Fed stays on hold

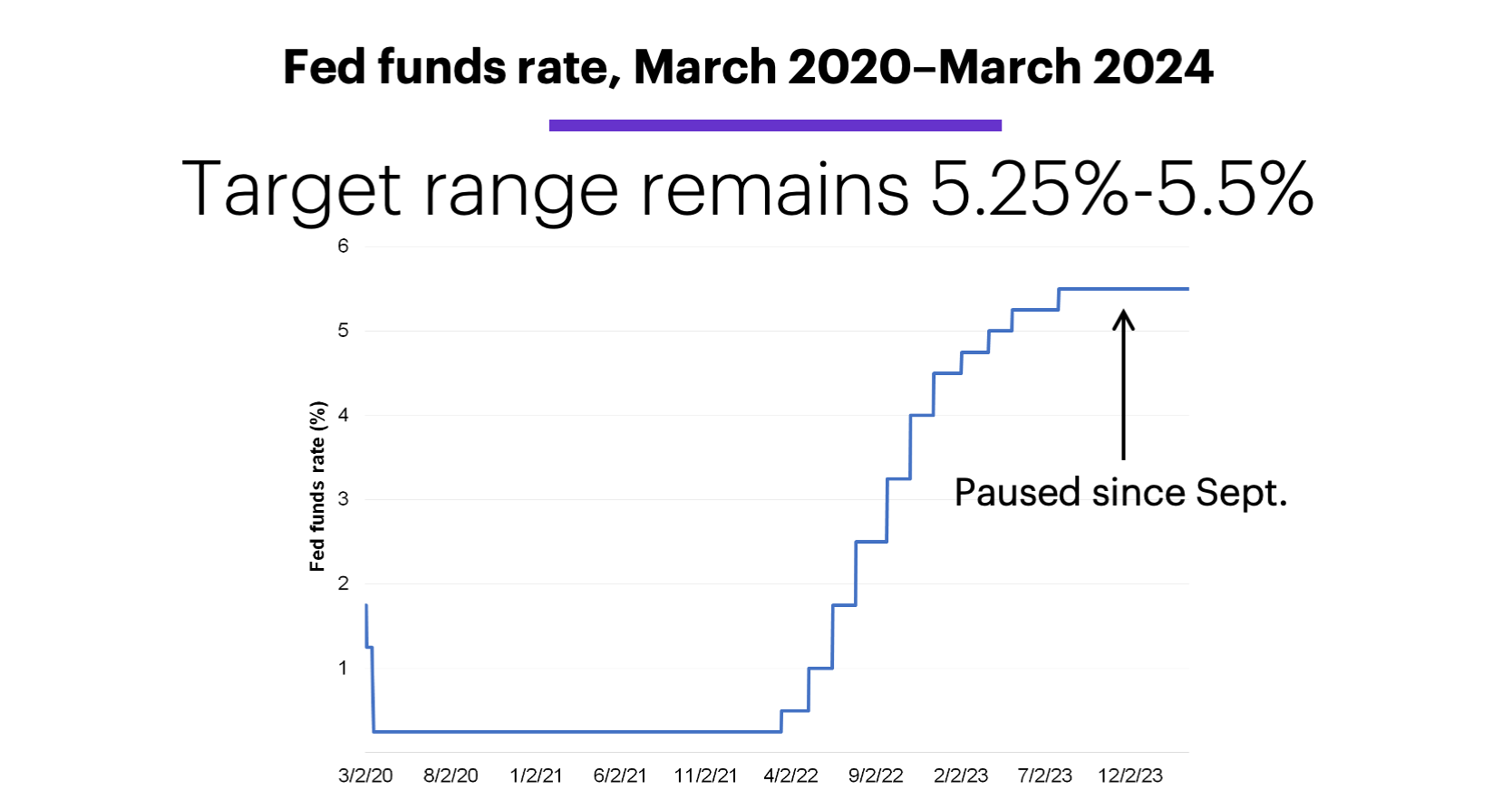

After its second policy meeting of 2024, the Federal Reserve surprised no one by leaving its benchmark fed funds rate unchanged on Wednesday. The current target range of 5.25%-5.5% has been in effect since September:

Source (data): Federal Reserve. Values represent upper end of Fed funds target range. (For illustrative purposes. Not a recommendation.)

When the Fed raises rates, auto loans, credit card rates, and mortgages become more expensive, while companies pay more to borrow money. That can make both consumers and businesses more conservative about spending—which may then cool the economy and, hopefully, drive down the prices of goods and services. The Fed’s challenge has been to accomplish this goal without tipping the economy into recession. So far, they’ve succeeded.

Now they face a different challenge—lowering rates without reigniting inflation. While it has cooled significantly since its mid-2022 high, inflation is still above the Fed’s 2% target level and the economy has, overall, remained robust.

Morgan Stanley & Co. analysts think inflation readings could remain 'bumpy,' but will continue to trend lower overall.

Last week, though, the Consumer Price Index (CPI) and Producer Price Index (PPI) both came in above estimates for a second-straight month, renewing concerns about inflation “stickiness” and whether it may cause the Fed to keep rates higher for longer. The Fed’s primary concern is that lowering rates too soon or by too much could overheat an already strong economy and send inflation higher again.

Morgan Stanley & Co. analysts believe the base case is for inflation readings to remain “bumpy,” but trend lower over the course of the year. If that’s accompanied by moderating job growth, they recently argued, it would keep the Fed on track to start cutting rates in June.1

Regardless of the uncertainty this may pose for the stock market, which has arguably already priced in multiple rate cuts for this year, higher interest rates have an upside: meaningful returns for fixed income investors. After falling sharply in November and December, bond yields rebounded, and are again relatively close to their highest levels of the past decade. Maintaining a balanced portfolio of quality stocks (those with proven cash flow, and/or a record of consistently raising dividends) and fixed income investments should remain an attractive strategy for long-term investors.

Note: The Fed’s next policy meeting is scheduled for April 30-May 1.

1 MorganStanley.com. Rate Cut Uncertainty. 3/15/24.