Market cautious as tariffs return to center stage

- Stocks dip amid new tariff announcements

- Commodities in spotlight as copper, OJ prices surge

- This week: inflation data, retail sales, earnings season

Although US stocks logged new all-time highs for the third week in a row, they lost ground last week as the central market issue of 2025 pushed its way back into the headlines.

The S&P 500 (SPX) stumbled out of the gate last Monday as the White House set a new August 1 tariff deadline, pushed to a new record high by Thursday, then pulled back again on Friday after the President proposed new tariffs on Canada. (He also announced new tariffs on the European Union and Mexico over the weekend.) However, the market pared its losses on both days, and the index’s total decline for the week was modest:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks pause amid the Return of the T-Word.

The fine print: The market’s muted reaction to the latest volley of tariff news may suggest some investors are—for better or worse—becoming anesthetized to the stream of announcements, or are guessing that the tariff bark will be worse than the eventual bite (or both). Regardless, that attitude has not been adopted by the Fed, which is holding the line on seeing more clarity on tariffs before it cuts rates—despite continued pressure from the White House to do so.

The move: July orange juice futures (OJN5) soared more than 31% last week amid the White House's announcement of new tariffs on Brazilian products.

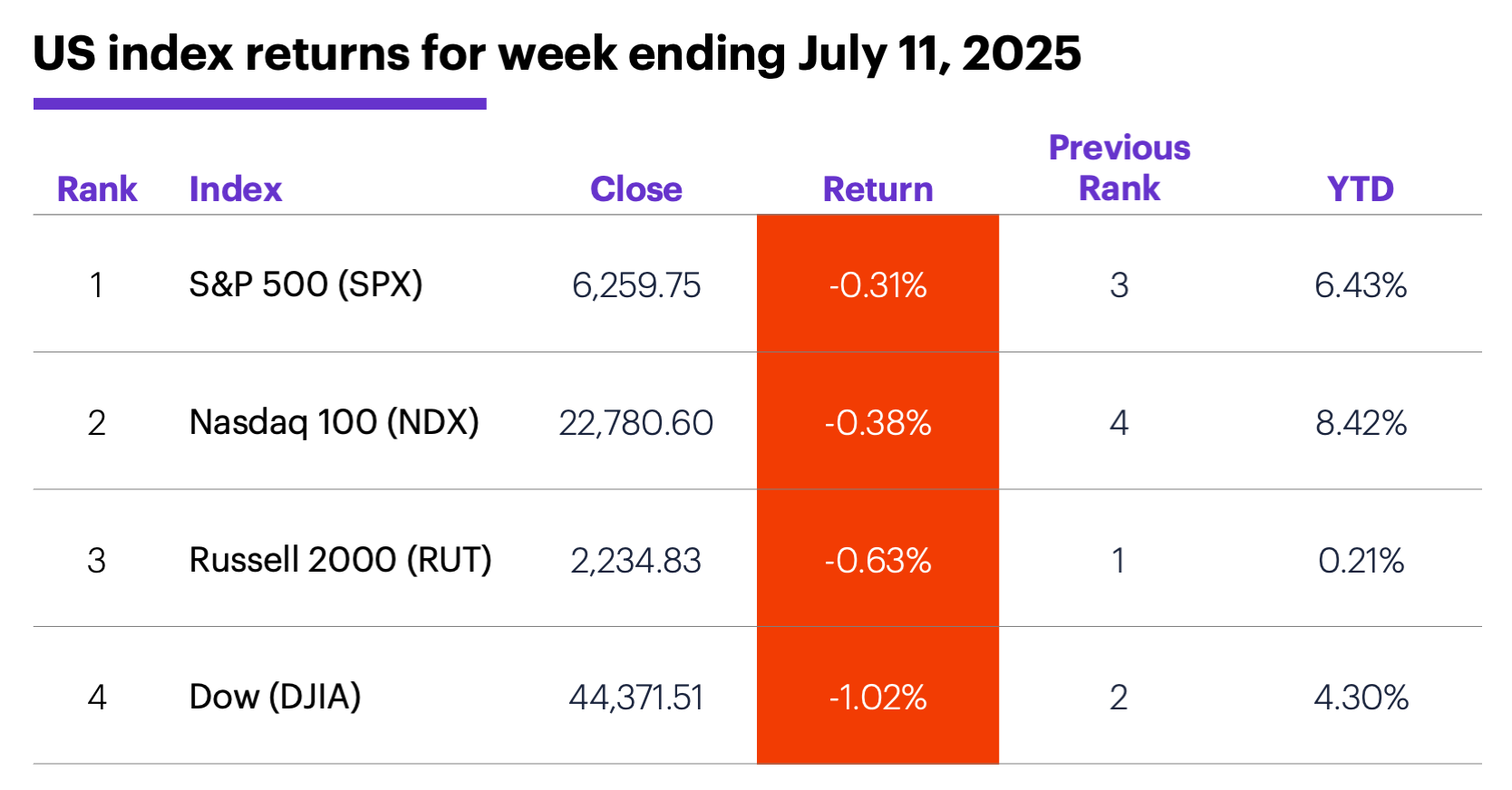

The scorecard: The SPX fell the least last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+2.4%), utilities (+0.7%), and industrials (+0.5%). The weakest sectors were financials (-2%), consumer staples (-1.8%), and communication services (-1.2%).

Stock moves: Rhythm Pharmaceuticals (RYTM) +36% to $88.37 on Wednesday, Newegg Commerce (NEGG) +71% to $49.24 on Friday. On the downside, Helen of Troy (HELE) -23% to $23.96 and Byrna Technologies (BYRN) -22% to $25.31, both on Thursday.

Yields: The benchmark 10-year Treasury yield edged 0.07% higher to 4.42%.

US dollar: The US Dollar Index (DXY) climbed 0.67 to 97.85.

Futures: August WTI crude oil (CLQ5) ended an up-and-down week $1.45 higher at $68.45. August gold (GCQ5) climbed $21.10 to $3,364 last week, thanks mostly to a strong Friday rally. Biggest up moves: September orange juice (OJU5) +31.5%, July ether (ETHN5) +15.4%. Biggest down moves: September Uranium (UXU5) -8.3%, December corn (ZCZ5) -5.7%.

Coming this week

This week brings the latest readings on inflation (CPI and PPI), retail spending, and consumer sentiment:

●Tuesday: consumer price index (CPI), Empire State Manufacturing Index

●Wednesday: producer price index (PPI), industrial production and capacity utilization, Fed Beige Book

●Thursday: retail sales, import price index, Philly Fed survey, business inventories, NAHB Housing Market Index

●Friday: housing starts and building permits, consumer sentiment (prelim)

Big banks signal the beginning of a new earnings season:

●Monday: Fastenal (FAST), Omnicom (OMC), Simulations Plus (SLP)

●Tuesday: Bank Of New York Mellon (BK), Blackrock (BLK), Citigroup (C), Crown Castle (CCI), Discover Financial (DFS), J.B. Hunt Transport (JBHT), JPMorgan Chase (JPM), Kinder Morgan (KMI)

●Wednesday: Bank of America (BAC), Cintas (CTAS), Goldman Sachs (GS), Johnson & Johnson (JNJ), Marten Transport (MRTN), Morgan Stanley (MS), Prologis (PLD), United Airlines (UAL)

●Thursday: Citizens Financial (CFG), Elevance Health (ELV), Fifth Third Bancorp (FITB), Netflix (NFLX), PepsiCo (PEP), Southern Copper (SCCO)

●Friday: Alcoa (AA), American Express (AXP), 3M (MMM), Schlumberger (SLB)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Copper market sees red

The new round of tariff announcements encompassed entire markets as well as specific countries. Last Tuesday, the White House’s proposed 50% tariff on all copper imports was followed by the biggest one-day jump in copper prices in more than three decades, with September copper futures (HGU5) jumping more than 17% intraday to a new record high:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Despite the high level of uncertainty surrounding the proposed tariff—when it would be implemented (if at all), and whether there would be specific country or product exemptions—Morgan Stanley & Co. analysts noted that, because the US is a net copper importer, the copper futures on the US-based COMEX exchange would be expected to trade at a higher premium to the copper futures listed on the London-based LME exchange.1

Analysts also singled out Southern Copper (SCCO) as a potential beneficiary in the event the proposed tariff materializes, since roughly 40% of its contracts are tied to the COMEX market.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com.US Plans 50% Copper Tariffs. 7/8/25.

2 MorganStanley.com.Trump to Announce 50% Copper Tariffs. 7/8/25.