Market pulls back into Q4

E*TRADE from Morgan Stanley

Entering the final quarter of what has been a consistently surprising 2023, the US stock market is coming off back-to-back down months for the first time in a year—even as the economy continued to roll.

But as September drew to a close, investors were facing an expanding autoworkers strike and the prospect of a government shutdown (avoided, for the time being, by a last-minute deal), neither of which boosted market sentiment as stocks retreated to their lowest levels since early June.

Having significantly lowered inflation from last year’s highs, the Fed faces what may be an even more difficult task: reaching its 2% target level.

But as has been the case for more than a year, the discussion never strayed far from inflation and interest rates. The Fed didn’t raise rates in September, but it didn’t show any inclination to cut them—in fact, it revealed a majority of its board felt it would be necessary to hike again. Even after lowering inflation significantly from last year, the Fed faces what could be an even more difficult task: getting it down to their stated 2% target level.

That’s just one facet of this increasingly complex story. For example, both the autoworkers strike and a government shutdown (if one occurs in the future) have the potential to lower GDP—which could actually help the Fed’s inflation fight, as Morgan Stanley & Co. analysts recently pointed out.1 But what if the Fed eventually faces a weakening economy and higher-than-desired inflation? In that case, would the Fed take hike rates (to cool inflation) or leave them alone (to avoid further slowing the economy)? Or would they abandon their 2% inflation target and live with a higher level?

Before looking ahead to some Q4 market themes, let’s see where the markets stood at the end of last month.

US equities

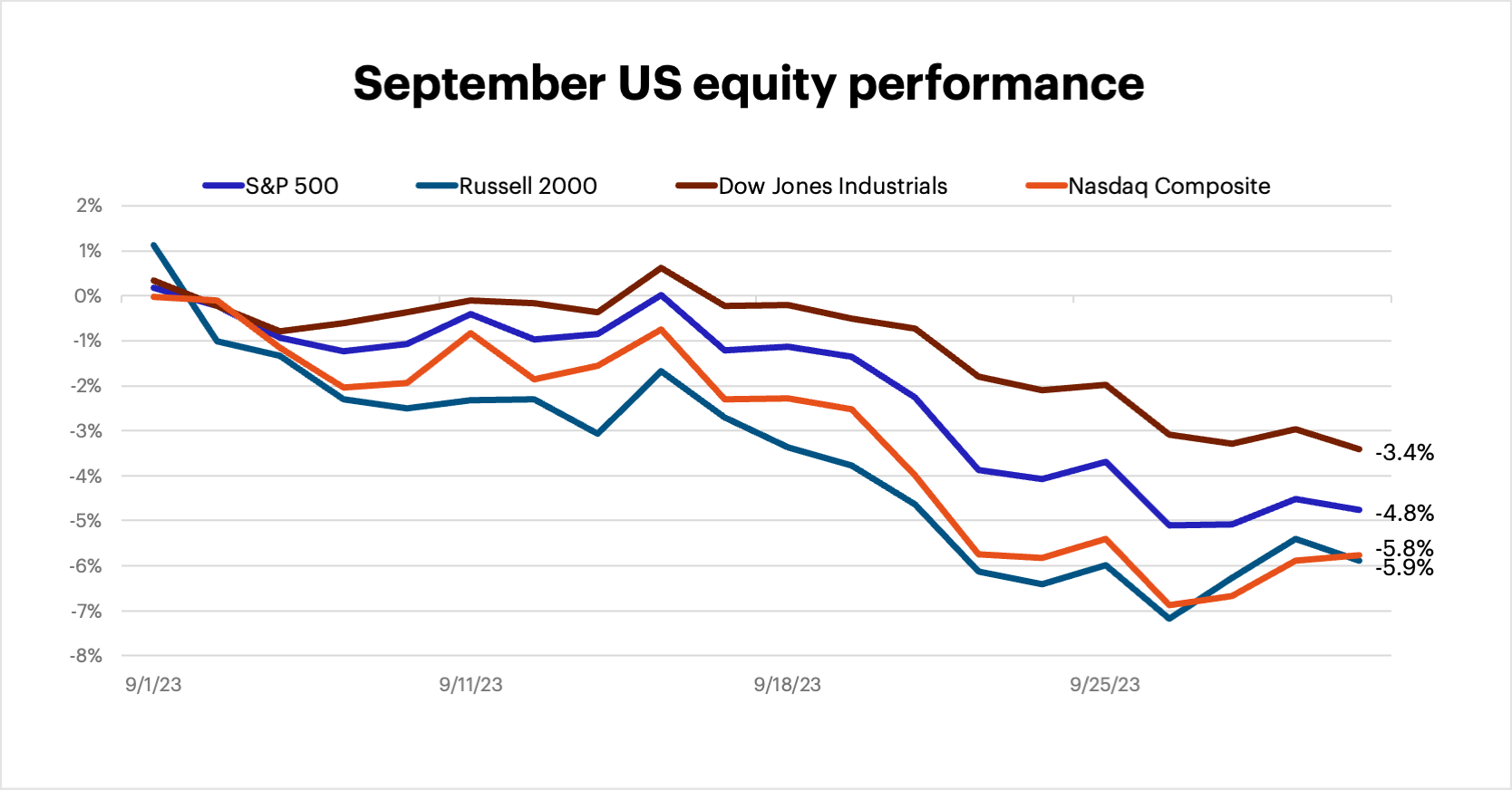

September certainly lived up to its bearish reputation. The S&P 500 fell 4.8% (its seventh negative September of the past decade), while the small-cap Russell 2000 and tech-heavy Nasdaq Composite posted even bigger losses:

FactSet Research Systems. (It is not possible to invest in an index.)

Sectors

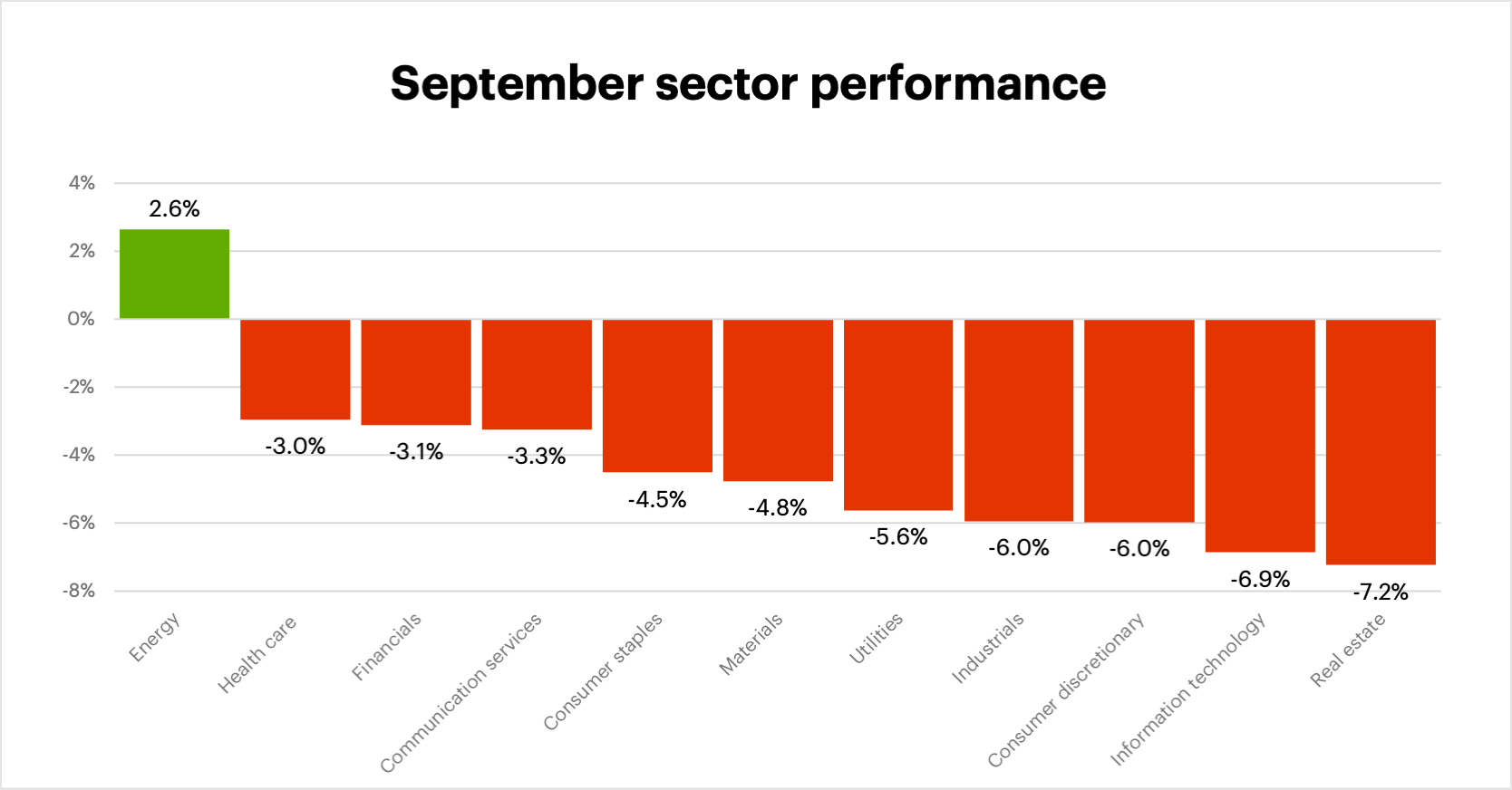

The only sector with a positive return in September was energy, which was boosted by crude oil prices that pushed to their highest levels in more than a year. Real estate and tech posted the biggest losses for the month:

FactSet Research Systems

International equities

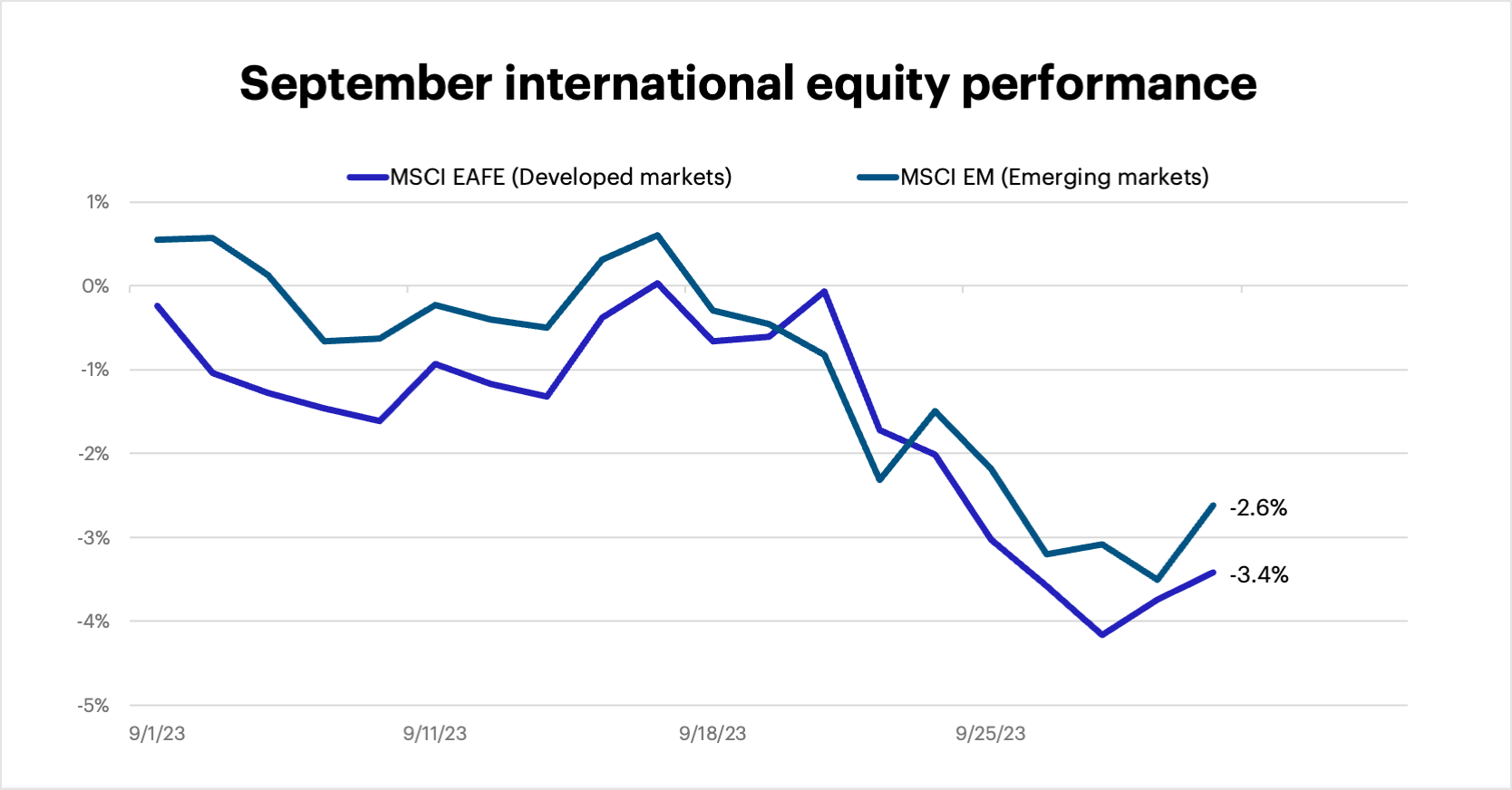

Global stocks fell less than the S&P 500 last month, with emerging markets slightly outperforming developed markets. The MSCI EM Index of emerging markets declined 2.6%, while the MSCI EAFE Index of developed markets fell 3.4%:

FactSet Research Systems (It is not possible to invest in an index.)

Fixed income

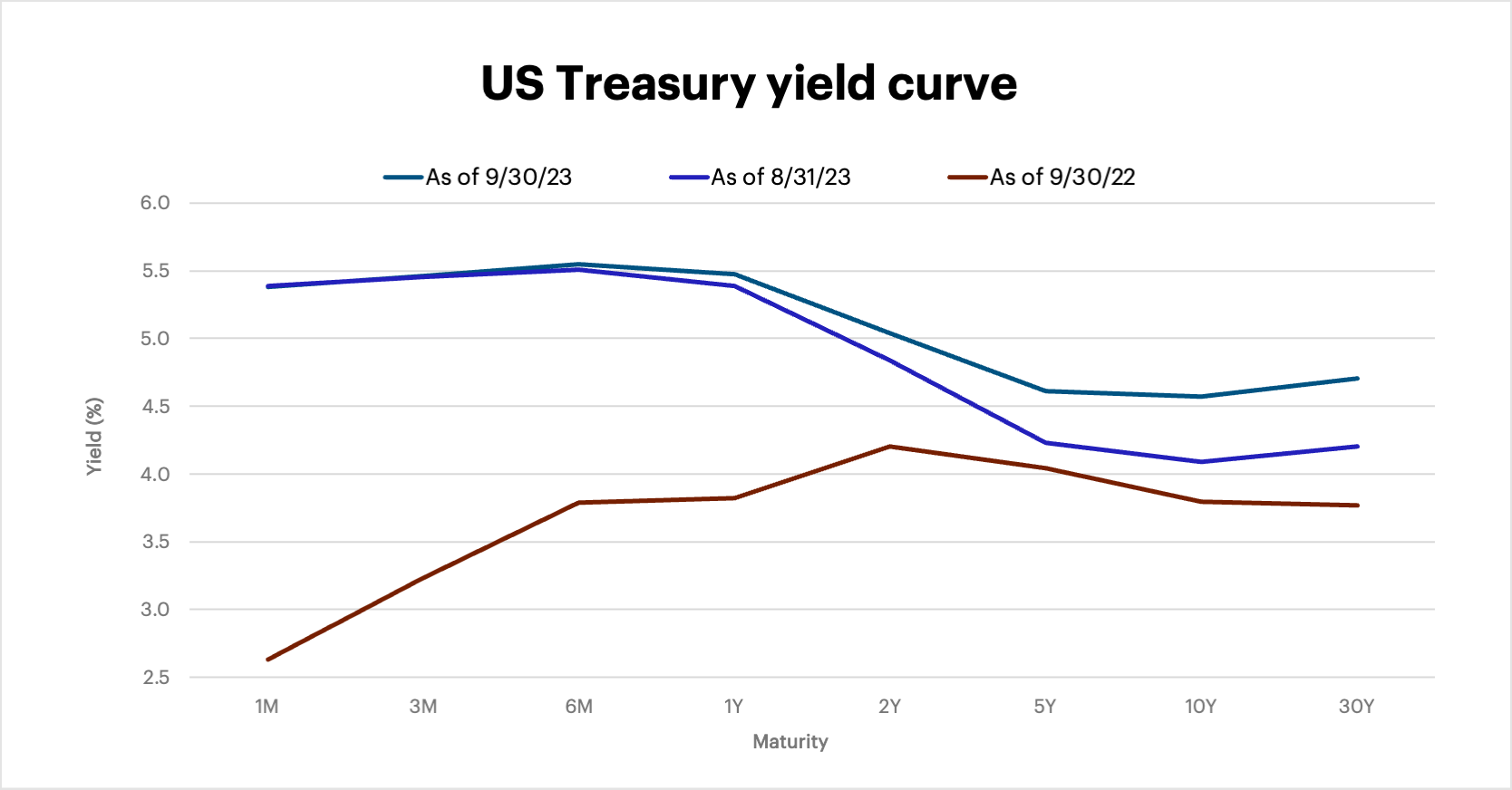

Bond prices mostly slumped last month as yields, which move in the opposite direction, hit their highest levels since 2006–2007. As was the case in August, longer-term yields increased the most. The benchmark 10-year Treasury yield ended September at 4.57%, up from 4.09% at the end of August (the biggest monthly jump in a year):

FactSet Research Systems

Looking ahead

A few thoughts as we enter the final quarter of 2023:

- Inflation sticky, rates high. Given the challenge of reducing inflation in a robust economy with high employment, interest rates are poised to remain higher for longer, even if the Fed has finished hiking. Unless inflation drops unexpectedly and significantly—and doesn’t immediately jump again—don’t expect the Fed to budge from its hawkish stance.

- Longer-term bonds more attractive? The upside of the interest rate picture continues to be meaningful fixed income yields, and not just at the short end of the yield curve. For the first time in many years, there may be more potential for attractive yields—and appreciation—in longer-term bonds.

- Growth opportunity. While tech and growth stocks have borne the brunt of the recent pullback, it may be worth looking at “quality defensive growth” stocks—companies with strong balance sheets that can preserve their pricing power and/or have the ability to keep raising dividends in the current environment.

It’s worth keeping in mind that even though stocks have pulled back for two months, the S&P 500 is still solidly positive for the year. The volatility we’ve seen recently is normal—and there may be more to come. The goal is to invest through it rather than react to it. As always, stay disciplined, diversified, and focused on the long term.

Thanks for reading, and we’ll talk to you again next month.

Head of Portfolio Construction for Morgan Stanley Portfolio Solutions

Mike Loewengart is Head of Portfolio Construction for Morgan Stanley Portfolio Solutions and a Managing Director in the Morgan Stanley Wealth Management Global Investment Office. Mike is responsible for the asset allocation and investment vehicle selections used in E*TRADE from Morgan Stanley’s advisory platforms. Prior to joining E*TRADE in 2007, Mike was the Director of Investment Management for a large multinational asset management company, where he oversaw corporate pension plan assets. Early in his career, Mike was a research analyst focusing on investment manager due diligence for the consulting divisions of several high-profile investment firms. Mike holds series 7, 24, and 66 designations, as well as the Chartered Alternative Investment Analyst (CAIA) designation. He is a graduate of Middlebury College with a degree in economics.

Executive Director, Morgan Stanley WM Global Investment Office

Andrew Cohen is an Executive Director in the Morgan Stanley Wealth Management Global Investment Office. Prior to joining E*TRADE in 2014, he was the Director of Investments and Operations for a large Registered Investment Advisor, where his responsibilities included investment manager research, asset allocation, and portfolio construction. Previously, he was a Senior Research Analyst and Team Leader for Morgan Stanley. He is a CFA® charterholder and a member of the CFA Institute and CFA Society New York. He is a graduate of Virginia Tech with a Bachelor of Science (B.S.) in finance.

1 Morgan Stanley.com. GDP, Inflation and a Possible Government Shutdown. 9/26/23.