Looking past a “record” January

E*TRADE from Morgan Stanley

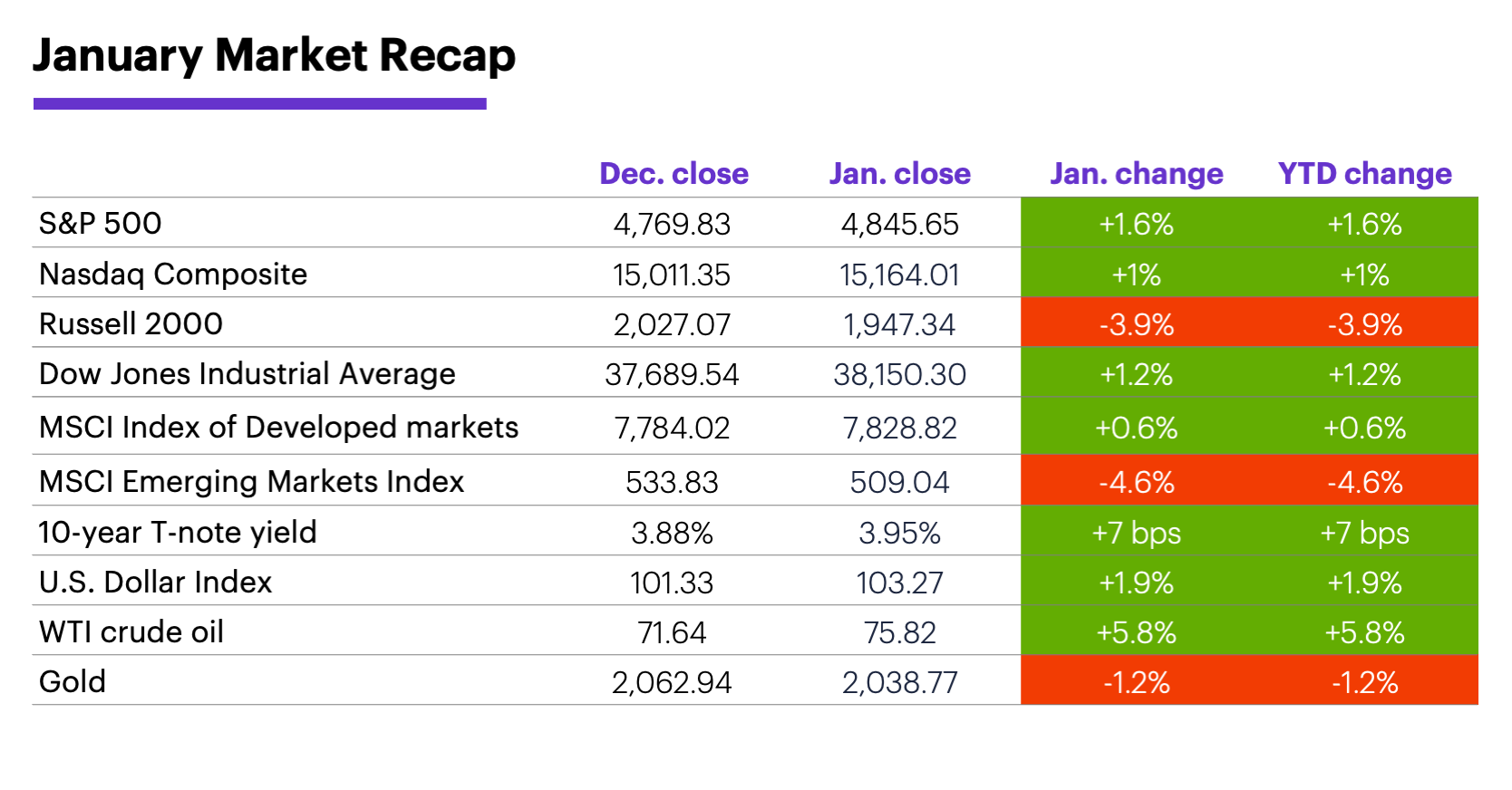

It may have had a rough start and bumpy finish, but January turned out to be what even some bulls may not have expected—an extension of the market’s record-setting rally off its late-October lows.

Instead of taking a breather after its second-strongest November-December rally of the past 60 years, the S&P 500 (SPX) pushed to new all-time highs last month, ending January up 15.5% since October 31—its biggest three-month gain since June 2020. But the month also ended on a cautious note as the Fed appeared to downplay the possibility of a March rate cut.

Small cap stocks were the notable exception. The Russell 2000 index (RUT), which rallied more than 12% in December, was the only major US index to decline in January.

Investors were mostly “risk on,” with communication services and tech posting the biggest gains of the month. Meanwhile, real estate, materials, and utilities lost ground—but so did consumer discretionary, which is typically a risk-on sector.

Bonds disengaged from stocks. Bond prices fell throughout most of January while stocks rallied, then rebounded at the end of the month as stocks pulled back. The benchmark 10-year T-note yield posted its first monthly increase (albeit, a small one) since October, despite a sharp downturn at the end of January.

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: Crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%.

The Fed left rates unchanged at 5.25%-5.5% on the last day of January, and continued to stress that it’s in no rush to lower them. The Fed’s path to interest rate cuts later this year—and the degree to which they may already be priced into the market—remains a focal point for the market. According to Morgan Stanley & Co. strategists, one thing that probably won’t influence the Fed is the presidential race.1

But the election is far from irrelevant for the markets. Morgan Stanley & Co. strategists believe this election will “clearly be consequential” for markets, but they argue it’s too early to know the outcome, or what policies may emerge from it. They also note that market and economic conditions closer to the election may influence voter behavior.2

February hasn’t been a particularly bullish month for US stocks, although its performance has been a little better over the past three decades.

Insight of the month. Despite the underperformance of international equities at the start the year, Morgan Stanley & Co. analysts see potential outperformance for European stocks going forward. Citing the alignment of multiple favorable factors, the strategists see the possibility of a 16% total return on MSCI Europe in 2024, with select sectors flagged for potential outperformance.3

February has not, historically, been one of the more bullish months of the year. The S&P 500 had a negative return in four of the past six Februaries, and from 1957-1989 February was a down month more often than not. It’s fared better since 1990—up 59% of the time (20 of 34 years), although its returns have been volatile, and its average return was the fourth lowest of all months during this period.4

Whether or not the market loses momentum this month, Morgan Stanley Wealth Management recently argued the economic soft landing many investors have been hoping for could translate into a range-bound 2024 rather than a “rate-driven reacceleration.”5

1 MorganStanley.com. Will the U.S. Presidential Election Change Fed Policy? 1/25/24.

2 MorganStanley.com. What Matters Most to Markets in the U.S. Election. 1/4/24.

3 MorganStanley.com. Why It’s Time to Be Bullish on European Equities. 1/26/23.

4All figures reflect S&P 500 (SPX) monthly closing prices, 1/2/57–12/31/23. Supporting document available upon request.

5 MorganStanley.com. The GIC Weekly: Cycle’s Achilles’ Heel: Liquidity. 1/29/24.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.