Market plays waiting game

- Small caps lead “flattish” week for stocks

- Energy soars amid Middle East uncertainty

- This week: Fed inflation, durable goods orders

US stocks head into the final full week of June looking to reverse last week’s minor slump, as geopolitics and the Fed appeared to keep traders and investors slightly off balance.

While elevated energy prices reflected uncertainty about the potential for a wider Middle East conflict, the stock market’s response was much milder, at least through the end of last week. The S&P 500 (SPX) ended the shortened week little changed, and traded mostly within the previous week’s high-low range:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks mull Middle East turmoil and interest rate outlook.

The fine print: Last Wednesday, the Fed extended its holding pattern, leaving interest rates unchanged (as expected), while Chairman Jerome Powell repeated the mantra that the still-solid economy gives the central bank leeway to wait and see how tariffs affect the economy. But on Friday, Fed governor Christopher Waller opined that the Fed could cut rates as soon as July. Although it remains to be seen how the US strike on Iranian nuclear facilities over the weekend will impact this debate, additional uncertainty is unlikely to speed up the Fed's timeline.

The number: 0.4%, the increase in the retail sales “control group” reported last week. While total retail sales fell by a larger-than-expected -0.9% in May, the increase in the control group, which excludes autos and gas, suggested consumer spending was more robust than the headline number suggested. Takeaway: The economy may be slowing, but it hasn’t ground to a halt.

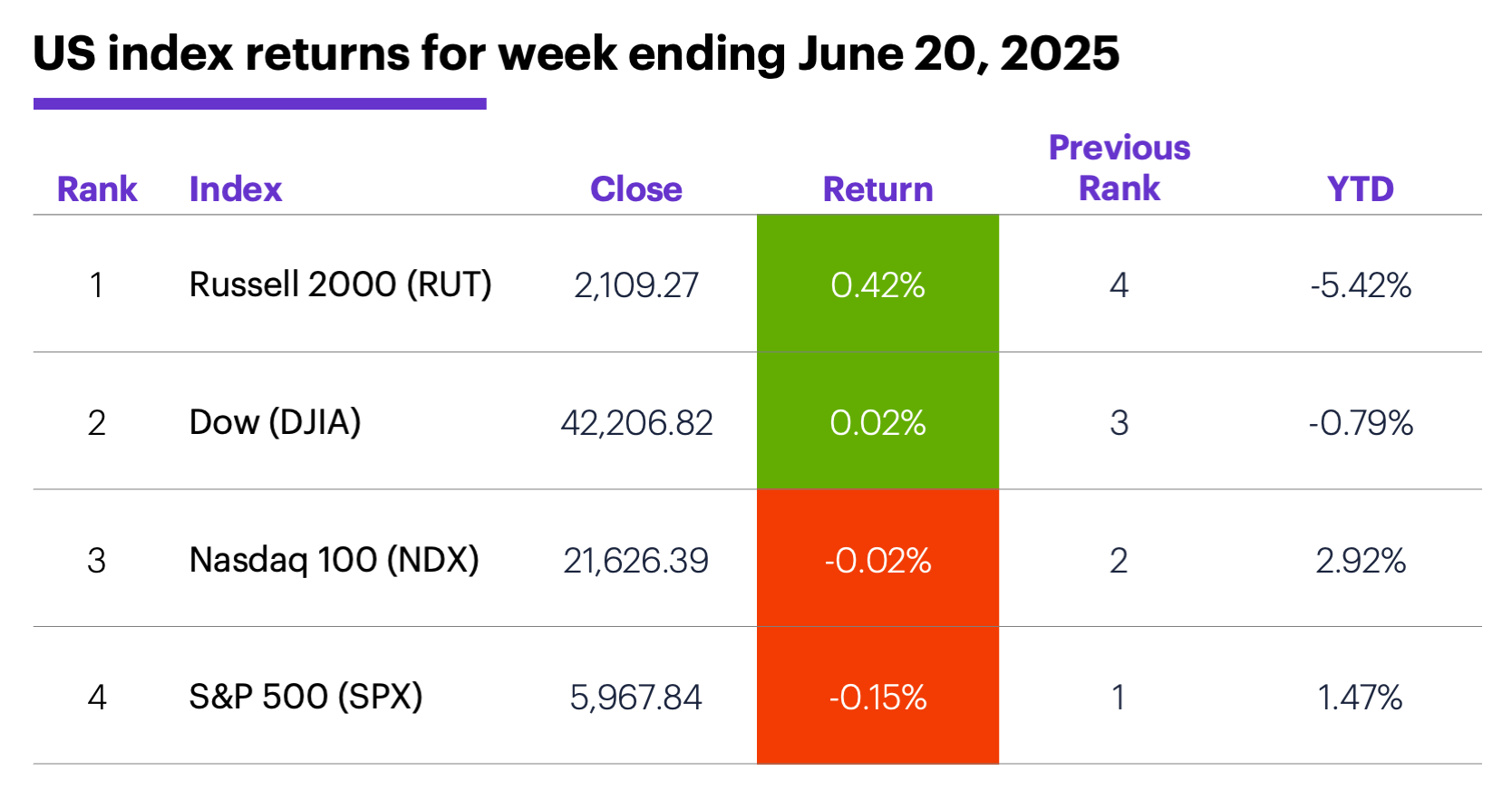

The scorecard: The Russell 2000 (RUT) small-cap index was last week’s standout:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+1.1%), tech (+0.9%), and financials (+0.8%). The weakest sectors were materials (-1.2%), communication services (-1.7%), and health care (-2.7%).

Stock moves: EchoStar (SATS) +49% to $25.11 on Monday, Houston American Energy (HUSA) +89% to $20 on Tuesday (then -13% to $17.50 on Wednesday and -15% to $14.80 on Friday). On the downside, Sarepta Therapeutics (SRPT) -42% to $20.94 on Monday, SolarEdge Technologies (SEDG) -33% to $15.96 on Tuesday.

Yields: The benchmark 10-year Treasury yield dipped 0.03% to 4.38% last week.

US dollar: The US Dollar Index (DXY) climbed modestly off its three-year lows, closing the week up 0.53 at 98.71.

Futures: Oil volatility continued, with August WTI crude oil (CLQ5) ending the week up $2.55 at $73.84. August gold (GCQ5) hit a five-week intraday high of $3,476.30 last Monday, then ended the week down $67.10 at $3,385.70.

Coming this week

This week’s economic calendar includes the Fed’s preferred inflation gauge (PCE Price Index), durable goods orders, and consumer confidence:

●Monday: S&P Global Manufacturing and Services PMIs (flash), existing home sales

●Tuesday: current account (Q1), S&P Case-Shiller Home Price, FHFA House Price Index, consumer confidence

●Wednesday: new home sales

●Thursday: durable goods orders, Q1 GDP (final), Chicago Fed National Activity Index, trade balance in goods (advance), retail and wholesale inventories (advance), pending home sales

●Friday: personal income and spending, PCE Price Index, consumer sentiment (final)

This week’s earnings include:

●Monday: Carnival (CCL), Commercial Metals (CMC), FactSet (FDS), KB Home (KBH), Progress Software (PRGS)

●Tuesday: AeroVironment (AVAV), FedEx (FDX), National Beverage (FIZZ), Levi Strauss (LEVI), TD Synnex (SNX)

●Wednesday: Apogee Enterprises (APOG), General Mills (GIS), Micron (MU)

●Thursday: Acuity (AYI), Concentrix (CNXC), Enerpac Tool Group (EPAC), McCormick & Company (MKC), Nike (NKE)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Quiet spring for housing

The longstanding inertia in the housing market doesn’t mean traders and investors should ignore this corner of the economy. As Chief Economic Strategist for Morgan Stanley Wealth Management Ellen Zentner recently pointed out, housing tends to lead the business cycle.

The housing market’s basic conundrum is that, although homes may not be as pricey as they were in late 2023, they are still quite expensive on a historical basis. Owners who locked in low, long-term mortgage rates in years past have little incentive to sell and finance a new home at current (higher) rate levels. Since they’re not selling, prices haven’t dropped, leaving many would-be home buyers on the outside looking in.

As Morgan Stanley US housing strategist Jim Egan noted, an estimated 75% of homeowners have mortgage rates below 5.5%,1 while current rates are closer to 7%. Although lower mortgage rates—say, below 6%—could help break the housing logjam, Egan explained mortgages are more directly impacted by longer-term (e.g., seven- to 10-year) rates, which are subject to open-market forces, rather than by Fed rate cuts.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 Wall Street Journal. Morgan Stanley Strategist on Unlocking the Housing Market. 5/18/25.