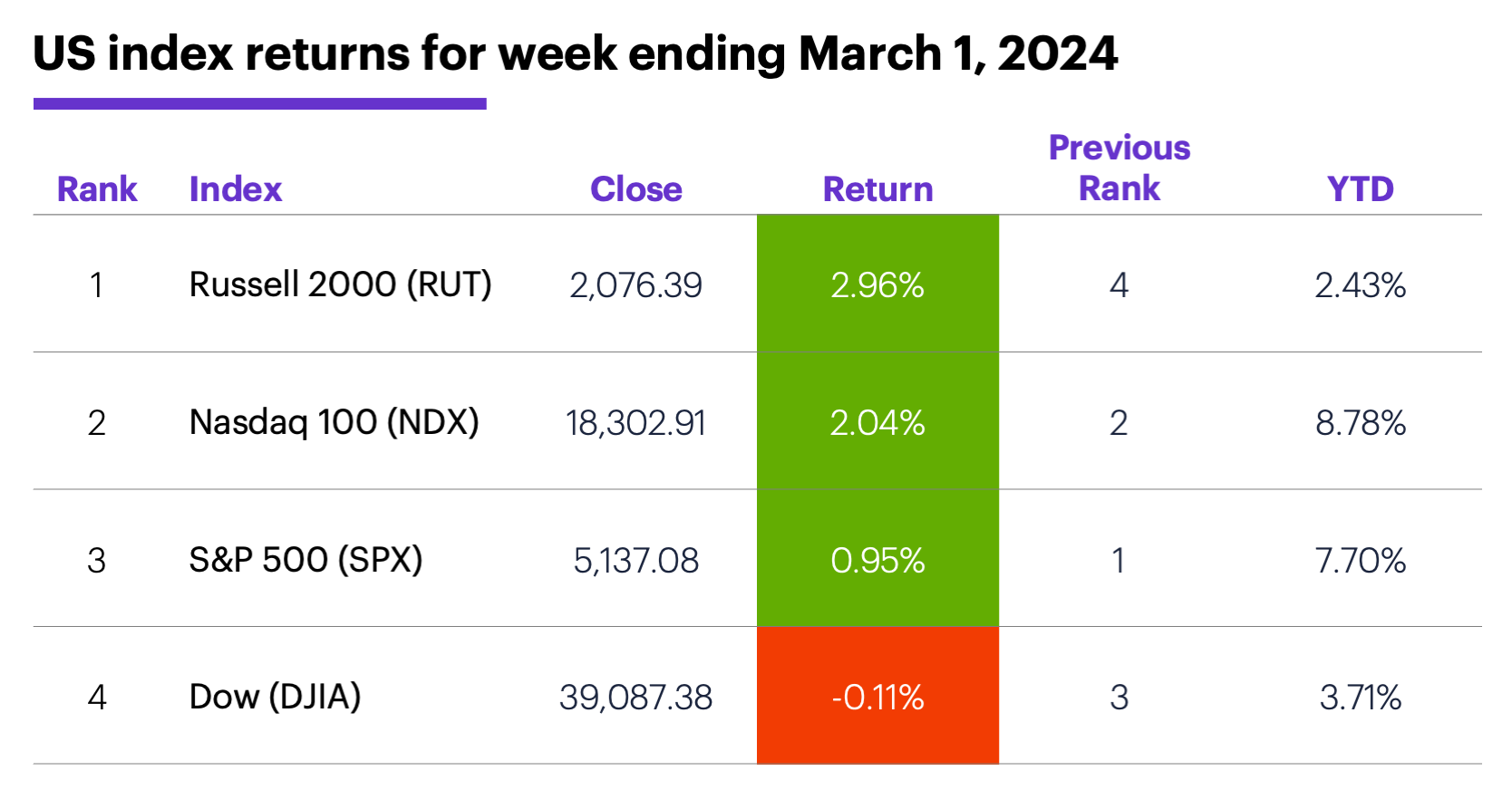

The scorecard: The Nasdaq 100 (NDX) led the market last week, and joined the SPX in hitting new record highs:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+2.5%), consumer discretionary (+2.2%), and real estate (+1.9%). The weakest sectors were health care (-1.%), utilities (-0.7%), and consumer staples (-0.5%).

Stock movers: On Tuesday, Janux Therapeutics (JANX) +230% to $49.75 and Viking Therapeutics (VKTX) +121% to $85.05. On Thursday, Ironwood Pharmaceuticals (IRWD) -38% to $9.43 and Xometry (XMTR) -35% to $19.56.

Futures: After falling to a six-day intraday low of $75.84 last Monday, WTI crude oil (CLJ4) ended last week near a four-month high of $79.97. After its biggest up day of the year on Friday, April gold (GCJ4) closed the week at a one-month high of $2,095.70. Week’s biggest rallies: March Micro bitcoin (MBTH4) +22.5%, March Micro ether (METH4) +16%. Week’s biggest declines: March Dry Whey (DYH4) -10.1%, April milk (DCJ4) -5.7%.

Coming this week

Friday’s jobs report is this week’s headliner, but two days of Fed Chair Jerome Powell congressional testimony may give it a run for its money:

●Tuesday: S&P Global Services PMI, ISM Services Index, Factory Orders

●Wednesday: ADP Employment, Job Openings and Labor Turnover Survey (JOLTS), Wholesale Inventories, Fed Beige Book, Jerome Powell congressional testimony

●Thursday: Challenger Job Cuts, Trade Balance, Productivity and Labor Costs, Consumer Credit, Jerome Powell congressional testimony

●Friday: Employment Report, Consumer Sentiment

This week’s earnings include:

●Monday: AeroVironment (AVAV), Gitlab (GTLB), Inhibrx (INBX)

●Tuesday: Box (BOX), CrowdStrike (CRWD), Nordstrom (JWN), Ross Stores (ROST)

●Wednesday: Abercrombie & Fitch (ANF), Campbell Soup (CPB), Foot Locker (FL), REV Group (REVG), Thor Industries (THO), United Natural Foods (UNFI)

●Thursday: American Eagle Outfitters (AEO), BJ's Wholesale Club (BJ), Burlington Stores (BURL), Kroger (KR), Broadcom (AVGO), DocuSign (DOCU), Mongodb (MDB)

●Friday: Buckle (BKE), Janux Therapeutics (JANX)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

That ‘70s Market

To many observers, last week may have seemed like “more of the same,” in that it marked the seventh-straight week the SPX hit at least one new record high.

But the SPX also marked a more obscure momentum milestone: It closed higher for the 16th week of the past 18, while hitting its highest level in at least 26 weeks.

The last time it did that, Richard Nixon was president, Patton was about to win the Oscar for Best Picture, and the SPX was trading a little above 100—in April 1971.

While that mostly highlights how strong the recent rally has been, it may be worth noting what happened after the other times the SPX accomplished the same feat. Eight weeks later the index had gained an additional 1.7%, on average, which is a little more than its 1.3% average return for all eight-week periods since 1957.3 Twelve weeks after the SPX hit these highs, though, the average return had contracted to 1.4%, which is also less than its 1.9% average return for all 12-week periods.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 CMEGroup.com. FedWatch Tool. 3/1/24.

2 MorganStanley.com. Making Sense of Confusing Economic Data. 2/28/24.

3 All figures reflect weekly closing prices, 1957–2024. There were 17 instances of the weekly pattern from 1957-1971. Supporting document available upon request.